Question: Refer to Exhibit 4-2 and 4-

Refer to Exhibit 4-2 and 4-3 in Chapter 4. Review the exhibits and compare them.

Required:

1. Differentiate between the two permissible methods under IFRS for classifying assets and liabilities on the SFP.

2. Refer again to Exhibit 4-2 and 4-3. Each entity shows one line for PPE rather than an expanded listing of each major category. Why do you think this has been done?

3. State a challenge for a financial statement user when an entity prepares its SFP using a liquidity approach without using a current and non-current classification.

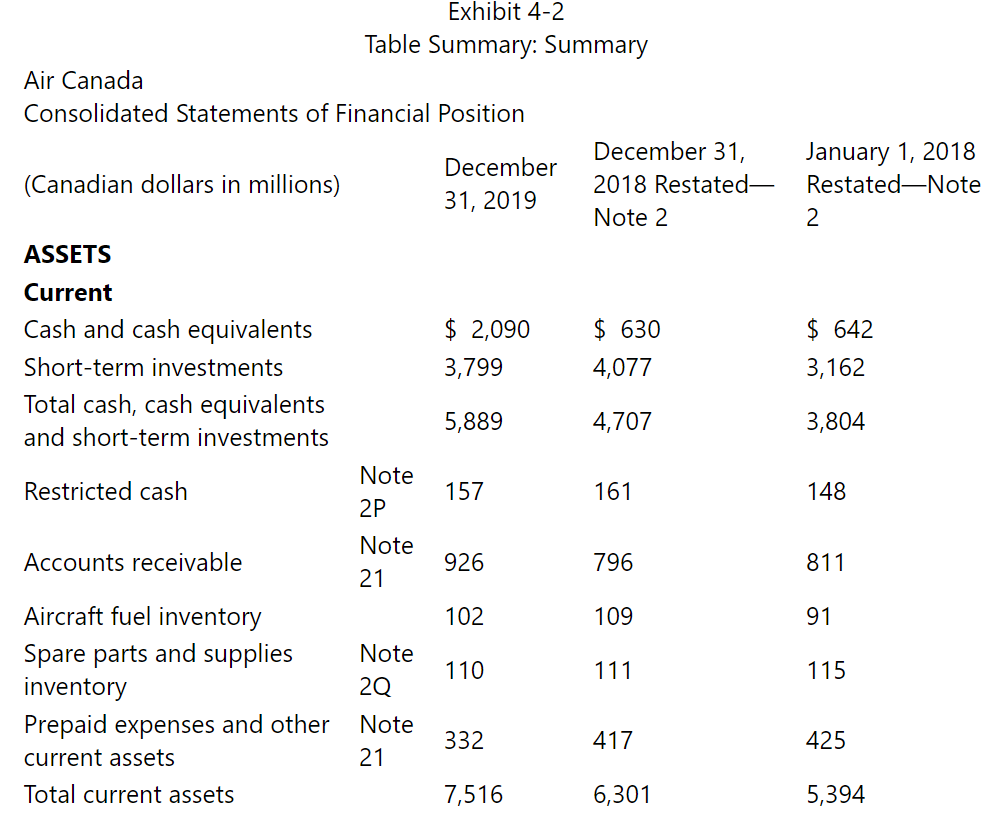

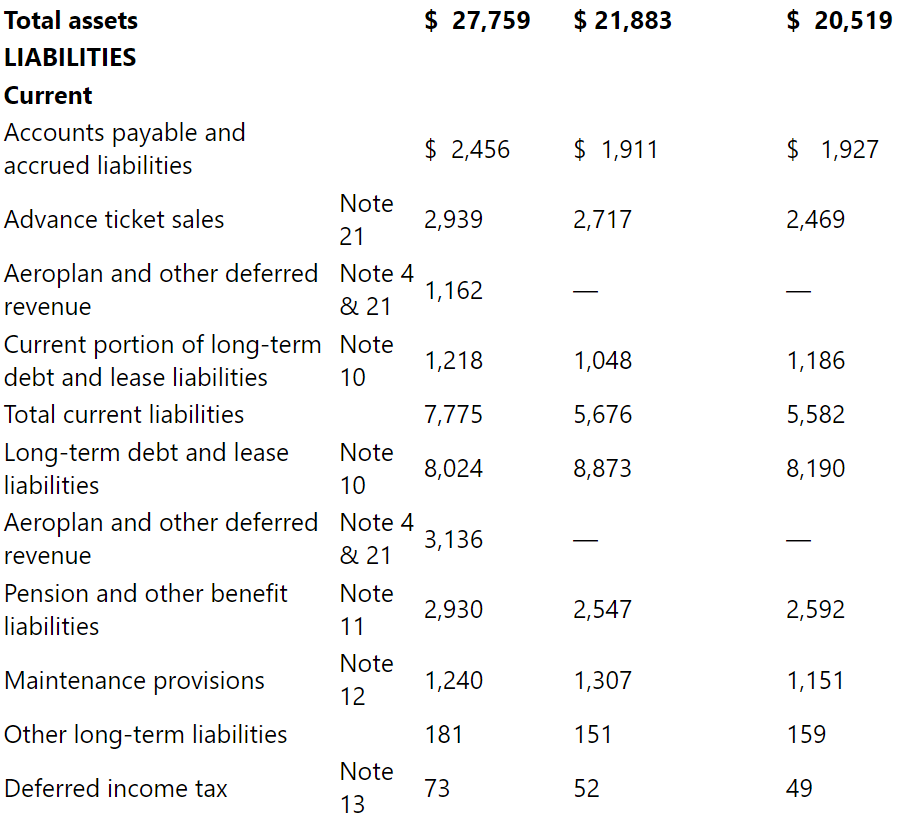

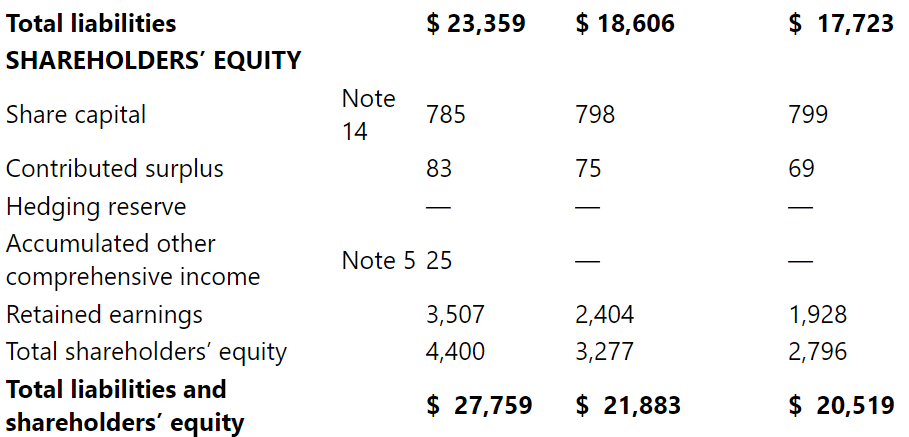

Data from Exhibit 4-2:

Exhibit 4-2 presents the consolidated SFP for Air Canada with the traditional format used by Canadian companies. Note that there are three columns. The third column is an opening balance sheet for the comparative period, which is required because Air Canada had a change in accounting policy. More on that issue later.

