Question: W&S Partners commenced the risk assessment

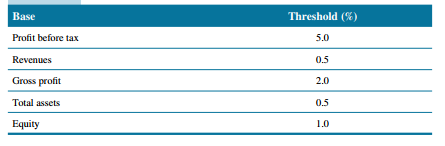

W&S Partners commenced the risk assessment phase of the Cloud 9 audit with procedures to gain an understanding of the client’s structure and its business environment. You have completed your research on the key market forces as they relate to Cloud 9’s operations. The topics you researched included the general and industry-specific economic trends and conditions; the competitive environment; product, customer, and supplier information; technological advances and the effect of the Internet; and laws and regulatory requirements. The purpose of this research is to identify the inherent risks. The auditor needs to identify which financial statement assertions may be affected by these inherent risks. Identifying the risks will help determine the nature of the audit procedures to be performed. Management implicitly or explicitly makes assertions regarding the recognition, measurement, presentation, and disclosure of the various elements of the financial statements. Auditors use assertions for account balances to form a basis for the assessment of risks of material misstatement. That is, assertions are used to identify the types of errors that could occur in transactions that result in the account balance. Consequently, further breaking down the account into these assertions will direct the audit effort to those areas of higher risk. The auditors broadly classify assertions as existence or occurrence; completeness; valuation or allocation; rights and obligations; and presentation and disclosure. An additional task during the risk assessment phase is to consider the concept of materiality as it applies to the client. The auditor will design procedures in order to identify and correct errors or irregularities that would have a material effect on the financial statements and affect the decision-making of the users of the financial statements. materiality is used in determining audit procedures and sample selections, and in evaluating differences between client records and audit results. It is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the base figure to be used to calculate materiality, an auditor should consider the key drivers of the business and ask, “What are the end users (that is, shareholders, banks, and so on) of the accounts going to be looking at?†For example, will shareholders be interested in profit figures that can be used to pay dividends and increase share price? W&S Partners’ audit methodology dictates that one planning materiality (PM) amount is to be used for the financial statements as a whole. Further, only one basis should be selected—a blended approach or average should not be used. The basis selected is the one determined to be the key driver of the business. W&S Partners use the percentages in table 4.12 as starting points for the various bases. These starting points can be increased or decreased by taking into account qualitative client factors, such as:

• the nature of the client’s business and industry (for example, rapidly changing through growth or downsizing, or because of an unstable environment)

• whether the client is a public company (or subsidiary of one) that is subject to regulations

• the knowledge of or high risk of fraud Typically, profit before tax is used; however, it cannot be used if reporting a loss for the year or if profitability is not consistent. When calculating PM based on interim figures, it may be necessary to annualize the results. This allows the auditor to plan the audit properly based on an approximate projected year-end balance. Then, at year end, the figure is adjusted, if necessary, to reflect the actual results.

Required:

Answer the following questions based on the information presented for Cloud 9 in Appendix A to this book and in the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters.

a. Using the December 31, 2020, trial balance (in Appendix A), calculate planning materiality and include the justification for the basis that you have used for your calculation.

b. Based on your knowledge of the client and its industry, discuss the inherent risks in the audit of Cloud 9. Identify the associated financial accounts that would be affected and provide an assessment of “high,†“medium,†or “low†in relation to the likelihood and materiality of the risk occurring.

Required:

Answer the following questions based on the information presented for Cloud 9 in Appendix A to this book and the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters.

a. Using analytical procedures and the information provided in the appendix, perform preliminary analytics of Cloud 9’s financial position and its business risks. Discuss the ratios indicating a significant or an unexpected fluctuation.

b. Which specific areas do you believe should receive special emphasis during your audit? Consider your discussion of the results of analytical procedures as well as your preliminary estimate of materiality. Prepare a memorandum to Suzie Pickering outlining potential problem areas (that is, where possible material misstatements in the financial report exist) and any other special concerns (for example, going concern). Specify the accounts and related assertions that would require particular attention

Transcribed Image Text:

Base Threshold (%) Profit before tax 5.0 Revenues 0.5 5 Gross profit 2.0 Total assets 0.5 Equity 1.0

> Tropical Cruises is a new client of MMM Partners. Tropical Cruises is a low-cost cruise ship operator, travelling between Canada and the United States. The planning for the first audit is under way. The auditors have become aware that police in two count

> The working paper in figure 5.11 was prepared by James Parkhill, a first-year accountant. Find seven errors that James made while completing this working paper. Figure 5.11: B D E F 1 New Millennium Ecoproducts 2 Year End: December 31, 2020 3 Cash

> Is it possible for Fellowes and Associates to use only accounts receivable confirmations as audit evidence and adhere to the mandatory requirements in CAS 230? Explain.

