Question: Milwaukee Specialty Chemical Company (MSCC) is a

Milwaukee Specialty Chemical Company (MSCC) is a diversified chemical processing company. The firm manufactures swimming pool chemicals, chemicals for metal processing, specialized chemical compounds, and pesticides.

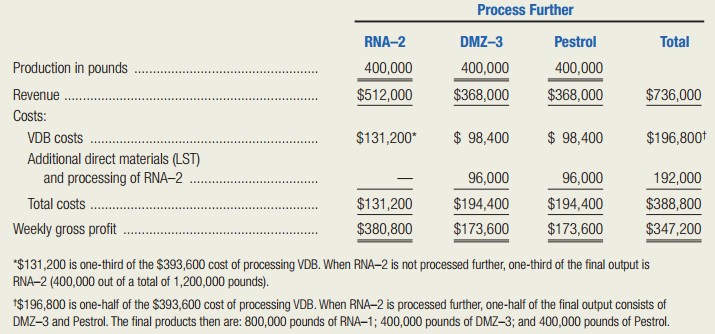

Currently, the Noorwood plant is producing two derivatives, RNA–1 and RNA–2, from the chemical compound VDB developed by the company’s research labs. Each week 1,200,000 pounds of VDB are processed at a cost of $393,600 into 800,000 pounds of RNA–1 and 400,000 pounds of RNA–2. The proportion of these two outputs cannot be altered, because this is a joint process. RNA–1 has no market value until it is converted into a pesticide with the trade name Fastkil. Processing RNA–1 into Fastkil costs $384,000. Fastkil wholesales at $80 per 100 pounds.

RNA–2 is sold as is for $128 per hundred pounds. However, management has discovered that RNA–2 can be converted into two new products by adding 400,000 pounds of compound LST to the 400,000 pounds of RNA–2. This joint process would yield 400,000 pounds each of DMZ–3 and Pestrol, the two new products. The additional direct-material and related processing costs of this joint process would be $192,000. DMZ–3 and Pestrol would each be sold for $92.00 per 100 pounds. The company’s management has decided not to process RNA–2 further based on the analysis presented in the following schedule.

Required:

Evaluate MSCC’s management’s analysis, and make any revisions that are necessary. Your critique and analysis should indicate:

a. Whether management made the correct decision.

b. The gross savings or loss per week resulting from the decision not to process RNA–2 further, if different from management’s analysis.

Transcribed Image Text:

Process Further RNA-2 DMZ-3 Pestrol Total Production in pounds 400,000 400,000 400,000 Revenue $512,000 $368,000 $368,000 $736,000 Costs: VDB costs $131,200* $ 98,400 $ 98,400 $196,800t Additional direct materials (LST) and processing of RNA–2 96,000 96,000 192,000 Total costs . $131,200 $194,400 $194,400 $388,800 Weekly gross profit $380,800 $173,600 $173,600 $347,200 "$131,200 is one-third of the $393,600 cost of processing VDB. When RNA-2 is not processed further, one-third of the final output is RNA-2 (400,000 out of a total of 1,200,000 pounds). 1$196,800 is one-half of the $393,600 cost of processing VDB. When RNA-2 is processed further, one-half of the final output consists of DMZ-3 and Pestrol. The final products then are: 800,000 pounds of RNA-1; 400,000 pounds of DMZ-3; and 400,000 pounds of Pestrol.

> Refer to the cost and production data for the Wave Darter in Exhibit 15–5. The target profit is $60,000. Exhibit 15-5: Required: Use the general formula for determining a markup percentage to compute the required markup percentages wi

> The following data pertain to Legion Lighting Company’s oak-clad, contemporary chandelier. Variable manufacturing cost ............................................................... $300 Applied fixed manufacturing cost .................................

> Should actual or budgeted service department costs be allocated? Why?

> Rosario Company produces a single product in its Buenos Aires plant, which currently sells for 7.50 p per unit. Fixed costs are expected to amount to 90,000 p for the year, and all variable manufacturing and administrative costs are expected to be incurr

> The following data pertain to LawnMate Corporation’s top-of-the-line lawn mower. Variable manufacturing cost ....................................................... $275 Applied fixed manufacturing cost ...................................................

