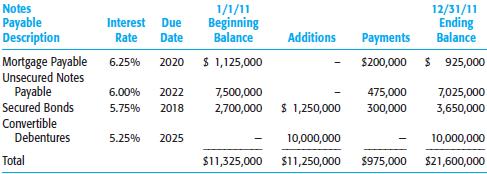

Question: Your client, Red Horse Inc., prepared the

Your client, Red Horse Inc., prepared the following schedule for long term debt for the audit of financial statements for the year ended December 31, 2011:

Required

a. What type of evidence would you examine to support the beginning balances in the accounts?

b. What types of evidence would you use to support the additions to each account?

c. What types of evidence would you examine to support payments?

d. What procedures would you perform related to the ending balances in the accounts?

e. What evidence would you use to verify interest rates and due dates?

f. How might you use the information presented above to audit interest expense and interest payable accounts?

Transcribed Image Text:

Notes Payable Description 1/1/11 Beginning Balance 12/31/11 Ending Balance Interest Due Date Rate Additions Payments Mortgage Payable Unsecured Notes Payable Secured Bonds Convertible Debentures 6.25% 2020 S 1,125,000 $200,000 $ 925,000 6.00% 2022 7,500,000 475,000 7,025,000 5.75% 2018 2,700,000 $ 1,250,000 300,000 3,650,000 5.25% 2025 10,000,000 10,000,000 Total $1,325,000 $11,250,000 $975,000 $21,600,000

> Explain why an auditor is interested in a client's future commitments to purchase raw materials at a fixed price.

> In the audit of the James Mobley Company, you are concerned about the possibility of contingent liabilities resulting from income tax disputes. Discuss the procedures you could use for an extensive investigation in this area.

> The following questions concern internal controls in the acquisition and payment cycle. Choose the best response. a. A client erroneously recorded a large purchase twice. Which of the following internal controls would be most likely to detect this error

> The cost accounting records are often an essential area to audit in a manufacturing or construction company. Required a. Why should the auditor review the cost accounting records and test their accuracy? b. For the audit of standard cost accounting reco

> Distinguish between a contingent liability and an actual liability and give three examples of each.

> Describe the purpose of a financial statement disclosure checklist and explain how it helps the auditor determine if there is sufficient appropriate evidence for each of the presentation and disclosure objectives.

> Identify and describe the four presentation and disclosure audit objectives.

> In your audit of Aviary Industries for calendar year 2011, you found a number of matters that you believe represent possible adjustments to the company's books. These matters are described below. Management's attitude is that "once the books are closed,

> Audit committees of public companies have many responsibilities in today's financial reporting environment. Visit the website of Microsoft Corporation (www.microsoft.com) and locate the Audit Committee's Charter under the "Investor Relations" link to ans

> The Check Clearing for the 21st Century Act (Check 21 Act) allows recipients of paper checks to create a digital image of the original check, eliminating the need for further handling of the actual check. The Federal Reserve Board has created a consumer

> In connection with an audit you are given the following work sheet: Checks Drawn but Not Paid by Bank No. Amount 573 ………………â

> The following are various potential misstatements due to errors or fraud (1 through 7), and a list of auditing procedures (a through h) the auditor would consider performing to gather evidence to determine whether the error or fraud is present. Possible

> In the audit of the Regional Transport Company, a large branch that maintains its own bank account, cash is periodically transferred to the central account in Cedar Rapids. On the branch account's records, bank transfers are recorded as a debit to the ho

> You are auditing general cash for the Pittsburgh Supply Company for the fiscal year ended July 31, 2011. The client has not prepared the July 31 bank reconciliation. After a brief discussion with the owner, you agree to prepare the reconciliation, with a

> The Frist Corporation has the following internal controls related to inventory: 1. The inventory purchasing system only allows purchases from pre-approved vendors. 2. The perpetual inventory system tracks the average number of days each inventory product

> Distinguish between FOB destination and FOB origin. What procedures should the auditor follow concerning acquisitions of inventory on an FOB origin basis near year-end?