> Discuss the strengths and weaknesses of accounts receivable confirmations as audit evidence for HCHG.

> Featherbed Surf & Leisure Holidays Ltd. is a resort company based on Vancouver Island. Its operations include boating, surfing, diving, and other leisure activities; a backpackers’ hostel; a family hotel; and a five-star resort. Justin and Sarah Morris o

> Answer the following questions based on the information presented for Cloud 9 in Appendix A and in the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters. Required: Based on your conclusio

> Jennifer Daoust is reading the documents prepared by the members of the team working on the audit of receivables for a large client. Jennifer is the senior manager assisting the engagement partner, Ruby Rogers. Jennifer and Ruby have worked together on m

> Max Crowe is a junior auditor who has just started with the team conducting the audit of a new client in the construction industry. Max is “shadowing” Susan Wong, an experienced auditor. Susan is showing Max how to be a member of an audit team and is try

> Securimax Limited has been an audit client of KFP Partners for the past 15 years. Securimax is based in Waterloo, Ontario, where it manufactures high-tech armour-plated personnel carriers. Securimax often has to go through a competitive market tender pro

> Solar Tube Gen is a start-up company in the renewable energy sector. The founder, Fritz Herzberg, has developed cutting-edge technology to convert the energy in the sun’s rays to electricity via a novel system of mirrors designed to focus the sun’s rays

> Mohammad Amed is responsible for preparing bank reconciliations at Ajax Ltd. Ajax has many bank accounts, including separate accounts for each major branch, imprest accounts for salaries and dividends, and accounts kept in foreign currency for overseas d

> Conversations between the board of directors of Acme Ltd. and the engagement partner of the financial audit, Angelo Del Santo, have revealed that Acme uses three legal firms. Ball and Partners performs all legal work related to property transfers, mortga

> The audit program for the revenue account for a client has been drafted. The following item appears: Required: a. Does the procedure address the stated assertion? Explain. b. If your answer to part (a) is no, provide the correct assertion or suggest ad

> The audit program for the revenue account for a client has been drafted. The following item appears: Required: a. Does the procedure address the stated assertion? Explain. b. If your answer to part (a) is no, provide the correct assertion or explain wh

> The audit program for the revenue account for a client has been drafted. The following item appears: Required: a. Does the procedure address the stated assertion? Explain. b. If your answer to part (a) is no, provide the correct assertion or explain wh

> Yellow Aviation is an existing client of PPP Partners. The auditors are aware that the impact of a global economic slowdown on airlines has been severe, with predictions of a prolonged downturn. Also, as a result of the crisis along with the entry of new

> Answer the following questions based on the information presented for Cloud 9 in Appendix A to this book and in the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters. Sharon Gallagher and

> Atlantic Academy is a private school that offers education to children from Kindergarten to Grade 7. The school operates as a not-for-profit entity and oversight of the school is performed by the board of directors. The board reviews the operational and

> Ana Dinh used 0.5 to 5 percent of gross profit in determining materiality of $70,000 in her audit of XYZ Inc., a company that builds replacement engines for tractors and combines. She used the $70,000 amount as her planning materiality, identifying accou

> You are the audit supervisor of Seagull & Co and are currently planning the audit of your existing client, Eagle Heating Co., for the year ending December 31, 2020. Eagle manufactures and sells heating and plumbing equipment to a number of home improveme

> Triple J Movers Ltd. is owned by Jacques Tétreault. The company used to be profitable but several new small companies have started to compete with Triple J, offering very low prices that Triple J cannot match. Jacques thinks he can make his company profi

