Question: You can use the computer-based Electronic

You can use the computer-based Electronic Workpapers on the textbook website to prepare the schedule of interbank transfers required in this problem.

EverReady Corporation is in the home building and repair business. Construction business has been in a slump, and the company has experienced financial difficulty over the past two years. Part of the problem lies in the company’s desire to avoid laying off its skilled crews of bricklayers and cabinetmakers. Meeting the payroll has been a problem.

The auditors are engaged to audit the 2017 financial statements. Knowing of EverReady’s financial difficulty and its business policy, the auditors decided to prepare a schedule of interbank transfers covering the 10 days before and after December 31, which is the

Company’s balance sheet date.

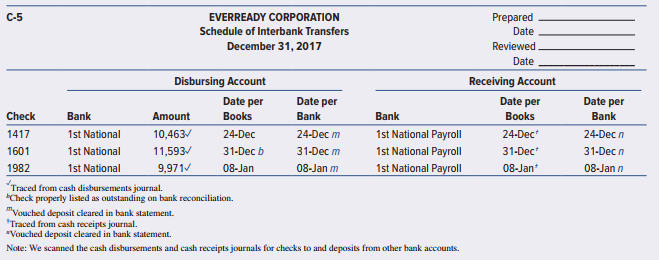

First, the auditors used the cash receipts and disbursements journals to prepare part of the schedule shown in Exhibit 6.52.1. They obtained the information for everything except the dates of deposit and payment in the bank statements (disbursing date per bank and receiving date per bank). The auditors learned that EverReady always transferred money to the payroll account at 1st National Bank from the general account at 1st National Bank. This transfer enabled the bank to clear the payroll checks without delay. The only bank accounts in the EverReady financial statements are the two at 1st National Bank.

Next, the auditors obtained the December 2017 and January 2018 bank statements for the general and payroll accounts at 1st National Bank. They recorded the bank disbursement and receipt dates in the schedule of interbank transfers. For each transfer, these dates are identical because the accounts are in the same bank. An alert auditor noticed that the 1st National Bank general account bank statement also contains deposits received from Citizen National Bank and canceled check 1799 dated January 5 payable to Citizen National Bank. This check cleared the 1st National Bank account on January 8 and was marked “transfer of funds.†This led to the auditors’ decision to inquire about this of EverReady’s chief financial officer.

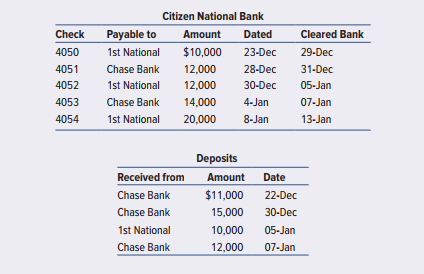

Asked about the Citizen National Bank transactions, EverReady’s chief financial officer readily admitted the existence of an off-books bank account. He explained that it was used for financing transactions in keeping with normal practice in the construction industry. He gave the auditors the December and January bank statements for the account at Citizen National Bank. In it, the auditors found the following:

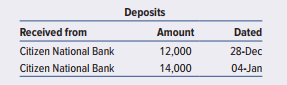

When asked about the Chase Bank transactions, EverReady’s chief financial officer admitted the existence of another off-books bank account, which he said was the personal account of the principal stockholder. He explained that the stockholder often used it to finance EverReady’s operations. He gave the auditors the December and January bank statements for this account at Chase Bank; in it, the auditors found the following:

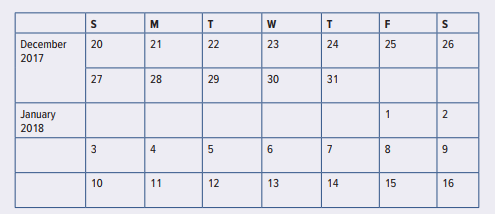

An abbreviated calendar for the period is in Exhibit 6.52.2.

Required:

a. Complete the Schedule of Interbank Transfers (document C-5, Exhibit 6.54.1) by entering the new information.

b. What is the actual cash balance for the three bank accounts combined, considering only the amounts given in this case information as of December 31, 2017 (before any of the December 31 payroll checks are cashed by employees)? As of January 8, 2018 (before any of the January 8 payroll checks are cashed by employees)?