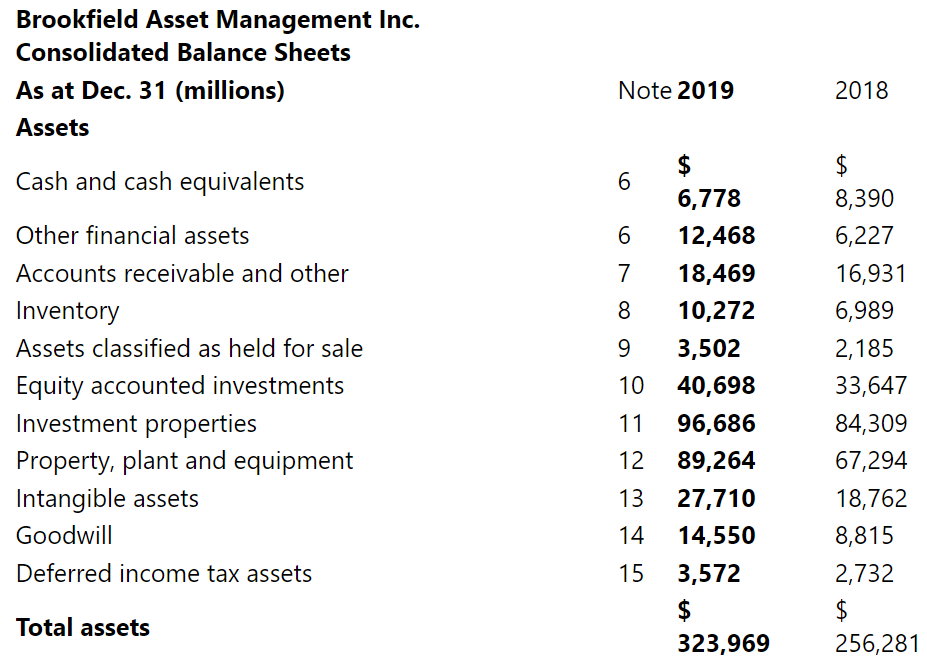

Data from Exhibit 4-3:

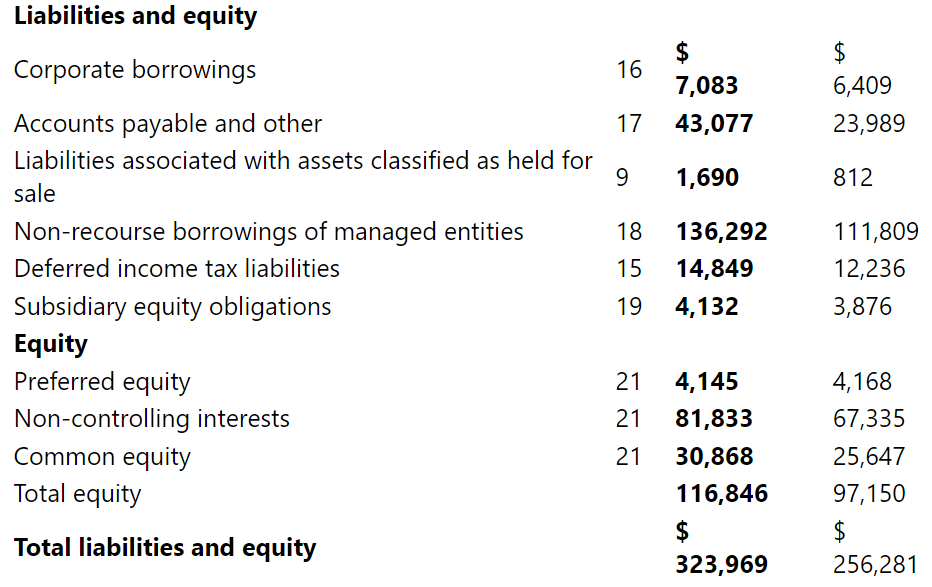

Exhibit 4-3 presents the consolidated SFP for Brookfield Asset Management Inc. using the alternative format based on liquidity.

Line Items

IFRS specifies that the SFP should contain 18 specific line items, to the extent that the entity has a material amount of those items. Air Canada shows 28 line items and Brookfield Asset Management Inc. shows 20 line items, a somewhat more detailed listing than required.

You will notice that there are no subdivisions within each of the current and noncurrent classifications. This linear presentation is increasingly popular among corporations, since there is limited space for detail. However, entities are free to present greater detail in the form of additional line items, headings, and subtotals that may help the reader understand the company’s financial position. For example, PP&E (property, plant, and equipment) might be expanded by listing the major categories on the face of the statement with a subtotal for PP&E

> Dominion Mobile Inc. provides cellular phone services. The company conducts a special sales campaign in which new subscribers will get a high-end cell phone for only $100 if they sign a 36-month contract that has a service fee of $100 per month. Thus, th

> BigBoy Equipment Inc. sells heavy-duty forklift trucks. Model 217A has a stand-alone price of $140,000. BigBoy offers to sell the 217A inclusive of a three-year service contract for $180,000. Required: Prepare a journal entry to record the sale of one Mo