> The following audit procedures are concerned with tests of details of general cash balances: 1. Obtain a standard bank confirmation from each bank with which the client does business. 2. Compare the balance on the bank reconciliation obtained from the cl

> The following are misstatements that might be found in the client's year-end cash balance (assume that the balance sheet date is June 30): 1. The outstanding checks on the June 30 bank reconciliation were under footed by $2,000. 2. A loan from the bank o

> The following questions deal with discovering fraud in auditing year-end cash. Choose the best response. a. Which of the following is one of the better auditing techniques to detect kiting? (1) Review composition of authenticated deposit slips. (2) Revi

> How will a company's bank reconciliation reflect an electronic deposit of cash received by the bank from credit card agencies making payments on behalf of customers purchasing products from the company's online Web site, but not recorded in the company's

> Explain why, in verifying bank reconciliations, most auditors emphasize the possibility of a nonexistent deposit in transit being included in the reconciliation and an outstanding check being omitted rather than the omission of a deposit in transit and t

> Why is there a greater emphasis on the detection of fraud in tests of details of cash balances than for other balance sheet accounts? Give two specific examples that demonstrate how this emphasis affects the auditor's evidence accumulation in auditing ye

> Distinguish between the verification of petty cash reimbursements and the verification of the balance in the fund. Explain how each is done. Which is more important?

> Assume that a client with excellent internal controls uses an imprest payroll bank account. Explain why the verification of the payroll bank reconciliation ordinarily takes less time than the tests of the general bank account, even if the number of disbu

> Distinguish between lapping and kiting. Describe audit procedures that can be used to uncover each.

> Items 1 through 8 are selected questions typically found in questionnaires used by auditors to obtain an understanding of internal control in the inventory and warehousing cycle. In using the questionnaire for a client, a "yes" response to a question ind

> When the auditor fails to obtain a cutoff bank statement, it is common to verify the entire statement for the month subsequent to the balance sheet date. How is this done and what is its purpose?

> In testing the cutoff of accounts payable at the balance sheet date, explain why it is important that auditors coordinate their tests with the physical observation of inventory. What can the auditor do during the physical inventory to enhance the likelih

> Explain the purpose of a four-column proof of cash. List two types of misstatements it is meant to uncover.

> What is meant by an imprest bank account for a branch operation? Explain the purpose of using this type of bank account.

> Why are auditors usually less concerned about the client's cash receipts cutoff than the cutoff for sales? Explain the procedure involved in testing for the cutoff for cash receipts.

> Describe what is meant by a cutoff bank statement and state its purpose.

> How do bank confirmations differ from positive confirmations of accounts receivable? Distinguish between them in terms of the nature of the information confirmed, the sample size, and the appropriate action when the confirmation is not returned after the

> Evaluate the effectiveness and state the shortcomings of the preparation of a bank reconciliation by the controller in the manner described in the following statement: "When I reconcile the bank account, the first thing I do is review the sorted list of

> Why is the monthly reconciliation of bank accounts by an independent person an important internal control over cash balances? Which individuals will generally not be considered independent for this responsibility?

> Explain the relationships among the initial assessed control risk, tests of controls and substantive tests of transactions for cash disbursements, and the tests of details of cash balances. Give one example in which the conclusions reached about internal

> The following questions concern testing the client's internal controls for inventory and warehousing. Choose the best response. a. When an auditor tests a client's cost accounting records, the auditor's tests are primarily designed to determine that (1)

> Explain the relationships among the initial assessed control risk, tests of controls and substantive tests of transactions for cash receipts, and the tests of details of cash balances.

> You are doing the first-year audit of Sherman School District and have been assigned responsibility for doing a four-column proof of cash for the month of October 2011. You obtain the following information: 6. Interest on a bank loan for the month of Oct

> It is less common to confirm accounts payable at an interim date than accounts receivable. Explain why.

> E-Antiques, Inc. is an Internet-based market maker for buyers and sellers of antique furniture and jewelry. The company allows sellers of antique items to list descriptions of those items on the E-Antiques Web site. Interested buyers review the Web site

> You are a CPA engaged in an audit of the financial statements of Pate Corporation for the year ended December 31, 2011. The financial statements and records of Pate Corporation have not been audited by a CPA in prior years. The stockholders' equity secti

> You are engaged in the audit of a corporation whose records have not previously been audited by you. The corporation has both an independent transfer agent and a registrar for its capital stock. The transfer agent maintains the record of stockholders and

> The following audit procedures are commonly performed by auditors in the verification of owners' equity: 1. Review the articles of incorporation and bylaws for provisions about owners' equity. 2. Analyze all owners' equity accounts for the year and docum

> Items 1 through 6 are common questions found in internal control questionnaires used by auditors to obtain an understanding of internal control for owners' equity. In using the questionnaire for a client, a "yes" response indicates a possible internal co

