Question: The Hurricane Lamp Company forecasts that next

The Hurricane Lamp Company forecasts that next year’s sales will be $6 million. Fixed operating costs are estimated to be $800,000, and the variable cost ratio (that is, variable costs as a fraction of sales) is estimated to be 0.75. The firm has a $600,000 loan at 10 percent interest. It has 20,000 shares of $3 preferred stock and 60,000 shares of common stock outstanding. Hurricane Lamp is in the 40 percent corporate income tax bracket.

a. Forecast Hurricane Lamp’s earnings per share (EPS) for next year. Develop a complete income statement using the revised format illustrated in Table 14.1. Then determine what Hurricane Lamp’s EPS would be if sales were 10 percent above the projected $6 million level.

b. Calculate Hurricane Lamp’s degree of operating leverage (DOL) at a sales level of $6 million using the following:

i. The definitional formula (Equation 14.1)

Equation 14.1:

ii. The simpler, computational formula (Equation 14.2)

Equation 14.2:

iii. What is the economic interpretation of this value?

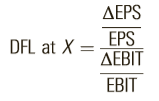

c. Calculate Hurricane Lamp’s degree of financial leverage (DFL) at the EBIT level corresponding to sales of $6 million using the following:

i. The definitional formula (Equation 14.3)

Equation 14.3:

ii. The simpler computational formula (Equation 14.4)

Equation 14.4:

iii. What is the economic interpretation of this value?

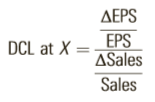

d. Calculate Hurricane Lamp’s degree of combined leverage (DCL) using the following:

i. The definitional formula (Equation 14.5)

Equation 14.5:

ii. The simpler computational formula (Equation 14.7)

Equation 14.7:

iii. The degree of operating and financial leverage calculated in Parts b and c

iv. What is the economic interpretation of this value?

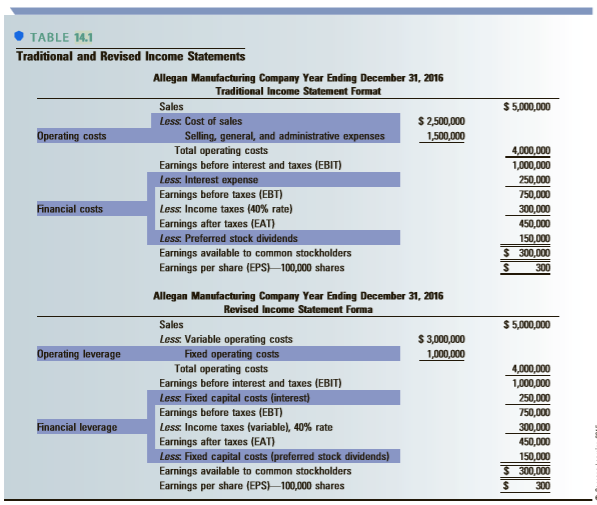

Table 14.1:

Continue to next pages………

Transcribed Image Text:

AEBIT EBIT ASales Sales DOL at X Sales – Variable costs DOL at X : EBIT ΔΕPS EPS AEBIT DFL at X = EBIT EBIT DFL at X EBIT – | – Dp/(1 – T) Dp/(1 – T) AEPS DCL at X =_EPS ASales Sales Sales – Variable costs DCL at X : EBIT – I – Dp/(1 – T) TABLE 14.1 Traditional and Revised Income Statements Allegan Manufacturing Company Year Ending December 31, 2016 Traditional Income Statement Format Sales $ 5,000,000 Less. Cost of sales $ 2,500,000 Operating costs Selling, general, and administrative expenses Total operating costs Earnings before interest and taxes (EBIT) Less. Interest expense Earnings before taxes (EBT) Less. Income taxes (40% rate) Earnings after taxes (EAT) 1,500,000 4,000,000 1,000,000 250,000 750,000 Financial costs 300,000 450,000 150,000 $ 300,000 Less. Preferred stock dividends Earnings available to common stockholders Earnings per share (EPS)-100,000 shares 300 Allegan Manufacturing Company Year Ending December 31, 2016 Revised Income Statement Forma $ 5,000,000 Sales Less. Variable operating costs $3,000 Operating leverage Fixed operating costs Total operating costs Earnings before interest and taxes (EBIT) Less. Fixed capital costs (interest) Earnings before taxes (EBT) Less: Income taxes (variable), 40% rate Earnings after taxes (EAT) Less: Fixed capital costs (prefered stock dividends) 1,000,000 4,000,000 1,000,000 250,000 750,000 300,000 450,000 Financial leverage 150,000 $ 300,000 Earnings available to common stockholders Earnings per share (EPS)-100,000 shares 300

> Referring to Table 13.2, calculate the market value of firm L (without a corporate income tax) if the equity amount in its capital structure decreases to $5,000 and the debt amount increases to $5,000. At this capital structure, the cost of equity is 15

> What other factors besides operating leverage can affect a firm’s business risk?

