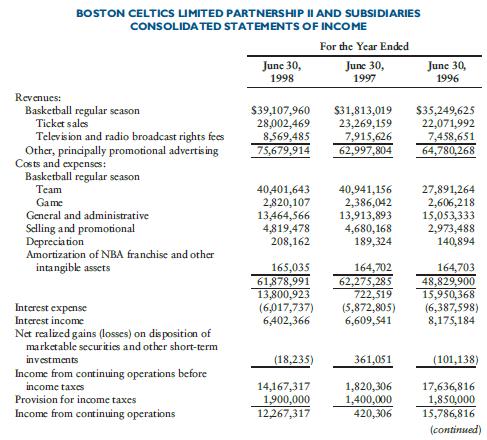

Question: Boston Celtics Limited Partnership II and

Boston Celtics Limited Partnership II and Subsidiaries presented the following consolidated

statements of income for 1998, 1997, and 1996.

Required

a. Comment on Amortization of NBA Franchise and Other Intangible Assets.

b. Would the discontinued operations be included in projecting the future? Comment.

c. The costs and expenses include team costs and expenses. Speculate on the major reason for the increase in this expense between 1996 and 1997.

d. What were the major reasons for the increase in income from continuing operations between 1997 and 1998?

e. Speculate on why distributions declared were higher in 1998 than 1996. (Notice that net income was substantially higher in 1996.)

Transcribed Image Text:

BOSTON CELTICS LIMITED PARTNERSHIP II AND SUBSIDIARIES CONSOLIDA TED STATEMENTS OF INCOME For the Year Ended June 30, 1998 June 30, 1997 June 30, 1996 Revenues: Basketball regular season Ticket sales Television and radio broadcast rights fees Other, principally promotional advertising Costs and expenses: Basketball regular season $39,107,960 28,002,469 8,569,485 75,679,914 $31,813,019 23,269,159 7,915,626 62,997,804 $35,249,625 22,071,992 7,458,651 64,780,268 40,401,643 2,820,107 13,464,566 4,819,478 208,162 Team 40,941,156 2,386,042 13,913,893 4,680,168 189,324 27,891,264 2,606,218 15,053,333 2,973,488 140,894 Game General and administrative Selling and promotional Depreciation Amortization of NBA franchise and other intangible assets 165,035 61,878,991 13,800,923 (6,017,737) 6,402,366 164,702 62,275,285 722,519 (5,872,805) 6,609,541 164,703 48,829,900 15,950,368 (6,387,598) 8,175,184 Interest expense Interest income Net realized gains (losses) on dis position of marketable securities and other short-term investments (18,235) 361,051 (101,138) Income from continuing operations before income taxes Provision for income taxes Income from continuing operations 14,167,317 1,900,000 12,267,317 1,820,306 1,400,000 420,306 17,636,816 1,850,000 15,786,816 (continued)

> Describe a proxy statement.

> Which of the following events, occurring subsequent to the balance sheet date, would require a note? a. Major fire in one of the firm’s plants b. Increase in competitor’s advertising c. Purchase of another company d. Introduction of new management te

> What are contingent liabilities? Are lawsuit against the firm contingent liabilities?

> Why are notes to statements necessary?

> What are the three principal financial statements of a corporation? Briefly describe the purpose of each statement.

> The following information for Lesky Corporation covers the year ended December 31, 2012: / Required Change this statement to a multiple-step format, as illustrated in this chapter.

> Are all financial statements presented with some kind of an accountant’s report? Explain.

> What type of opinion is expressed on a compilation?

> Will the accountant express an opinion on reviewed financial statements? Describe the accountant’s report for reviewed financial statements.

> Describe an auditor’s review of financial statements.

> Why do some unqualified opinions have explanatory paragraphs?

> What is the purpose of the SEC’s integrated disclosure system for financial reporting?

> What are the roles of management and the auditor in the preparation and integrity of the financial statements?