> The Redford Corporation took out a 20-year mortgage on June 15, 2011, for $2,600,000 and pledged its only manufacturing building and the land on which the building stands as collateral. Each month subsequent to the issue of the mortgage, a payment of $20

> The following covenants are extracted from the indenture of a bond issue. The indenture provides that failure to comply with its terms in any respect automatically makes the loan immediately due (the regular date is 20 years hence). List any audit steps

> The following questions concern internal controls in the inventory and warehousing cycle. Choose the best response. a. Which of the following controls will most likely justify a reduced assessed level of control risk for the occurrence assertion for purc

> The ending general ledger balance of $186,000 in notes payable for the Sterling Manufacturing Company is made up of 20 notes to eight different payees. The notes vary in duration anywhere from 30 days to 2 years, and in amounts from $1,000 to $10,000. In

> The following are frequently performed audit procedures for the verification of bonds payable issued in previous years: 1. Analyze the general ledger account for bonds payable, interest expense, and unamortized bond discount or premium. 2. Obtain a confi

> Distinguish between a vendor’s invoice and a vendor’s statement. Which document should ideally be used as evidence in auditing acquisition transactions and which for verifying accounts payable balances? Why?

> Items 1 through 6 are questions typically found in a standard internal control questionnaire used by auditors to obtain an understanding of internal control for notes payable. In using the questionnaire for a client, a "yes" response indicates a possible

> The following questions concern the audit of accounts in the capital acquisition and repayment cycle. Choose the best response. a. During an audit of a publicly held company, the auditor should obtain written confirmation regarding debenture transactions

> The following multiple choice questions concern interest-bearing liabilities. Choose the best response. a. The audit program for long-term debt should include steps that require the (1) Verification of the existence of the bondholders. (2) Examination o

> Explain the relationship between the audit of owners' equity and the calculations of earnings per share. What are the main auditing considerations in verifying the earnings per share figure?

> What should be the major emphasis in auditing the retained earnings account? Explain your answer.

> If a transfer agent disburses dividends for a client, explain how the audit of dividends declared and paid is affected. What audit procedures are necessary to verify dividends paid when a transfer agent is used?

> Assuming that the auditor properly documents receiving report numbers as a part of the physical inventory observation procedures, explain how the proper cutoff of purchases, including tests for the possibility of raw materials in transit, should be verif

> Evaluate the following statement: "The most important audit procedure to verify dividends for the year is a comparison of a random sample of cancelled dividend checks with a dividend list that has been prepared by management as of the dividend record dat

> What kinds of information can be confirmed with a transfer agent?

> Describe the duties of a stock registrar and a transfer agent. How does the use of their services affect the client's internal controls?

> How does the audit of owners' equity for a closely held corporation differ from that for a publicly held corporation? In what respects are there no significant differences?

> Explain why it is common for auditors to send confirmation requests to vendors with “zero balances” on the client’s accounts payable listing but uncommon to follow the same approach in verifying accounts receivable.

> What are the major internal controls over owners' equity?

> Evaluate the following statement: "The corporate charter and the bylaws of a company are legal documents; therefore, they should not be examined by the auditors. If the auditor wants information about these documents, an attorney should be consulted."

> What are the primary objectives in the audit of owners' equity accounts?

> List two types of restrictions long-term creditors often put on companies when granting them a loan. How can the auditor find out about these restrictions?

> Distinguish between (a) Tests of controls and substantive tests of transactions (b) Tests of details of balances for liability accounts in the capital acquisition and repayment cycle.

> Each employee for the Gedding Manufacturing Co., a firm using a job-cost inventory costing method, must reconcile his or her total hours worked with the hours worked on individual jobs using a job time sheet at the time weekly payroll time cards are prep

> What is the primary purpose of analyzing interest expense? Given this purpose, what primary considerations should the auditor keep in mind when doing the analysis?

> Why is it more important to search for unrecorded notes payable than for unrecorded notes receivable? Suggest audit procedures that the auditor can use to uncover unrecorded notes payable.

> Which analytical procedures are most important in verifying notes payable? Which types of misstatements can the auditor uncover by the use of these tests?