> Chapnik Equipment Corp. (CEC) produced custom-designed machinery for a long-time customer. The direct cost to produce the machinery was $1.4 million. CEC sold the equipment to the customer for $2.0 million. The machinery was delivered, installed, and tes

> On 30 April 20X2, Neuman Ltd. sells a product to a customer for $600,000. The product carries a one-year assurance warranty. Neuman management estimates that the probable cost of fulfilling the warranty will be $50,000. Between 1 May and 31 December 20X2

> Beaver Ltd. is a retail company that sells sporting goods. It has a customer loyalty program that allows customers to earn points based on sales made. These points can be accumulated and used for future purchases. One customer loyalty point is awarded fo

> GoRight Inc. (GRI) is a franchisor who sells the rights to its trademark to franchisees. The franchisee pays an upfront, nonrefundable deposit of $1,000. This amount is used to cover the expenses for GRI performing a check on the franchiseeâ€&

> Drabinski Ltd. decided on 1 July 20X3 to dispose of an asset group consisting of land, a building, and equipment. An active plan of disposal is being carried out, and sale is highly probable within the following year. The assets’ carryi

> McLaughlin Novelty Corp. (McLaughlin) developed an unusual product, electric clip-on eyeglass wipers. McLaughlin felt the product would appeal to hikers, joggers, and cyclists who engaged in their sports in rainy climates. Because retail establishments w

> A company sells books through the Internet. The company obtains the books from the publishers and carries them in inventory for immediate shipment. Customer payment is by credit card. 2. An interior design company operates a showroom. Furniture manufactu

> Statement of financial position, statement of comprehensive income data, and additional information are provided below for Supreme Co. Additional information: 1. Purchased a capital asset, $9,000; payment by issuing 600 common shares. 2. Payment at matur

> Refer to the data in A5-6. Required: Prepare the complete SCF, in good form, using the direct method in the operating activities section. Include the required note disclosure of non-cash transactions. Omit the separate disclosure of cash flow for interes

> Grand Corp.’s 20X2 financial statements reflect the following: Additional information: During the year, equipment with an original cost of $82,000 was sold for cash. Required: 1. Prepare the SCF in good form using the indirect method fo

> The financial statements for Totten Limited are shown below: During the year, the company purchased a capital asset valued at $30,000; payment was made by issuing common shares. Additional capital assets were acquired for cash. Unexplained changes in acc

> Statement of financial position balances as at 31 December 20X8 and 20X9 are provided below for Laurel Inc. Laurel Inc. additional information: - Net earnings for 20X9 were $712,000. - Equipment with an original cost of $400,000 and a NBV of $150,000 was

> The records of Rangler Paper Co. reflect the select data provided below for the reporting period ended 31 December 20X5. Required: Prepare the SCF using the indirect method for operating activities. Group all changes in non-cash working capital in operat

> Ronald Corp. is a privately owned candy maker. The graph below provides information on cash flow activities for Ronald Corp. for the eight-year period 20X2 to 20X9. Required: Interpret the results of the graph and explain the nature of Ronald Corp.â

> Graphs for two companies, Ming Ltd. and Tom Ltd., are provided below, showing comparisons of net earnings and cash flows over a period of time. Required: Interpret the graphs and conclude, with an explanation, on which company appears to have a better qu

> On 13 September 20X1, Nitish Corp.’s board of directors moved the company’s operations into a newly constructed building and declared its old building available for sale. The original cost of the old building was $20 million; it was 40% depreciated. Othe

> Account balances, taken from the ledger of Argot Flooring Ltd. as of 31 December 20X5, appear below. Additional information: 1. Store supplies were counted at 31 December and found to be valued at $5,600. 2. Depreciation of building and equipment is over

> The records of Agricola Corp. provide information about transactions and events of the year. Select information is provided below. 1. Sold equipment for $172,000 cash; original cost, $720,000, accumulated depreciation, $420,000. 2. Repaid a bank loan, pa

> You are presented with the following data from Jake Doyle Inc. for the year ended 31 December 20X1. Additional information: 1. Sold property, plant, and equipment for cash. Cost of the assets was $236,000; net book value was $76,000. 2. Purchased equipme

> The records of Koop Co. provided the following information for the year ended 31 December 20X8: Additional information: 1. Sold equipment for cash (cost, $30,000; accumulated depreciation, $18,000). 2. Purchased land, $40,000 cash. 3. Acquired land for $

> Return to the facts of A5-24. Required: 1. Prepare the operating activities section of the SCF incorporating ASPE classification and policy decisions. Include supplemental disclosure of interest paid, income tax paid, and dividend revenue received. Tax p

> Return to the facts of A5-17. Required: 1. Prepare the operating activities section of the SCF, using the indirect method of presentation, but incorporating separate disclosure of income tax paid and interest paid within the operating activities section.