> Refer to the data given in the preceding two exercises. 1. Prepare a table of Serendipity Sound’s revenue, cost, and profit relationships. For guidance refer to panel C of Exhibit 15–3. 2. Draw a graph similar to panel

> Refer to the preceding exercise. The divisional controller at Serendipity Sound’s Minneapolis Division has estimated the following cost data for the division’s sound systems. (Assume there are no fixed costs.) Quantit

> List the seven steps in the decision-making process

> Are the concepts underlying a relevant-cost analysis still valid in an advanced manufacturing environment? Are these concepts valid when activity-based costing is used? Explain.

> “Accounting systems should produce only relevant data and forget about the irrelevant data. Then I’d know what was relevant and what wasn’t!” Comment on this remark by a company president.

> Give two examples of sunk costs, and explain why they are irrelevant in decision making.

> There is an important link between decision making and managerial performance evaluation. Explain

> How is sensitivity analysis used to cope with uncertainty in decision making?

> Briefly describe the proper approach to making a production decision when limited resources are involved.

> What is a joint production process? Describe a special decision that commonly arises in the context of a joint production process. Briefly describe the proper approach for making this type of decision.

> Briefly describe the proper approach for making a decision about adding or dropping a product line.

> What behavioral tendency do people often exhibit with regard to opportunity costs?

> Define the term reciprocal services.

> Define the term opportunity cost, and give an example of one.

> Why might a manager exhibit a behavioral tendency to inappropriately consider sunk costs in making a decision?

> Is the book value of inventory on hand a relevant cost? Why?

> List and explain two important criteria that must be satisfied in order for information to be relevant.

> What is meant by each of the following potential characteristics of information: relevant, accurate, and timely? Is objective information always relevant? Accurate?

> Ontario Pump Company, a small manufacturing company in Toronto, Ontario, manufactures three types of pumps used in a variety of applications. For many years the company has been profitable and has operated at capacity. However, in the last two years pric

> All Sports Company’s production manager, Chris Adler, had requested to have lunch with the company president. Adler wanted to put forward his suggestion to add a new product line. As they finished lunch, Meg Thomas, the company presiden

> New Jersey Chemical Company manufactures two industrial chemical products, called z anide and kreolite. Two machines are used in the process, and each machine has 24 hours of capacity per day. The following data are available: The company can produce and

> Refer to the data given in the preceding exercise for Plato Corporation. Assume that the direct-labor rate is $12 per hour, and 11,000 labor hours are available per year. In addition, the company has a short supply of machine time. Only 9,000 hours are a

> Refer to the data given in Exercise 6. Breakfasttime Cereal Company has an opportunity to process its Crummies further into a mulch for ornamental shrubs. The additional processing operation costs $1.50 per kilogram, and the mulch will sell for $10.50 pe

> Plato Corporation manufactures two products, Alpha and Beta. Contribution margin data follow. Plato Corporation’s production process uses highly skilled labor, which is in short supply. The same employees work on both products and earn

> Global’s special order also requires 1,000 kilograms of genatope, a solid chemical regularly used in the company’s products. The current stock of genatope is 8,000 kilograms at a book value of 12.15 p per kilogram. If the special order is accepted, the f

> Global Chemical Company, located in Buenos Aires, Argentina, recently received an order for a product it does not normally produce. Since the company has excess production capacity, management is considering accepting the order. In analyzing the decision

> Juarez Corporation produces cleaning compounds and solutions for industrial and household use. While most of its products are processed independently, a few are related. Grit 337, a coarse cleaning powder with many industrial uses, costs $3.20 a pound to

> Thorpe Industries produces chemicals for the swimming pool industry. In one joint process, 10,000 gallons of GSX are processed into 7,000 gallons of xenolite and 3,000 gallons of banolide. The cost of the joint process, including the GSX, is $17,500. The

> College Town Pizza’s owner bought his current pizza oven two years ago for $10,500, and it has one more year of life remaining. He is using straight-line depreciation for the oven. He could purchase a new oven for $2,200, but it would last only one year.

> If Toon Town Toy Company closes its Packaging Department, the department manager will be appointed manager of the Cutting Department. The Packaging Department manager m a kes $51,000 per year. To hire a new Cutting Department manager will cost Toon Town

> Toon Town Toy Company is considering the elimination of its Packaging Department. Management has received an offer from an outside firm to supply all Toon Town’s packaging needs. To help her in making the decision, Toon Town’s president has asked the con

> Day Street Deli’s owner is disturbed by the poor pr o fit performance of his ice cream counter. He has prepared the following profit analysis for the year just ended. Required: Criticize and correct the owner’s analys