Transcribed Image Text:

С-5 EVERREADY CORPORATION Prepared Schedule of Interbank Transfers Date December 31, 2017 Reviewed . Date Disbursing Account Receiving Account Date per Date per Date per Date per Check Bank Amount Books Bank Bank Bank Books 24-Dec 31-Dec 08-Jan 1417 1st National 10,463/ 24-Dec 24-Dec m 1st National Payroll 24-Dec n 1601 1st National 11,593/ 31-Dec b 31-Dec m 1st National Payroll 31-Dec n 9,971/ 1st National Payroll 08-Jan n 1982 1st National 08-Jan 08-Jan m Traced from cash disbursements journal. Check properly listed as outstanding on bank reconciliation. "Vouched deposit cleared in bank statement. "Traced from cash receipts journal. *Vouched deposit cleared in bank statement. Note: We scanned the cash disbursements and cash receipts journals for checks to and deposits from other bank accounts. Citizen National Bank Payable to Check Amount Dated Cleared Bank 4050 1st National $10,000 23-Dec 29-Dec 4051 Chase Bank 12,000 28-Dec 31-Dec 4052 1st National 12,000 30-Dec 05-Jan 4053 Chase Bank 14,000 4-Jan 07-Jan 4054 1st National 20,000 8-Jan 13-Jan Deposits Amount Received from Date Chase Bank $11,000 22-Dec Chase Bank 15,000 30-Dec 1st National 10,000 05-Jan Chase Bank 12,000 07-Jan M W F December 20 21 22 23 24 25 26 2017 27 28 29 30 31 January 2018 1 2 3 4 6 7 9. 10 11 12 13 14 15 16 co

> Cash receipts from sales on account have been misappropriated. Which of the following acts would conceal this defalcation and be least likely to be detected by an auditor? a. Understating the sales journal. b. Overstating the accounts receivable control

> Cash receipts from sales on account have been misappropriated. Which of the following acts would conceal this defalcation and be least likely to be detected by an auditor? a. Understating the sales journal. b. Overstating the accounts receivable control

> When an audit team does not receive a response on a positive accounts receivable confirmation, a second request. b. Do nothing for immaterial balances. c. Examine shipping documents. d. Examine client correspondence files.

> The best way to enact a broad fraud prevention program is to a. Install airtight control systems of checks and supervision. b. Name an “ethics officer” who is responsible for receiving and acting on fraud tips. c. Place dedicated hotline telephones on wa

> Write-offs of doubtful accounts should be approved by a. The salesperson. b. The credit manager. c. The treasurer. d. The cashier.

> When an audit team traces a sample of shipping documents to the related sales invoice copies, they are trying to find relevant evidence that a. Shipments to customers were invoiced. b. Shipments to customers were recorded as sales. c. Recorded sales were

> The negative request form of accounts receivable confirmation is useful particularly when the Assessed Level of Risk of Material Number of Small Balances Is Proper Consideration by the Recipient Is Misstatement Relating to Receivables Is a. Low Many

> When accounts receivable are confirmed at an interim date, auditors need not be concerned with a. Obtaining a summary of receivables transactions from the interim date to the year-end date. b. Obtaining a year-end trial balance of receivables, comparing

> In the audit of accounts receivable, the most important emphasis should be on the a. Completeness assertion. b. Existence assertion. c. Rights and obligations assertion. d. Presentation and disclosure assertion.

> When a sample of customer accounts receivable is selected for vouching debits, auditors will vouch them to a. Sales invoices with shipping documents and customer sales invoices. b. Records of accounts receivable write-offs. c. Cash remittance lists and b

> Why should a list of cash remittances be made and sent to the accounting department? Wouldn’t it be easier to send the cash and checks to the accountants so they can enter the credits to customers’ accounts accurately?

> Confirmation of individual accounts receivable balances directly with debtors will, of itself, normally provide the strongest evidence concerning the a. Collectability of the balances confirmed. b. Ownership of the balances confirmed. c. Existence of the

> Confirmation of individual accounts receivable balances directly with debtors will, of itself, normally provide the strongest evidence concerning the a. Collectability of the balances confirmed. b. Ownership of the balances confirmed. c. Existence of the

> Upon receipt of customers’ checks in the mail room, a responsible employee should prepare a remittance list that is forwarded to the cashier. A copy of the list should be sent to the a. Internal auditor to investigate the list for unusual transactions. b

> When auditing with “fraud awareness,” auditors should especially notice and follow up employee activities under which of these conditions? a. The company always estimates the inventory but never takes a complete physical count. b. The petty cash box is a