> Return to the facts of A5-16. Required: 1. Prepare the operating activities section of the SCF, using the indirect method of presentation but incorporating separate disclosure of income tax paid and interest paid within the operating activities section.

> The SCF for Wave Electronics Ltd., using the indirect method of presentation for operating activities, is shown below. Required: 1. Some of the items included in operating activities above may be presented in other sections of the SCF. Explain the altern

> The SCF for MacLaren Supplies Ltd., using the direct method of presentation for operating activities, is shown below. Required: 1. Some of the items included in operating activities, above, may be presented in other sections of the SCF. Explain the alter

> Information related to various financial statement items is provided for three cases: Case A Tax expense was $341,400. The deferred tax liability had an opening balance of $92,000 and a closing balance of $103,000. Income tax payable declined by $22,400

> The accounting records of Food Complex Ltd., a publicly listed company, showed the amounts below for the year ended 31 January 20X7, in millions of Canadian dollars. The company had 40 million common shares outstanding throughout the fiscal year. Require

> Todd Corp. reported the following in its 20X4 financial statements: Required: 1. Prepare the SCF using the indirect method. Assume that unexplained changes in the accounts are caused by logical transactions. Omit separate disclosure of cash paid for inte

> The following data was derived from the accounting records of NewFort Ltd. at year-end, 31 December 20X9: Additional information: 1. Sold plant assets for cash; cost, $252,000; two-thirds depreciated. 2. Purchased plant assets for cash. 3. Purchased plan

> The main sections of the SCF are shown below with letter identification. Next, several transactions are given. Match the transactions with the SCF sections by entering one or more letters in each blank space. Assume loans and notes receivable are long-te

> Mackey Ltd. reported the following selected balances: Additional information: 1. There was a stock dividend of $25,000 on common shares and a cash dividend of $35,000. 2. Of the preferred shares, $50,000 were retired for cash, and $75,000 were converted

> The following select information is available for Jones & Co. Ltd., for the year ended 31 December 20X8: Additional information: 1. Equipment with an original cost of $100,000 was sold for cash. 2. Other equipment was purchased for cash. 3. There is

> Shown below are the statements of comprehensive income, the comparative statements of financial position, and additional information useful in preparing the 20X5 SCF for Remote Company. Additional information: 1. Equipment costing $66,000 with a book val

> Financial statements for Diamond Company are as follows: Additional information: 1. The company sold equipment that had an original cost of $584,000 and a net book value of $247,600. Other equipment was purchased for cash. Patent amortization was $8,000.

> Information related to capital assets is provided for three cases: The company sold an asset with an original cost of $120,000 at a loss of $8,000. Total depreciation expense for the period was $50,000. Other capital assets were acquired for cash. The co

> Minex Corp. owns a number of mine sites, and is involved in exploration, extraction, and refining. Output is sold under long-term contracts, where prices are set, but extraction and exploration decisions are influenced by commodity prices. Operating acti

> Golf Ltd. owns a chain of golf courses. Members sign multi-year membership packages, with increasing payments in later years of the contract. Revenue is recognized evenly over the membership term, regardless of the cash flow pattern. Operating activities

> The accounting records of Wireless Digital Inc., a publicly listed company, showed the amounts below for the year ended 31 December 20X2: Required: Prepare a single-step statement of income and comprehensive income by: 1. Nature of the expense 2. Functio

> Dromeda Ltd. has prepared the following comparison (in thousands): The same information has been collected for Panel Corp.: Required: 1. Which of the companies above illustrates higher quality of earnings? Explain. 2. Suggest four factors that would make

> The accounting records of Laurent Co. reflect the following data: Additional information: 1. Paid a $24,000 long-term note payable by issuing common shares. 2. Purchased capital assets that cost $99,000; gave a $72,000 long-term note payable and paid $27

> The following financial information is available for Suza Inc. for the 20X3 fiscal yea: Additional information: 1. Marketable securities were sold at their carrying value. The marketable securities are not cash equivalents. 2. A partially depreciated bui

> The records of Neon Corp. provided the following data: 1. Purchased a capital asset for $340,000; paid cash. 2. Depreciation expense is $134,000. 3. Sold a capital asset for $68,000 cash; original cost was $180,000, accumulated depreciation is $140,000.