> Refer to the data given in the preceding exercise. Data given in preceding exercise: Breakfasttime Cereal Company manufactures two breakfast cereals in a joint process. Cost and quantity information is as follows: Required: Use the relative-sales-valu

> Redo Exhibit 14–4 without the irrelevant data. Exhibit 14-1: 1. Clarity the decision problem 2. Specity the oriterion Managerial accountant participates as part of cross-functional Quantitative Analysis 3 Identify the alternatives m

> Choose an organization and a particular decision situation. Then give examples, u s ing that decision context, of each step illustrated in Exhibit 14–1. Exhibit 14-1: 1. Clarify the decision problem 2. Specify the criterion Manager

> Contemporary Trends sells paint and paint supplies, carpet, and wallpaper at a single-store location in suburban Baltimore. Although the company has been very profitable over the years, management has seen a significant decline in wallpaper sales and ear

> CoffeeTime, Inc., manufactures two types of electric coffeemakers, Regular and Deluxe. T h e major difference between the two appliances is capacity. Both are considered top-quality units and sell for premium prices. Both coffeemakers pass through two ma

> Galaxy Candy Company manufactures two popular candy bars, the Eclipse bar and the Nova bar. Both candy bars go through a mixing operation where the various ingredients are combined, and the Coating Department where the bars from the Mixing Department are

> Time Saver Meals, Inc., offers monthly service plans providing prepared meals that are delivered to the customers’ homes. The target market for these meal plans includes double-income families with no children and retired couples in upper income brackets

> Oceana Corporation manufactures and sells three products, which are manufactured in a factory with four departments. Both labor and machine time are applied to the products as they pass through each department. The machines and labor skills required in e

> Excalibur, Inc., received an order for a piece of special machinery from Rex Company. J ust as Excalibur completed the machine, Rex Company declared bankruptcy, defaulted on the order, and forfeited the 10 percent deposit paid on the selling price of $21

> In addition to fine chocolate, International Chocolate Company also produces chocolate-covered pretzels in its Savannah plant. This product is sold in five-pound metal canisters, which also are manufactured at the Savannah facility. The plant manager, Ma

> Breakfasttime Cereal Company manufactures two breakfast cereals in a joint process. Cost and quantity information is as follows: Required: Use the physical-units method to allocate the company’s joint production cost between Yummies a

> PennTech Corporation has been producing two precision bearings, components T79 and B81, f or use in production in its central Pennsylvania plant. Data regarding these two components follow. PennTech’s annual requirement for these compon

> Palisades Corporation’s Midwest Division manufactures subassemblies that are used in the corporation’s final products. Lynn Hardt of Midwest’s Profit Planning Department has been assigned the task of determining whether a component, JY–65, should continu

> Treasure Island Beach Equipment, Inc., manufactures deluxe beach cabanas in Tampa, Florida. Its manufacturing plant has the capacity to produce 2,500 cabanas each month. Current monthly production is 1,875 cabanas. The company normally charges $525 per c

> Mercury Skateboard Company manufactures skateboards. Several weeks ago, the firm received a special-order inquiry from Venus, Inc. Venus desires to market a skateboard similar to one of Mercury’s and has offered to purchase 11,000 units if the order can

> Handy Dandy Tools Company manufactures electric carpentry tools. The Production Department has met all production requirements for the current month and has an opportunity to produce additional units of product with its excess capacity. Unit selling pric

> Martinez, Inc., is a small firm involved in the production and sale of electronic business products. The company is well known for its attention to quality and innovation. During the past 15 months, a new product has been under development that allows us

> Cincinnati Flow Technology (CFT) has purchased 10,000 pumps annually from Kobec, Inc. Because the price keeps increasing and reached $102.00 per unit last year, CFT’s management has asked for an estimate of the cost of manufacturing the pump in CFT’s fac

> Dentech, Inc., uses 10 units of part RM67 each month in the production of dentistry equipment. The cost of manufacturing one unit of RM67 is the following: Direct material ..................................................................................

> Chef Gourmet, Inc., has assembled the following data pertaining to its two most popular products. Past experience has shown that the fixed manufacturing overhead component included in the cost per machine hour averages $30. Management has a policy of fil

> Golden Gate Fashions, Inc. a high-fashion dress manufacturer, is planning to market a new cocktail dress for the coming season. Golden Gate Fashions supplies retailers primarily on the west coast. Four yards of material are required to lay out the dress

> Refer to the data given in the preceding exercise. Data in preceding exercise: Bay State Community College enrolls students in two departments, Liberal Arts and Sciences. The college also has two service departments, the Library and the Computing Servic

> The board of education for the Blue Ridge School District is considering the acquisition of several minibuses for use in transporting students to school. Five of the school district’s bus routes are under populated, with the result that the full-size bus

> Instant Dinners, Inc. (IDI), is an established manufacturer of microwavable frozen foods. L eland Forrest is a member of the planning and analysis staff. Forrest has been asked by Bill Rolland, chief financial officer of IDI, to prepare a net-present-val

> Discuss the pros and cons of the accounting rate of return as an investment criterion.