> The Ruswell Manufacturing Company applied manufacturing overhead to inventory at December 31, 2011, on the basis of $3.47 per direct labor hour. Explain how you will evaluate the reasonableness of total direct labor hours and manufacturing overhead in th

> Included in the December 31, 2011, inventory of the Wholeridge Supply Company are 2,600 deluxe ring binders in the amount of $5,902. An examination of the most recent acquisitions of binders showed the following costs: January 26, 2012, 2,300 at $2.42 ea

> List the major analytical procedures for testing the overall reasonableness of inventory. For each test, explain the type of misstatement that could be identified.

> Which internal controls should the auditor be most concerned about in the audit of notes payable? Explain the importance of each.

> Define what is meant by compilation tests. List several examples of audit procedures to verify compilation.

> Explain why a proper cutoff of purchases and sales is heavily dependent on the physical inventory observation. What information should be obtained during the physical count to make sure that cutoff is accurate?

> During the taking of physical inventory, the controller intention ally withheld several inventory tags from the employees responsible for the physical count. After the auditor left the client's premises at the completion of the inventory observation, the

> In the verification of the amount of the inventory, one of the auditor's concerns is that slow-moving and obsolete items be identified. List the auditing procedures that can be used to determine whether slow-moving or obsolete items have been included i

> What major audit procedures are involved in testing for the ownership of inventory during the observation of the physical counts and as a part of subsequent valuation tests?

> At the completion of an inventory observation, the controller requested the auditor to give him a copy of all recorded test counts to facilitate the correction of all discrepancies between the client's and the auditor's counts. Should the auditor comply

> Before the physical examination, the auditor obtains a copy of the client's inventory instructions and reviews them with the controller. In obtaining an understanding of inventory procedures for a small manufacturing company, these deficiencies are ident

> Explain why most auditors consider the receipt of goods and services the most important point in the acquisition and payment cycle.

> Many auditors assert that certain audit tests can be significantly reduced for clients with adequate perpetual records that include both unit and cost data. What are the most important tests of the perpetual records that the auditor must make before redu

> State what is meant by cost accounting records and explain their importance in the conduct of an audit.

> It is common practice to audit the balance in notes payable in conjunction with the audit of interest expense and interest payable. Explain the advantages of this approach.

> Explain the relationship between the acquisition and payment cycle and the inventory and warehousing cycle in the audit of a manufacturing company. List several audit procedures in the acquisition and payment cycle that support your explanation.

> Give the reasons why inventory is often the most difficult and time consuming part of many audits.

> You are assigned to the December 31, 2011, audit of Sea Gull Airframes, Inc. The company designs and manufactures aircraft superstructures and airframe components. You observed the physical inventory at December 31 and are satisfied that it was properly

> Since 1938, when auditors failed to uncover fictitious inventory recorded by the McKesson & Robbins Company, auditors have been ordinarily required to physically observe the counting of inventory. It is important to recognize that auditors are not requir

> During the first-year audit of Jones Wholesale Stationery, you observe that commission’s amount to almost 25 percent of total sales, which is somewhat higher than in previous years. Further investigation reveals that the industry typically has larger sal

> Archer Uniforms, Inc., is a distributor of professional uniforms to retail stores that sell work clothing to professionals, such as doctors, nurses, security guards, etc. Traditionally, most of the sales are to retail stores throughout the United States

> The following are various asset misappropriations involving the payroll and personnel cycle. 1. The payroll clerk submitted payroll information for a fictitious employee and had the funds directly deposited to a bank account that he controlled. 2. An emp

> You are assessing internal control in the audit of the payroll and personnel cycle for Rogers Products Company, a manufacturing company specializing in assembling computer parts. Rogers employs approximately two hundred hourly and thirty salaried employe

> What is meant by a voucher? Explain how its use can improve an organization’s internal controls.

> In comparing total payroll tax expense with that of the preceding year, Merlin Brendin, CPA, observed a significant increase, even though the total number of employees increased only from 175 to 185. To investigate the difference, he selected a large sam

> The Securities and Exchange Commission (SEC) found that Centerpulse Ltd., a publicly traded company based in Switzerland, fraudulently misstated its 2002 third and fourth quarter financial statements filed with the SEC. Visit the SEC’s website (www.sec.g

> The following audit procedures are typical of those found in auditing the payroll and personnel cycle: 1. Scan journals for all periods for unusual transactions to determine whether they are recorded correctly. 2. Select a sample of 40 entries in the pay

> The following misstatements are included in the accounting records of Lathen Manufacturing Company: 1. Joe Block and Frank Demery take turns “punching in” for each other every few days. The absent employee comes in at noon and tells his foreman that he h