> The Atlantic Refinery Corp. (ARC) is a public company headquartered in St. John’s, Newfoundland. On 31 December 20X5, the post-closing trial balance included the following accounts (in thousands of Canadian dollars): The following trans

> On 31 December 20X2, the balances of Argon Enterprises Inc.’s shareholders’ equity accounts were as follows (all are credit balances): Capital stock $303,000 Contributed surplus 6,000 Retained earnings 121,000 Currency

> Listed below are some financial statement classifications coded with letters and, below them, selected transactions and/or account titles. A Earnings/loss from continuing operations B Earnings/loss from discontinued operations C Other comprehensive inco

> Akerman Techonology Corp. is preparing its SFP at 31 December 20X5. The following items are under consideration: 1. Rent received in advance for the first quarter of 20X6, $20,000. 2. Note payable, long-term, $100,000. This note was issued on 1 July 20X5

> The consolidated SFP of Mutron Lock Inc. is shown below. MUTRON LOCK INC. Consolidated Statement of Financial Position As of 31 December 20X5 Required: For each of items (a) through (k) in the SFP above, calculate the amount that should appear.

> Acrimony Ltd. has the following balances in its general ledger on 31 December 20X8 (in thousands of Canadian dollars): Required: Prepare, in good form, a statement of income and comprehensive income. Use a continuous format.

> Amana Cement Corp. is a private corporation controlled by Amin Amana. The company’s adjusted trial balance and other related data at 31 December 20X5 are given below. Although the company uses some obsolete terminology, the amounts are

> The most recent SFP of Blackstone Tire Corp., a private corporation, appears below: BLACKSTONE TIRE CORPORATION Statement of Financial Position For the year ended 31 December 20X5 Asset Current Cash $ 23,000 Short-term investments 10,000 Accounts receiva

> Prime Essentials Ltd. is a small private corporation. The owner plans to approach the bank for an additional loan or a line of credit to facilitate expansion. The company bookkeeper, after discussion with the owner of the company, has prepared the follow

> Rutgers e-Terminal Ltd. is a private corporation wholly owned by Mr. Adonis Rutgers. Mr. Rutgers also personally owns 40% of the common shares of a company named Princeton Corp. A further 20% of the Princeton common shares are held by Rutgers e-Terminal

> The following trial balance was prepared by Vantage Electronics Corp., a Canadian private enterprise, as of 31 December 20X5. The adjusting entries for 20X5 have been made, except for any related to the specific information noted below. Other information

> Below are select account names and balances from Junior Corp.’s general ledger: Required: 1. Calculate Junior Corp.’s current ratio. 2. Calculate Junior Corp.’s quick ratio. 3. Calculate Junior Corp.&

> Juncture Corp. uses the following accounts in its general ledger and all currently have balances: Juncture Corp.—Select Accounts from the General Ledger Cash in bank Petty cash Treasury bills J. Patent J. Patent—accumulated amortization M. Patent M. Pate

> The chapter provides various examples of SFPs, such as in Exhibit 4-2 and 4-3, which you should review carefully to understand what an SFP prepared in good form looks like. Required: 1. Provide three explanations on how the SFP is useful from the perspec

> The SFP of a junior Canadian gold-mining company reports the following amounts (in $thousands): Assets Current Assets Cash and cash equivalents $ 8,260 Accounts receivable, less allowance for doubtful accounts 20,338 Taxes recoverable 200 Inventori

> The SFP of Karmax Ltd. discloses the following assets: The following information has been established in relation to market values (amounts in thousands of dollars): Note 1 The long-term investment is an investment in the common shares of a company owned

> Identify whether the following items in comprehensive income will be reclassified to net income or not reclassified.