> In what year did the IASB publish an IFRS for SMEs? How did this impact the road map of convergence between IFRSs and U.S. GAAP?

> Professor Ball noted a number of problems with implementing IFRS. What were the problems noted by Professor Ball?

> The SEC announced that it would accept financial statements from private issuers without reconciliation to U.S. GAAP if they are prepared using IFRS, as issued by the International Accounting Standards Board. Comment on possible problems with this positi

> The following information for Decher Automotives covers the year ended 2012: Administrative expense………………………….. $ 62,000 Dividend income…………………………………… 10,000 Income taxes $............................................. 100,000 Interest expense ……………………………

> Describe the Norwalk Agreement.

> The SEC released for public comment a proposed road map for adoption of IFRS by public companies in the United States. What were the serious concerns?

> Briefly describe the PCAOB.

> Comment on the materiality implications of the Sarbanes-Oxley Act.

> Describe the book Accounting Trends & Techniques.

> If its accounting period ends December 31, would a company be using a natural business year or a fiscal year?

> Comment on the responsibility of private companies under the Sarbanes-Oxley Act.

> Comment on perceived benefits from Section 404 of the Sarbanes-Oxley Act.

> Under the Sarbanes-Oxley Act, what must the financial statement auditor do in relation to the company’s internal control?

> Comment on what Section 404 of the Sarbanes Oxley Act requires of companies.

> China Unicom (Hong Kong) Limited provides a full range of telecommunications services, including mobile and fixed line service, in China. They are listed on the New York Stock Exchange and filed a Form 20-F with the SEC for the period ended December 31,

> It is not important to know when cash is received and when payment is made. Comment.

> The cash basis does not reasonably indicate when the revenue was earned and when the cost should be recognized. Comment.

> Briefly explain the difference between an accrual basis income statement and a cash basis income statement.

> There are five different measurement attributes currently used in practice. List these measurement attributes.

> SFAC No. 5 indicates that, to be recognized, an item should meet four criteria, subject to the cost-benefit constraint and materiality threshold. List these criteria.

> According to SFAC No. 2, relevance and reliability are the two primary qualities that make accounting information useful for decision making. Comment on what is meant by relevance and reliability.

> Financial accounting is designed to measure directly the value of a business enterprise. Comment.

> The objectives of general-purpose external financial reporting are primarily to serve the needs of management. Comment.

> Briefly describe the following: a. Committee on Accounting Procedures b. Committee on Accounting Terminology c. Accounting Principles Board d. Financial Accounting Standards Board

> What is the FASB Conceptual Framework for Accounting and Reporting intended to provide?

> For those assets deemed to be impaired, the impairment to be recognized is measured as the amount by which the carrying amount of the assets exceeds the fair value of the assets. The Company’s determination of fair value is primarily ba

> Briefly describe the operating procedure for Statements of Financial Accounting Standards.

> Briefly explain the term generally accepted accounting principles.

> Explain the matching principle. How is the matching principle related to the realization concept?

> What is the basic problem with the monetary assumption when there has been significant inflation?

> Which U.S. government body has the legal power to determine generally accepted accounting principles?

> Dexter Company charges to expense all equipment that costs $25 or less. What concept supports this policy?

> Elliott Company constructed a building at a cost of $50,000. A local contractor had submitted a bid to construct it for $60,000 a. At what amount should the building be recorded? b. Should revenue be recorded for the savings between the cost of $50,000

> At which point is revenue from sales on account (credit sales) commonly recognized?

> Would an accountant record the personal assets and liabilities of the owners in the accounts of the business? Explain.

> Why did the FASB commence the Accounting Standards Codification™ project?

> An entity may choose between the use of the accrual basis of accounting and the cash basis. Comment.

> Some industry practices lead to accounting reports that do not conform to the general theory that underlies accounting. Comment.

> Many important events that influence the prospects for the entity are not recorded in the financial records. Comment and give an example.

> Is the presentation of a personal income statement appropriate?

> The same generally accepted accounting principles apply to all companies. Comment.