> This is the second year that your firm is auditing JJ Company, which is developing a new drug for a rare form of cancer. The company is controlled by Jack Mukash, who purchased the shares from the previous owner this year. You have been informed that the

> LLL Avionics Ltd. has contacted your accounting firm to inquire about the cost of an external audit. The company’s president explained that he feels that “the previous auditor charged too much and only issued a qualified opinion.” Your firm was recommend

> Clear Sky Aviation credits prepayments of air travel to a deferred revenue account until the travel service is provided, at which point it transfers the appropriate amount to sales revenue. A problem with its control system means that the proper allocati

> Comment on the audit strategy likely to be adopted for the audit of patient revenue for Gardens Nursing Home

> Identify the audit risks associated with the installation of the new IT system for patient revenue for Gardens Nursing Home.

> Cheap-as-Chips stocks thousands of items in inventory that range in value from $1 to $100. The inventory on hand represents a material portion of current assets. The merchandise items change according to the season and the promotional theme adopted by th

> Answer the following questions based on the information for Cloud 9 presented in Appendix A of this book and in the current and earlier chapters. You should also consider your answers to the case study questions in earlier chapters. Required: a. Conside

> Based on the background information, what are the major inherent risks in the Securimax audit? Consider both industry and entity risks in your answer.

> Featherbed Surf & Leisure Holidays Ltd. is a resort company based on Vancouver Island. Its operations include boating, surfing, diving, and other leisure activities; a backpackers’ hostel; a family hotel; and a five-star resort. Justin and Sarah Morris o

> Bright Spark Fashion has retail outlets in six large regional cities in eastern Canada. The shops are run by local managers but purchasing decisions for all stores are handled by Ray Bright, the owner of the business. Fashion is an extremely competitive

> Li Chen has calculated profitability ratios using data extracted from his client’s pre-audit trial balance. He also has the values for the same ratios for the preceding two years (using audited figures). Table 4.11 presents the data for

> You are the audit senior of Rhino & Co. and you are planning the audit of Kaine Construction Co. for the year ended March 31, 2020. Kaine specializes in building houses and provides a five-year building warranty to its customers. Your audit manager h

> Niagara Dairy is a boutique cheese maker based in the Niagara region of Ontario. Over the years, the business has grown by supplying local retailers and, eventually, by exporting cheese products. In addition, there is a “farm-gate” shop and café located

> Tom’s Trailers Ltd. (TTL), located in London, Ontario, manufactures industrial trailers that are used to ship goods across the country. Originally, Tom Tran owned 60 percent of the common shares of TTL and the other 40 percent was owned

> Gold Explorers Inc. is a major Canadian gold mining corporation. Gold Explorers has mines and development projects in Canada (Northern Ontario and British Columbia), the United States, and South America. Shares of Gold Explorers trade on three major inte

> Carl’s Computers imports computer hardware and accessories from China, Japan, Korea, and the United States. It has branches in every provincial capital, and the main administration office and central warehouse is in Montreal. There is a branch manager in

> Planning, performance, and specific materiality Challenging LO 2 Claytonhill Beverages Ltd. is 100-percent owned by Buzz Bottling. While the company has in the past been profitable, it incurred a loss for the year ended December 31, 2020. The parent comp

> W&S Partners will need the assistance of auditors in China and the United States and may need derivatives experts to complete the Cloud 9 audit. The other auditors will be asked to provide evidence about the inventory shipped to Canada from the productio

> Ajax Finance Ltd. provides small- and medium-sized personal, car, and business loans to clients. It has been operating for more than 10 years and run throughout its life by Bill Schultz. Bill has been the public face of the finance company, appearing in

> An airline company has been adversely impacted by a global economic slowdown and its effect on business travel. In addition to lower overall demand, the airline company faces increased competition from other airlines, which are heavily discounting flight

> Francine Rideau, controller of Quatco Company, is reviewing the year-end financial statements with Tonya Kowalski, the company president. The financial statements currently report a net income of $563,480. Tonya is applying for a very substantial bank lo

> Sisters Inc. beauty salon is a 100% subsidiary of Benefit Beauty Supply Inc., a beauty supply company. As a result of this relationship, there were several transactions between the two entities during the last year. Sisters rented retail space for its sa

> a. Identify and explain any significant fraud risk factors for Featherbed. b. For each fraud risk factor you identify, explain how the risk will affect your approach to the audit of Featherbed.