> Abriel Ltd., a public company, has the following accounts in its year-end 20X5 trial balance: 1. Dividends payable. 2. Restricted cash balance in Abriel’s bank, being held by the bank for a bank loan that will come due in early 20X7. 3. Loss on repurchas

> The following disclosure note appeared in the 31 December 20X5 financial statements of Dridell Corporation, a manufacturer of electronic equipment: Dridell is exposed to liabilities and compliance costs arising from its past and current generation, manag

> The following disclosure note is from the 31 October 20X2 financial statements of GreenWorld Ltd., a mining company: The preparation of the financial statements, in conformity with generally accepted accounting principles, requires management to make est

> The following disclosure note is from the 31 December 20X4 financial statements of Riconda Ltd.: The company operates one operating segment, that being the design, manufacture, and sale of graphics and multimedia products for personal computers and consu

> Union Carbolics Inc. has five operating segments. Segment operating data (in millions of Canadian dollars) for the year 20X6 are as follows: Required: Identify which of these five segments are reportable segments under IFRS. Indicate the grounds on which

> The auditor has completed her work on the financial statements of Leslie Kwok Inc. (LKI) for the year ended 31 December 20X7. The auditor signed her audit opinion on 5 March 20X8; LKI’s board of directors has not yet approved the statements. The followin

> Northern Switching Ltd. (NSL) is a manufacturer of digital switching equipment and systems. The company has total assets of approximately $784 million. Each of the following events occurred after the end of NSL’s 20X8 fiscal year, but before the statemen

> Zero Growth Ltd. has completed financial statements for the year ended 31 December 20X6. The financial statements have yet to be finalized or issued. The following events and transactions have occurred: 1. The office building housing administrative staff

> Unlimited Possibilities Ltd. (UPL) is finalizing the financial statements for 20X5. The company’s managers are uncertain how each of the following events and situations should be reported: 1. UPL is the guarantor on a $10 million bank loan that was obtai

> Note disclosures provide the following information: 1. Explain the accounting policies that the company is using. 2. Provide additional detail for financial statement components. 3. Identify major underlying assumptions and estimates. 4. Provide informat

> Identify whether the following items belong in comprehensive income or net income.

> Indicate whether each statement is true or false. If the statement is false, provide a brief explanation of why it is false. 1. A disclosed basis of accounting is GAAP. 2. An audit opinion can be provided on a disclosed basis of accounting. 3. A disclose

> Ruan Corp. discovered in 20X9 that it had been overestimating the number of products that would be received for warranty service in Product Line A. Product Line A had been introduced in 20X7 and even though quality assurance checks had been conducted ext

> Dashall Ltd. has the following accounts in its year-end 20X7 trial balance: 1. Retained earnings. 2. Investment in shares of another company as a temporary use of cash to earn a return. 3. Deferred income tax asset. 4. Note payable for equipment, payable

> 1. Rela Corp. changes its estimate of the useful life of one of its pieces of machinery. Using the previous estimate, the depreciation expense in the current year would have been $15,000 and in applying the revised estimated useful life, the current year

> Mellie Inc. has never recorded an allowance for doubtful accounts. Due to worsening economic conditions, credit losses are determined to be material in the current year. Mellie Inc. sets up an allowance for doubtful accounts for outstanding receivables o

> Moncton Developments Ltd. was established in early 20X2. During the first three years, the company followed the policy of expensing its development costs rather than capitalizing and amortizing them. It did so because in the early stages of the company&a

> Hannam Co. decided to change from the declining-balance method of depreciation to the straight-line method effective 1 January 20X7. The following information was provided: The company has a 31 December year-end. The tax rate is 20%. No dividends were de

> In May 20X5, the newly appointed controller of Butch Baking Corp. conducted a thorough review of past accounting, particularly of transactions that exceeded the company’s normal level of materiality. As a result of his review, he instru

> On 23 November 20X7, when engaged in preparing for the 20X7 fiscal year-end, the chief accountant of Harper Ltd. discovered two accounting errors in the 20X5 statements: 1. A government ministry had paid $4.5 million in partial settlement of an amount du