> You have identified relevant controls for several assertions within the revenue cycle, and you must use IDEA to perform several tests of controls. Required: a. ELM has a policy of using prenumbered customer order forms to help control for the completene

> For this exercise, your client, Bright IDEAs Inc., has provided you with data for two related files, a listing of sales invoices, and a listing of customers with credit limits. To test whether credit authorization controls are in place, the auditor must

> The following article was published in Newsday on February 9, 2009: Call for Probe of Ticket Sales Bruce Springsteen fans were victims of a “classic bait and switch” scam by the nation’s largest concert ticket seller, Senator Charles Schumer said yester

> The following four questions are taken from an internal control questionnaire. For each question, state (a) one test of controls procedure you could use to find out whether the control technique was really functioning and (b) what error or fraud could oc

> The following narrative description of a company’s cash receipts and billing system is in the auditors’ audit files: Rural Building Supplies Inc. is a single-store retailer that sells a variety of tools, garden supplies, lumber, small appliances, and ele

> The study and evaluation of management risk mitigation control is not easy. First, auditors must determine the risks and the controls subject to audit. Then they must find a standard by which performance of the control can be evaluated. Next they must sp

> You are the director of internal auditing of a large municipal hospital. You receive monthly financial reports prepared by the accounting department, and your review of them has shown that total accounts receivable from patients has steadily and rapidly

> What is the basic sequence of activities in the cash collection process?

> Your firm has audited the Rock Island Quarry Company for several years. Rock Island’s main revenue comes from selling crushed rock to construction companies from several quarries owned by the company in Illinois and Iowa. The rock is priced by weight, qu

> You are using computer audit software to prepare accounts receivable confirmations during the annual audit of the Eastern Sunrise Services Club. The company has the following data files: Master file—debtor credit record. Master file—debtor name and addre

> What can an auditor find using net worth analysis? Expenditure analysis?

> This case is designed like the ones in the chapter. Your assignment is to write the “audit approach” portion of the case, organized around these sections: Objective. Express the objective in terms of the facts supposedly asserted in financial records, ac

> Each morning the controller gets the prior day’s list of remittances, a copy of the payment report, and a copy of the deposit slip returned from the bank. When comparing these items, the controller would be able to determine that a. No checks were return

> Which of the following might be detected by auditors’ cutoff review and examination of sales journal entries for several days prior to the balance sheet date? a. Lapping year-end accounts receivable. b. Inflating sales for the year. c. Kiting bank balanc

> L. King, CPA, is auditing the financial statements of Cycle Company, a client that has receivables from customers arising from the sale of goods in the normal course of business. King is aware that the confirmation of accounts receivable is a generally a

> Exhibit 7.64.1 contains an arrangement of examples of transaction errors (lettered a–g) and a set of client control procedures and devices (numbered 1–15). Required: For each client control procedure numbered 1–15, write a test of controls that could pro

> Exhibit 7.64.1 contains an arrangement of examples of transaction errors (lettered a–g) and a set of client control procedures and devices (numbered 1–15). Required: For each error/control objective, identify the asse

> Exhibit 7.64.1 contains an arrangement of examples of transaction errors (lettered a–g) and a set of client control procedures and devices (numbered 1–15). Make a copy of the exhibit page and complete the following requirements. Required a. Opposite the

> The case below tells the actual story of a cash embezzlement scheme. The case has two major parts: (1) problem and (2) audit approach. For the case, please consider how the auditor may have discovered the cash embezzlement scheme. Problem Albert owned a

> Take a closer look at Exhibit 6.3 given below, Is there anything wrong with the bank statement? What are some ways to tell whether any of the amounts have been altered? 27 XFirst RepublicBank FIRST REPUBLICBANK AUSTIN, N.A. ACCOUNT P.0. BOX 908 60401

> The case below tells the actual story of a cash embezzlement scheme. The case has two major parts: (1) problem and (2) audit approach. For the case, please consider how the auditor may have discovered the cash embezzlement scheme. Problem The petty cash

> Which audit procedures are usually the most useful for auditing the existence assertion?

> An audit client sells 15 to 20 units of product annually. A large portion of the annual sales occur in the last month of the fiscal year. Annual sales have not materially changed over the past five years. Which of the following approaches would be most e

> Assume you have received a message from an informant regarding the following case. Your assignment is to write the “audit approach” portion of the case. a. Write a brief explanation of desirable controls, missing controls, and especially the kinds of “de

> You can use the computer-based Electronic Workpapers on the textbook website to prepare the net worth analysis required in this problem. Net worth analysis is performed when fraud has been discovered or is strongly suspected and the information to calcul

> Immediately upon receipt of cash, a responsible employee should a. Record the amount in the cash receipts journal. b. Prepare a remittance listing. c. Update the subsidiary accounts receivable records. d. Prepare a deposit slip in triplicate.