> Explain the difference between business risk and financial risk.

> What is arbitrage? How is it used in deriving the proposition that the value of a firm is independent of its capital structure?

> What role does signaling play in the establishment of a firm’s capital structure?

> What assumptions are required in deriving the proposition that a firm’s cost of capital is independent of its capital structure?

> Explain why, according to the pecking order theory, firms prefer internal financing to external financing.

> According to the pecking order theory, if additional external financing is required, which type of securities should a firm issue first? Last?

> Describe two techniques that a company can use to hedge against transaction exchange risk.

> What is the asymmetric information concept? What role does this concept play in a company’s decision to change its financial structure or issue new securities?

> What is the relationship between the value of a firm and its capital structure, given the existence of a corporate income tax, bankruptcy costs, and agency costs?

> What is the relationship between the value of a firm and its capital structure without a corporate income tax? With a corporate income tax?

> Explain the research results of Modigliani and Miller in the area of capital structure.

> National Value Foods Company (NVFC) is considering opening a new wholly owned subsidiary in Booneville. To finance this investment, NVFC is considering two financing plans: (1) sell 600,000 shares of common stock at $20 each; or (2) sell 200,000 shares

> Rauchous Resources has traditionally been financed in a most conservative way. The CEO and founder, Rebecca, just does not believe in debt. However, after hearing a consultant discuss the concept of an optimal capital structure, she began to consider new

> Ellington’s Cabaret is planning a major expansion that will require $95 million of new financing. Ellington’s currently has a capital structure consisting of $400 million of common equity (with a cost of 14 percent and 4 million shares outstanding), $50

> EBITDA Inc. a subsidiary of Robinson Enterprises, is considering the purchase of a fleet of new BMWs for the CEO and other senior managers. Currently the firm has a capital structure that consists of 60 percent debt, 30 percent common equity, and 10 perc

> University Technologies, Inc. (UTI) has a current capital structure consisting of 10 million shares of common stock, $200 million of first-mortgage bonds with a coupon interest rate of 13 percent, and $40 million of preferred stock paying a 5 percent div

> Waco Manufacturing Company has a cash (and marketable securities) balance of $150 million. Free cash flows during a projected one-year recession are expected to be $200 million with a standard deviation of $200 million. (Assume that free cash flows are a

> What is covered interest arbitrage?

> Next year’s EBIT for the Latrobe Company is approximately normally distributed with an expected value of $8 million and a standard deviation of $5 million. The firm’s marginal tax rate is 40 percent. Fixed financial charges (interest payments) next year

> Bowaite’s Manufacturing has a current cash and marketable securities balance of $50 million. The company’s economist is forecasting a two-year recession. Free cash flows during the recession, which are normally distributed, are expected to total $70 mill

> Lassiter Bakery currently has 3 million shares of common stock outstanding that sell at a price of $25 per share. Lassiter also has $10 million of bank debt outstanding at a pretax interest rate of 12 percent and a private placement of $20 million in bon

> The Oakland Shirt Company has computed its indifference level of EBIT to be $500,000 between an equity financing option and a debt financing option. Interest expense under the debt option is $200,000 and $100,000 under the equity option. The EBIT for the

> Jenkins Products has a current capital structure that consists of $50 million in longterm debt at an interest rate of 10 percent and $40 million in common equity (10 million shares). The firm is considering an expansion program that will cost $10 million

> The Bullock Cafeteria Corporation has computed the indifference point between debt and common equity financing options to be $4 million of EBIT. EBIT is approximately normally distributed with an expected value of $4.5 million and a standard deviation of

> The Anaya Corporation is a leader in artificial intelligence research. Anaya’s present capital structure consists of common stock (30 million shares) and debt ($250 million with an interest rate of 15%). The company is planning an expansion and wishes to

> High Sky Inc., a hot-air balloon manufacturing firm, currently has the following simplified balance sheet: The company is planning an expansion that is expected to cost $600,000. The expansion can be financed with new equity (sold to net the company $4

> Morton Industries is considering opening a new subsidiary in Boston, to be operated as a separate company. The company’s financial analysts expect the new facility’s average EBIT level to be $6 million per year. At this time, the company is considering t

> Two capital goods manufacturing companies, Rock Island and Davenport, are virtually identical in all aspects of their operations—product lines, amount of sales, total size, and so on. The two companies differ only in their capital struc

> What is the theory of interest rate parity?