> What personal financial statement should be prepared when an explanation of changes in net worth is desired?

> In a personal statement of financial condition, what is the equity section called?

> When preparing a personal statement of financial condition, should assets and liabilities be presented on the basis of historical cost or estimated current value?

> Are comparative financial statements required when presenting personal financial statements?

> Is a statement of changes in net worth required when presenting personal financial statements?

> What is the basic personal financial statement?

> May personal financial statements be prepared only for an individual? Comment.

> Why are the financial data of a component unit included with the government entities reporting entity?

> For the government-wide statements, governmental activities are to be presented separately from the financial statements of business-type activities. Give one example of a governmental activity and one example of a business-type activity.

> Under GASB, which statement has been the most substantial pronouncement?

> It is proper to handle immaterial items in the most economical, expedient manner possible. In other words, generally accepted accounting principles do not apply. Comment, including a concept that justifies your answer

> What is the purpose of the book, Codification of Governmental Accounting and Financial Reporting Standards?

> How many members serve on the GASB? How many votes are needed to issue a pronouncement?

> Could a profit-oriented enterprise use fund accounting practices? Comment Answer: No. The accounting for a profit enterprise is centered on the entity concept and the efficiency of the entity. Fund accounting is centered on a self-balancing set of acc

> The accounting for not-for-profit institutions does not typically include the concept of efficiency. Indicate how the concept of efficiency can be incorporated in the financial reporting of a not-for-profit institution.

> The rating on an industrial revenue bond is representative of the probability of default of bonds issued with the full faith and credit of a governmental unit. Comment.

> Which organization provides a service whereby it issues a certificate of conformance to governmental units with financial reports that meet its standards?

> The budget for a state or local government is not as binding as a budget for a commercial business. Comment.

> How many funds will be used by a state or local Government?

> The accounting for governments is centered on the entity concept and the efficiency of the entity. Comment.

> Do not-for-profit organizations, other than governments, use fund accounting? Comment.

> No estimate or subjectivity is allowed in the preparation of financial statements. Discuss.

> List some objectives that could be incorporated into the financial reporting of a professional accounting organization.

> If quoted market prices are not available, a personal financial statement cannot be prepared. Comment.

> Give examples of disclosure in notes with personal financial statements.

> List some sources of information that may be available when preparing personal financial statements.

> Is the concept of working capital used with personal financial statements? Comment.

> GAAP as they apply to personal financial statements use the cash basis. Comment.

> For governmental accounting, define the following types of funds: 1. General fund 2. Proprietary fund 3. Fiduciary fund

> Why must the user be cautious in analyzing bank holding companies?

> To what agencies and other users of financial statements must banks report?

> Why are banks concerned with their loans/deposits ratios?

> Discuss why the concept of full disclosure is difficult to apply.

> Why are savings accounts liabilities for banks?

> Why are loans, which are usually liabilities, treated as assets for banks?

> What are the main sources of revenue for banks?

> Insurance companies tend to have a stock market price at a discount to the average market price (price/ earnings ratio). Indicate some perceived reasons for this relatively low price/earnings ratio.

> Insurance industry-specific financial ratios are usually prepared from financial statements prepared under what standards?

> Briefly describe the unique aspects of revenue recognition for an insurance company.

> Briefly describe the difference between accounting for intangibles for an insurance company under GAAP and under SAP?

> For an insurance company, describe the difference between GAAP reporting and SAP reporting of deferred policy acquisition costs?

> Why could an insurance company with substantial investments in real estate represent a risk?

> Annual reports that insurance companies issue to the public are in accordance with what accounting standards?

> The consistency concept requires the entity to give the same treatment to comparable transactions from period to period. Under what circumstances can an entity change its accounting methods, provided it makes full disclosure?

> Are annual reports filed with state insurance departments in accordance with U.S. GAAP?

> Explain how the publication Financial Analysis of the Motor Carrier Industry could be used to determine the percentage of total revenue a firm has in relation to similar trucking firms?