> Expenditure analysis is used when fraud has been discovered or strongly suspected and the information to calculate a suspect’s income and expenditures can be obtained (e.g., asset and liability records, bank accounts). Expenditure analysis consists of es

> The following are some “suspicions”; you have been requested to select some effective extended procedures designed to confirm or deny the suspicions. Required: Write the suggested procedures for each case in definite terms so another person can know wha

> Consider the following story of an actual embezzlement. This was the ingenious embezzler’s scheme: (a) He hired a print shop to print a private stock of Ajax Company checks in the company’s numerical sequence. (b) In his job as an accounts payable clerk

> Consider the following scenario: Adam worked for the local hardware store as an outside sales representative. His job was to visit local companies and contractors in an attempt to identify their needs for tools and materials and provide a bid to supply t

> Suppose you are auditing cash disbursements and discover several payments to a company you are unfamiliar with and cannot find information about this company on the Internet or in the local telephone directory. The invoices from this company have numbers

> How can you tell whether the amount on a check was altered after it was paid by a bank?

> What is the difference between a normal procedure and an extended procedure?

> Caulco Inc. is the audit client. The February bank statement is shown in Exhibit 6.3Â in the text. You have obtained the client-prepared bank reconciliation as of February 28 (see the following). Required: Check 2231 was the first check writt

> You can use the computer-based Electronic Audit Documentation on the textbook’s website to prepare the proof of cash required in this problem. The auditors of Steffey Ltd., decided to study the cash receipts and disbursements for the month of July of the

> Auditors typically will find the items lettered A–F in a client-prepared bank reconciliation. Required: Assume these facts: On October 11, the auditor received a cutoff bank statement dated October 7. The September 30 deposit in trans

> You are the auditor for Konerko’s Office Supply Store, which is opening for business next week. The store owner has established all the controls you have recommended for ensuring that sales are recorded properly and cash is accounted for. The owner has h

> Which of the following is an effective audit procedure that an auditor might use to detect kiting between intercompany banks? a. Review the composition of authenticated deposit slips. b. Review subsequent bank statements. c. Prepare a schedule of the ban

> You are the in-charge auditor examining the financial statements of the Gutzler Company for the year ended December 31. During late October, with the help of Gutzler’s controller, you completed an internal control questionnaire and prep

> Taylor, a CPA, has been engaged to audit the financial statements of University Books, Incorporated. University Books maintains a large cash fund exclusively for the purpose of buying used books from students for cash. The cash fund is active all year be

> The Runge Controls Corporation manufactures and markets electrical control systems: temperature controls, machine controls, burglar alarms, and the like. The company acquires electrical and semiconductor parts from outside vendors and assembles systems i

> Fraud risk factors are events or conditions that indicate I. An incentive or pressure to perpetrate fraud. II. An opportunity to carry out the fraud. III. An attitude or rationalization that justifies the fraudulent action. Which of the following stateme

> How can a proof of cash reveal unrecorded cash deposit and cash payment transactions?

> Is there anything odd about these two situations? (a) A check to Larson Electric Supply was endorsed with “Larson Electric” above the signature of “Eloise Garfunkle.” (b) Numerous checks were issued and dated December 25, January 1, and July 4.

> Incorporating elements of unpredictability in the selection of audit procedures to be performed by auditors include all of the following except a. Varying the timing of the audit procedures. b. Selecting items for testing that have lower amounts or are o

> In what way can audit procedures be modified to address assessed fraud risks? a. Obtain more reliable information. b. Perform procedures close to year-end. c. Apply computer-assisted techniques to all items. d. All of these are valid modifications.