> Emco Products has a present capital structure consisting only of common stock (10 million shares). The company is planning a major expansion. At this time, the company is undecided between the following two financing plans (assume a 40 percent marginal t

> Kaufman Industries expects next year’s operating income (EBIT) to equal $4 million, with a standard deviation of $2 million. The coefficient of variation of operating income is equal to 0.50. Interest expenses will be $1 million, and preferred dividends

> Scherr Corporation’s current EPS is $5.00 at a sales level of $10 million. At this sales level, EBIT is $2 million. Scherr’s DCL has been estimated to be 2.0 at the current level of sales. Sales are forecast to have an expected value of $11 million next

> Walker’s Gunnery, a small arms manufacturer, has current sales of $10 million and operating income (EBIT) of $450,000. The degree of operating leverage for Walker is 2.5. Next year’s sales are expected to increase by 5 percent. Walker has found that, ove

> Earnings per share (EPS) for Valcor Inc. are $3 at a sales level of $2 million. If Valcor’s degree of operating leverage is 2.0 and its degree of combined leverage is 8.0, what will happen to EPS if operating income increases by 3 percent?

> McGonnigal Inc. has expected sales of $40 million. Fixed operating costs are $5 million, and the variable cost ratio is 65 percent. McGonnigal has outstanding a $10 million, 10 percent bank loan and $3 million in 12 percent coupon-rate bonds. McGonnigal

> Connely Inc. expects sales of silicon chips to be $30 million this year. Because this is a very capital-intensive business, fixed operating costs are $10 million. The variable cost ratio is 40 percent. The firm’s debt obligations consist of a $2 million,

> Cohen’s Bowling Emporium has a degree of financial leverage of 2.0 and a degree of combined leverage of 6.0. The breakeven sales level for Cohen’s has been estimated to be $500,000. Fixed costs total $250,000. What effect will a 15 percent increase in sa

> A firm has sales of $10 million, variable costs of $5 million, EBIT of $2 million, and a degree of combined leverage of 3.0. a. If the firm has no preferred stock, what are its annual interest charges? b. If the firm wishes to reduce its degree of comb

> Blums Inc. expects its operating income over the coming year to equal $1.5 million, with a standard deviation of $300,000. Its coefficient of variation is equal to 0.20. Blums must pay interest charges of $700,000 next year and preferred stock dividends

> Rank in order of priority (highest to lowest) the following claims on the proceeds from the liquidation of a bankrupt firm: • Taxes owed to federal, state, and local governments • Preferred stockholders • Common stockholders • Expenses of administeri

> A firm has earnings per share of $2.60 at a sales level of $5 million. If the firm has a degree of operating leverage of 3.0 and a degree of financial leverage of 5.5 (both at a sales level of $5 million), forecast earnings per share for a 2 percent sale

> McGee Corporation has fixed operating costs of $10 million and a variable cost ratio of 0.65. The firm has a $20 million, 10 percent bank loan and a $6 million, 12 percent bond issue outstanding. The firm has 1 million shares of $5 (dividend) preferred s

> Given the following information for Computech, compute the firm’s degree of combined leverage (dollars are in thousands except EPS): 2015 2016 Sales $ 500,000 $ 570,000 Fixed costs 120,000 120,000 Variable costs 300,000 342,000 Ear

> Albatross Airlines’ fixed operating costs are $5.8 million, and its variable cost ratio is 0.20. The firm has $2 million in bonds outstanding with a coupon interest rate of 8 percent. Albatross has 30,000 shares of preferred stock outstanding, which pays

> Show algebraically that Equation 14.2: is equivalent to Equation 14.1: Sales - Variable costs DOL at X = EBIT ДЕВІТ EBIT ASales DOL at X = Sales

> Gibson Company sales for the year 2016 were $3 million. The firm’s variable operating cost ratio was 0.50, and fixed costs (that is, overhead and depreciation) were $900,000. Its average (and marginal) income tax rate is 40 percent. Currently, the firm h

> The Alexander Company reported the following income statement for 2016: Sales…………………………………………………………………………………………..$15,000,000 Less: Operating expenses Wages, salaries, benefits……………………………………………………………….$ 6,000,000 Raw materials.………………………………………………………………

> What is cash insolvency analysis, and how can it help in the establishment of an optimal capital structure?

> Why do public utilities typically have capital structures with about 50 percent debt, whereas major oil companies average about 25 percent debt in their capital structures?