> You have access to the following information for Featherbed: • prior period financial statements • anticipated results for the current year • industry comparisons Required: Explain how you would use this information to understand your new client.

> Ivy Bishnoi is preparing a report for the engagement partner of an existing client, Scooter Ltd., an importer of scooters and other low-powered motorcycles. Ivy has been investigating certain aspects of Scooter’s business given the change in economic con

> Stokes Ltd. operates in the steel fabrication industry. Its business is organized into domestic and international sales and it has many clients in each area. It obtains most of its raw materials from two suppliers, both located in the same province as St

> Dunks Holdings Ltd. (Dunks) is an importer of hardware goods and distributes them to hardware retailers around the country. The growth in the do-it-yourself (DIY) market, which has accompanied the boom in house prices in most capital cities over the past

> Expansion Aviation has installed a new payroll module for its existing accounting system that integrates with the general ledger application. The new payroll application is more complex than the old system, but its reporting function provides more detail

> Armstrong, Aldrin & Collins Professional Corporation (AAC) operates a public accounting practice that is located in Woodstock, Ontario. AAC’s common shares are owned equally by its three shareholders, who are Chartered Professional

> McKesson & Robbins was a company at the centre of a famous fraud in the United States in the 1930s. Required: a. Research the facts of the McKesson & Robbins fraud and write a short description of the case. b Make a list of the defects in the company’s

> Farm Fresh Foods Inc. (FFF) is a new food distribution company that has been profitable since the second month of operations. It has arranged with Smith LLP, an accounting firm, to conduct an external audit of its first year of operations. FFF has a larg

> Discuss the factors to consider when determining preliminary materiality for Securimax. Questions 4.21 and 4.22 are based on the following case. Fellowes and Associates is a successful mid-tier accounting firm with a large range of clients across Canada.

> Required: Match the numbered situations below with one of the following types of audit sampling or sampling risk: a. Statistical sampling b. N on-statistical sampling c. Sampling risk d. Non-sampling risk 1. Rather than looking only for authorized si

> State the assertion that is violated in the following sentences: a. The client fails to accrue management bonuses in the current year. b. The client does not adjust its inventory to the lower of cost or market. c. The client books revenue in the current

> For each of the following items, identify the related assertion: a. Inventory is recorded at the lower of cost and net realizable value. b. All delivery vans recorded in the accounting records are owned by the entity c. All payroll-related accruals at ye

> For each of the following documents, state whether it would be located in the auditors’ permanent file or the current file. a. Articles of incorporation b. Bank confirmation for the current year c. Management representation letter for the current year d.

> What substantive tests apply to the existence and valuation assertions for investment balances?

> Explain why an unexpected change in the gross profit ratio leads the auditor to suspect a wide range of possible misstatements in recorded transactions and balances.

> It is increasingly common for companies to program their computer information system to print and distribute cheques without further authorization. As an auditor, describe controls you would expect to find in place over such a system.

> Hatami and Partners completed the field work for the December 31, 2020, audit of Harbinger Corporation on March 1, 2021. The financial statements and auditor’s report were issued and mailed to shareholders on March 15, 2021. Required: In each of the two s

> C. D. Hodgson and Associates Chartered Professional Accountants audited the financial statements of Tallender Company, a sporting goods retailer. As with all of his firm’s audits, Carl Hodgson conducted the Tallender audit in accordance with generally ac

> Shane White bone is getting to know his new client, Clarrie Potters, a large discount electrical retailer. Ben Brothers has been the engagement partner on the Clarrie Potters audit for the past five years, but the audit partner rotation rules have meant

> Identify the type of audit evidence being used in each situation described below: a. The auditor tests cash remittance advices to ensure that allowances and discounts are appropriate and that receipts are posted to the correct customer accounts in the ri

> Audit opinions Moderate LO 1, 5 Required What type of audit report would be appropriate in each of the following scenarios? Explain. a. There is uncertainty relating to a pending exceptional litigation matter that is adequately disclosed in the notes. b.