> Po-Yen Devices Inc. and Kejia Computer Ltd. are competing businesses. Selected data from the financial statements for the two companies for the year ended 31 December 20X2 are shown below. Required: 1. Compute the following ratios for both companies (for

> Refer to the data in A4-8. Assume that the assets of Argon Enterprises Inc. totalled $1,980,000 at the end of 20X1, $1,750,000 at year-end 20X2, and $2,120,000 at year-end 20X3. Required: 1. Assume you are analyst for a private equity firm. Determine th

> Identify each of the following statements as true or false. 1. ASPE and IFRS both require comprehensive income. 2. Held-for-sale assets are classified as current assets in ASPE and noncurrent assets in IFRS. 3. Both ASPE and IFRS may have non-controlling

> The following information is available for three independent companies: Required: 1. Solve the missing numbers in the table. 2. Prepare a statement of retained earnings in good form for Company Carole. 3. If Company Carole is a public enterprise, is it a

> The following is select information provided for Penvin Corporation for the year ended December 31, 20X2: Penvin Corporation’s income tax rate is 35%. Required: 1. Prepare a partial statement of changes in equity for Penvin Corporation.

> Consider each of the following separate situations that arose in 20X1: 1. Corporation G invested $70,000 in corporate bonds as a short-term investment. The year-end 20X1 market value of the bonds is $63,000. The bonds are measured at fair value every rep

> Golf Inc. is a public company that has been in business since the 1980s. It owns and operates over 40 golf courses across Canada. It also owns and operates pro shops and dining facilities. On 1 November 20X4 GI announced it was going to sell three of its

> Haliteck Corp. is based in Halifax. At the end of 20X4, the company’s accounting records show the following items: 1. A $100,000 loss from hurricane damage. 2. Total sales revenue of $2,600,000, including $400,000 in the Decolite division, for which the

> The following information pertains to Junction Ltd. Corporation: - Income from continuing operations: $1,203,000 - Loss from discontinued operations: $126,000 - Gain on sale from discontinued operations: $24,400 - Net foreign exchange gain (loss) on tran

> 1. Using the information contained in A3-5, prepare: 1.A continuous SCI 2.A separate statement of income and statement of comprehensive income Data from A3-5: Quebecor Inc. is a major provider of cable services and also the owner of many newspapers. The

> Quebecor Inc. is a major provider of cable services and also the owner of many newspapers. The company reported the following items in its 20X1 financial statements (in millions of Canadian dollars, except per-share amounts): a. Revenues $4,206.6 b. Cost

> The information below pertains to the operations of Montreal Retail Corporation for the year ended 31 December 20X6: Cost of merchandise sold $102,000 Inventory warehousing cost 20,000 Accounts payable 120,000 Sales revenue 525,000 Accumulated depreciati

> The following items were taken from the adjusted trial balance of the Bremeur Corp. on 31 December 20X5. Assume an average 20% income tax on all items (including the divestiture loss). The accounting period ends 31 December. All amounts given are pre-tax

> Identify each of the following statements as true or false. 1. All companies are required to provide basic and diluted EPS calculations. 2. Public companies are required to provide EPS calculations before and after a discontinued operation. 3. Basic EPS

> Ceti Co. sells environmentally friendly coffee cups through an online store. The company is owned by Ceti Kadi. The following transactions took place over the first two years of operations: 20X1 Purchased 8,000 units for resale at $9 each 20X1 Purchased

> Mytel Corporation owns and operates a variety of restaurants, hotels, and budget lodging. In June 20X8, the management of Mytel Corporation decided to sell off its budget lodging operations, as the rate of return on the division’s assets was lower than m

> You have been asked to prepare the financial statements for Neema Corp., a private Canadian corporation, for the year ended 31 December 20X4. The company began operations in early 20X4. The following information is available about its business activities

> Return to A3-18 and assume instead that Mira Products is a private company reporting in accordance with ASPE. How would the reorganization affect Mira’s 20X4 financial reporting? Data from A3-18: Leos Janacek is CEO and controlling shareholder of Mira P

> Cayman Islands–based Harris Corp. is in the beauty industry. The company develops and produces a wide range of products for hair and skin care. The products are sold both at wholesale (through professional beauty supply stores) and retail (through variou