> Explain how a firm that has failed can be reorganized to operate successfully.

> Describe some of the measures used by companies to discourage unfriendly takeover attempts.

> Under what circumstances should a firm use more debt in its capital structure than is used by the average firm in the industry? When should it use less debt than the average firm?

> In practice, how can a firm determine whether it is operating at (or near) its optimal capital structure?

> What are the major limitations of EBIT-EPS analysis as a technique to determine the optimal capital structure?

> Is it possible for a firm to have a high degree of combined leverage and a low level of total risk? Explain.

> Is it possible for a firm to have a high degree of operating leverage and a low level of business risk? Explain.

> How is a firm’s degree of combined leverage (DCL) related to its degrees of operating and financial leverage?

> Define the following: a. Operating leverage b. Financial leverage

> Define and give examples of the following: a. Fixed costs b. Variable costs

> Define leverage as it is used in finance.

> What issues of business ethics may be involved in the establishment of a firm’s dividend payment amounts?

> In connection with reorganization plans, what do fairness and feasibility mean?

> You are the holder of common stock in the G. Lewis Apartment Renovation Company. Historically, the firm has paid generous cash dividends. The firm has recently announced that it would replace its cash dividend with a 20 percent annual stock dividend. Is

> What effect do share repurchases (undertaken as part of the firm’s dividend decision) have on the value of the firm?

> What are the tax limitations on the practice of share repurchases as a regular dividend policy?

> Why do many firms choose to issue stock dividends? What is the value of a stock dividend to a shareholder?

> What is a dividend reinvestment plan? Explain the advantages of a dividend reinvestment plan to the firm and to shareholders.

> Some people have suggested that it is irrational for a firm to pay dividends and sell new stock in the same year because the cost of newly issued equity is greater than the cost of retained earnings. Do you agree? Why or why not?

> Under what circumstances would it make sense for a firm to borrow money to make its dividend payments?

> Why do many managers prefer a stable dollar dividend policy to a policy of paying out a constant percentage of each year’s earnings as dividends?

> How can the passive residual view of dividend policy be reconciled with the tendency of most firms to maintain a constant or steadily growing dividend payment record?

> What role do most practitioners think dividend policy plays in determining share values?

> What are the differences between Chapter 7 and Chapter 11 of the Bankruptcy Reform Act?

> In the theoretical world of Miller and Modigliani, what role does dividend policy play in the determination of share values?

> Explain what is meant by the signaling effects of dividend policy.

> Explain what is meant by the informational content of dividend policy.

> Explain what is meant by the clientele effect.

> What other “external” factors limit a firm’s ability to pay cash dividends?

> What aspects of U.S. tax laws tend to (a) encourage and (b) discourage large dividend payments by corporations? Explain how.

> What legal constraints limit the amount of cash dividends that may be paid by a firm?

> Under what condition or conditions, if any, might a firm find it desirable to borrow funds from a bank or other lending institution in order to take a cash discount?

> Determine the effect of each of the following conditions on the annual financing cost for a line of credit arrangement (assuming that all other factors remain constant): a. The bank raises the prime rate. b. The bank lowers its compensating balance req

> What savings are realized when accounts receivable are factored rather than pledged?

> Explain why an informal settlement may be preferable to declaring bankruptcy for both the failing firm and its creditors.

> Explain why banks normally include a “cleanup” provision in a line of credit agreement.

> Explain why the annual financing cost of secured credit is frequently higher than that of unsecured credit.

> Explain the difference between a floating lien and a trust receipts arrangement.

> Explain the differences between pledging and factoring receivables.

> What are some of the disadvantages of relying too heavily on commercial paper as a source of short-term credit?

> Explain the differences between a line of credit and a revolving credit agreement

> Define the following: a. Accrued expenses b. Deferred income c. Prime rate d. Compensating balance e. Discounted loan f. Commitment fee

> Under what condition or conditions is trade credit not a “cost-free” source of funds to the firm?

> Explain the difference between spontaneous and negotiated sources of short-term credit.

> How is the annual financing cost for a short-term financing source calculated? How does the annual financing cost differ from the true annual percentage rate?

> In a debt reorganization, explain the difference between a composition and an extension.

> Define and discuss the function of collateral in short-term credit arrangements.

> a. Which of the following working capital financing policies subjects the firm to a greater risk? i. Financing permanent current assets with short-term debt ii. Financing fluctuating current assets with long-term debt b. Which policy will produce the

> Why is no single working capital investment and financing policy necessarily optimal for all firms? What additional factors need to be considered in establishing a working capital policy?