> If the auditor believes that a misstatement is or might be intentional and the effect on the financial statements could be material or cannot be readily determined, the auditor should do which of the following? a. Inquire of management as to the possibil

> Which of these arrangements of duties could most likely lead to an embezzlement or theft? a. The inventory warehouse manager has responsibility for making the physical inventory observation and reconciling discrepancies to the perpetual inventory records

> Allison Everhart, an employee in accounts payable, believes she can run a fictitious invoice through the accounts payable system and collect the money. She knows payments are subject to an audit. Which account would be the best place to hide the fraud? a

> Which of the following combinations is a good way to conceal employee fraud but an ineffective means of perpetrating management (financial reporting) fraud? a. Overstating sales revenue and overstating customer accounts receivable balances. b. Overstatin

> Fraud risk factors are events or conditions that indicate which of the following? a. An opportunity to carry out a fraud. b. An attitude or rationalization that justifies a fraudulent action. c. An incentive or pressure to perpetrate fraud. d. All of the

> Which of the following is least indicative of fraudulent activity? a. Numerous cash refunds have been made to different people at the same post office box address. b. Internal auditors cannot locate several credit memos to support reductions of customers

> A code of ethics is an important element of a fraud prevention program. Which of the following would diminish the effectiveness of a company’s code of conduct? a. The establishment of a chief ethics officer. b. The establishment of a hotline for reportin

> How does a schedule of interbank transfers show improper cash transfer transactions?

> Is capability required to commit a fraud? Is capability part of opportunity, or should it be considered a separate element of fraud?

> Give some examples of rationalizations that people have used to excuse fraud. Can you imagine using them?

> Which of the following control activities could prevent a paid disbursement voucher from being presented for payment a second time? a. Vouchers should be prepared by individuals who are responsible for signing disbursement checks. b. Disbursement voucher

> What conditions provide opportunities for employee fraud?

> What are some pressures that can cause honest people to contemplate fraud? List some egocentric and ideological pressures as well as economic ones.

> What does a fraud perpetrator look like? How does one act?

> What are the defining characteristics of employee fraud? Embezzlement?

> Which three events should generally have occurred prior to the recognition of sales revenue?

> Why do you think companies use revenue recognition as a primary means for inflating profits?

> Why is inherent risk for the existence assertion for accounts receivable often set higher than inherent risk for the completeness assertion?

> Why do auditors focus on revenue as a significant account and the occurrence of revenue as a relevant assertion in the revenue cycle?

> During an audit of cash, the auditor is most concerned with the management assertion of a. Existence. b. Rights and obligations. c. Valuation or allocation. d. Occurrence.

> Suppose that you selected a sample of customers’ accounts receivable and wanted to find supporting evidence for the entries in the accounts. Where would you go to vouch the debit entries? What would you expect to find? Where would you go to vouch the cre

> What is check kiting? How might auditors detect kiting?

> What is the basic sequence of activities and accounting in a revenue and collection cycle?

> In the case of Bill Often, Bill Early, what information might have been obtained from inquiries? From tests of controls? From observations? From confirmations?

> In the case of The Canny Cashier, name one control that could have revealed signs of the embezzlement

> What are the goals of dual-direction testing regarding an audit of the accounts receivable and cash collection system?

> What procedures should be performed to determine the adequacy of the allowance for doubtful accounts?

> What special care should be taken with regard to examining the sources (e.g., faxed copy) of accounts receivable confirmation responses?

> What are some justifications for not using confirmations of accounts receivable on a particular audit?

> Distinguish between positive and negative confirmations. Under what conditions would you expect each type of confirmation to be appropriate?

> What analytical procedures might be informative regarding the existence assertion?

> Which of the following control activities would best protect against the preparation of improper or inaccurate cash disbursements? a. All checks must be signed by an officer designated by the board of directors. b. All signed checks must be reviewed and

> What is a cutoff bank statement? How do auditors use it?

> In preparing for the audit of cash, the auditors perform analytical procedures concerning cash balances. Which of the following would be the best source of information for use in the estimate of cash? a. Prior-years’ balances. b. Management inquiry. c. C

> Which of the following would the auditor consider to be an incompatible operation if the cashier receives remittances? a. The cashier prepares the daily deposit. b. The cashier makes the daily deposit at a local bank. c. The cashier posts the receipts to

> Why is the Auditing Standards Board’s set of management assertions important to auditors? Do these assertions differ from those included in PCAOB standards? If so, how are they different?

> Which of the following would be considered an assurance engagement? a. Giving an opinion on a prize promoter’s claims about the amount of sweepstakes prizes awarded in the past. b. Giving an opinion on the conformity of the financial statements of a univ

> What is the concept of reasonable assurance? What are the key limitations of an internal control system?

> An auditor’s purpose in auditing the information contained in the pension footnote most likely is to obtain evidence concerning management’s assertion about a. Rights and obligations. b. Existence. c. Presentation and disclosure. d. Valuation.