> How is an investment project’s accounting rate of return defined? Why do the accounting rate of return and internal rate of return on a capital project generally differ?

> What is meant by the term payback period? How is this criterion sometimes used in capital budgeting?

> Define the term profitability index. How is it used in ranking investment proposals?

> Why may the net-present-value and internal-rate-of return methods yield different rankings for investments with different lives?

> Explain how a gain or loss on disposal is handled in a capital-budgeting analysis.

> Why is accelerated depreciation advantageous to a business?

> Distinguish between the following approaches to discounted-cash-flow analysis: total-cost approach versus incremental-cost approach.

> Bay State Community College enrolls students in two departments, Liberal Arts and Sciences. The college also has two service departments, the Library and the Computing Services Department. The usage of these two service departments’ out

> List and briefly explain four assumptions underlying discounted-cash-flow analysis.

> List and briefly explain two advantages that the net-present-value method has over the internal-rate of-return method.

> Explain the following terms: recovery of investment versus return on investment.

> State the decision rule used to accept or reject an investment proposal under each of these methods of analysis: (1) net-present-value method and (2) internal-rate-of return method.

> Briefly explain the concept of discounted-cash-flow analysis. What are the two common methods of discounted-cash-flow analysis?

> “The greater the discount rate, the greater the present value of a future cash flow.” True or false? Explain your answer.

> Distinguish between the following two types of capital budgeting decisions: acceptance-or-rejection decisions and capital-rationing decisions.

> “Time is money!” is an old saying. Relate this statement to the evaluation of capital-investment projects.

> (Appendix B) Briefly describe two correct methods of net-present-value analysis in an inflationary period. Appendix B: The sales-price variance is the difference between the actual and budgeted sales prices multiplied by the actual sales volume. This va

> Tropics Fruit Company, based on Oahu, grows, processes, cans, and sells three main pineapple products: sliced, crushed, and juice. The outside skin is cut off in the Cutting Department and processed as animal feed. The feed is treated as a by-product. Th

> Refer to the data given in the preceding exercise. Data given in preceding exercise: Aurora National Bank has two service departments, the Human Resources (HR) Department and the Computing Department. The bank has two other departments that directly ser

> Edmonton Chemical Company manufactures two industrial chemical products in a joint process. In May, 10,000 gallons of input costing $180,000 were processed at a cost of $450,000. The joint process resulted in 8,000 pounds of Resoline and 2,000 pounds of

> Define the following terms: joint production process, joint costs, joint products, split-off point, separable costs, and by-product.

> Explain the difference between two-stage allocation with departmental overhead rates and activity-based costing. Which approach generally results in more accurate product costs?

> How does the managerial accountant determine the department sequence in the step-down method? How are ties handled?

> Explain briefly the main differences between the direct, step-down, and reciprocal-services methods of service department cost allocation.

> Distinguish between a service department and a production department. Give an example of the counterpart of a manufacturer’s “production” department in a bank.

> Define the term net realizable value, and explain how this concept can be used to allocate joint costs.

> What are the two main drawbacks of the payback method?

> Give an example of a cash flow that is not on the income statement. How do you determine the after-tax amount of such a cash flow?

> What is a depreciation tax shield? Explain the effect of a depreciation tax shield in a capital-budgeting analysis.

> Aurora National Bank has two service departments, the Human Resources (HR) Department and the Computing Department. The bank has two other departments that directly service customers, the Deposit Department and the Loan Department. The usage of the two s

> Briefly describe the time-and-material pricing approach

> Could tear-down methods be used effectively for target pricing in a service-industry company, such as a hotel or an airline? Explain.

> Explain the role of value engineering in target costing

> Why is a focus on the customer such a key principle of target costing?

> Explain the phrase price-led costing.

> Briefly explain the concept of return-on-investment pricing.

> Explain the behavioral problem that can result when cost-plus prices are based on variable cost.

> What is the primary disadvantage of basing the cost plus pricing formula on absorption cost?