> Required: From the list below, identify what you would consider as a. an incentive for fraud, and b. an opportunity for fraud. 1. college or university tuition 2. gambling debts 3. the fact that nobody counts the inventory, so losses are not known 4. the

> Patrizia Montani is considering the sample size needed for a selection of sales invoices relating to the test of internal controls of the Caistor Company. She is determining the acceptable risk and deviation rates, and is considering two possible scenari

> There are several categories of control activities listed in this chapter. They include performance reviews, authorization controls, account reconciliations, physical controls, and segregation of duties. Required: For each of the following, identify the

> Overhead is to be absorbed into the cost of inventory on the basis of the normal level of activity. What evidence is available to the auditor in verifying management’s determination of that level of activity?

> What does “assurance” mean in the financial reporting context? What qualities must an “assurer” have in order for you to feel that their statement has high credibility?

> CAS 260 stresses the importance of communication with “those charged with governance.” Who are these people and why is it important that the auditor communicate with them (and not others)?

> Explain the difference between limitation of scope and disagreement with those charged with governance.

> What is “modified wording” in an audit report? What are the different types of modified wording and when are they used?

> Ajax Ltd. is a listed company and a new client of Delaware Partners, a medium-sized audit firm. Jeffrey Nycz is the engagement partner on the audit and has asked the members of the audit team to start the process of gaining an understanding of the client

> Why do audit reports contain paragraphs outlining (a) management’s responsibility for the financial statements and (b) the auditor’s responsibility for the financial statements? What is contained in these paragraphs?

> What options does an auditor have when material errors are found? Do these options vary for current-year misstatements and prior-year misstatements?

> Explain the difference between the two types of subsequent events. Discuss the auditor’s responsibility for detecting subsequent events (a) prior to the completion of field work, (b) prior to signing the audit report, and (c) between the date of the audit

> What procedures must the auditor perform to search for contingent liabilities?

> What is the accounting assumption of “going concern”? Why is it of interest to auditors?

> What matters does an auditor communicate at the end of an audit to those charged with governance? Why are these matters important?

> List and describe the elements in the/the process/engagement wrap-up process. Why is important?

> Explain the financial reporting principle underlying the audit verification of the existence and completeness assertions with respect to entities consolidated into group financial statements.

> When inspecting securities on hand, what things should the auditor observe?

> Explain lapping. Describe appropriate audit procedures to perform where it is suspected.

> Sax Co. sells insurance, and it has recently become a listed company. In accordance with corporate governance guidelines, the finance director of Sax is reviewing the company’s corporate governance practices. Bill Bassoon is the chair of Sax. Bill vacate

> Outline the procedures involved in verifying the bank reconciliation.

> Describe the procedures for counting cash on hand.

> Explain why it is important to trace transfers between bank accounts on either side of the end of the reporting period.

> Explain why the balance of cash on hand and at bank is always audited, and why a substantive approach is preferred.

> Describe procedures to be undertaken where group entities are audited by other auditors.

> Explain the use and audit of imprest accounts.

> What steps can the auditor take to ensure that the disposal of fully depreciated assets is properly recorded? What are the implications if such assets are retained in the accounts?

> What are the problems confronting the auditor in verifying both the rate and method of depreciation?

> Discuss procedures that would be useful in ensuring that all disposals of property, plant, and equipment have been recorded.

> Why does the auditor usually adopt a substantive audit strategy for property, plant, and equipment assertions?

> A new client, an oil and gas explorer in Western Canada, is currently negotiating a loan worth $3 million to avoid defaulting on its long-term debt that is due in three months. Its latest quarterly earnings report indicated the entity has a working capit

> Discuss the cut-off implications of the inventory count being before or after the year end and closing inventory being determined by adjusting the count by reference to purchases and sales records in the intervening period.

> Many companies use standard costing as the basis for inventory costing. What audit procedures may be appropriate for establishing the fairness of the standard costs, for testing the maintenance of the standard cost records, and for determining the dispos

> What steps should the auditor perform when observing the inventory count? Why should the auditor take test counts?

> When conducting tests of details of transactions for property, plant, and equipment, there are three types of transactions that need to be substantiated. These transactions are additions, disposals, and repairs and maintenance. Briefly describe what is in