Question: a. A material departure from generally accepted

a. A material departure from generally accepted accounting principles will result in auditor consideration of:

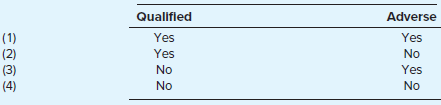

(1) Whether to issue an adverse opinion rather than a disclaimer of opinion.

(2) Whether to issue a disclaimer of opinion rather than a qualified opinion.

(3) Whether to issue an adverse opinion rather than a qualified opinion.

(4) Nothing, because none of these opinions is applicable to this type of exception.

b. The auditors’ report should be dated as of the date the:

(1) Report is delivered to the client.

(2) Auditors have accumulated sufficient appropriate evidence.

(3) Fiscal period under audit ends.

(4) Peer review of the working papers is completed.

c. In an audit report on combined financial statements, reference to the fact that a portion of the audit was performed by a component auditor is:

(1) Not to be construed as a qualification, but rather as a division of responsibility between the two CPA firms.

(2) Not in accordance with generally accepted auditing standards.

(3) A qualification that lessens the collective responsibility of both CPA firms.

(4) An example of a dual opinion requiring the signatures of both auditors.

d. Assume that the opinion paragraph of an auditors’ report begins as follows: “With the explanation given in Note 6, . . . the financial statements referred to above present fairly . . .†This is:

(1) An unmodified opinion.

(2) A disclaimer of opinion.

(3) An “except for†opinion.

(4) An improper type of reporting.

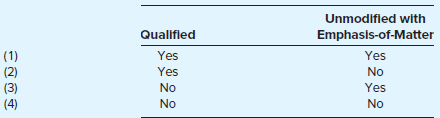

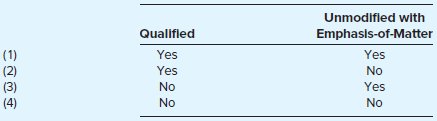

e. The auditors who wish to draw reader attention to a financial statement note disclosure on significant transactions with related parties should disclose this fact in:

(1) An emphasis-of-matter paragraph to the auditors’ report.

(2) A footnote to the financial statements.

(3) The body of the financial statements.

(4) The “summary of significant accounting policies†section of the financial statements.

f. What type or types of audit opinion are appropriate when financial statements are materially and pervasively misstated?

g. Which of the following ordinarily involves the addition of an emphasis-of-matter paragraph to an audit report of a nonpublic company?

(1) A consistency modification.

(2) An adverse opinion.

(3) A qualified opinion.

(4) Part of the audit has been performed by component auditors.

h. An audit report for a public client indicates that the audit was performed in accordance with:

(1) Generally accepted auditing standards (United States).

(2) Standards of the Public Company Accounting Oversight Board (United States).

(3) Generally accepted accounting principles (United States).

(4) Generally accepted accounting principles (Public Company Accounting Oversight Board).

i. An audit report for a public client indicates that the financial statements were prepared in conformity with:

(1) Generally accepted auditing standards (United States).

(2) Standards of the Public Company Accounting Oversight Board (United States).

(3) Generally accepted accounting principles (United States).

(4) Generally accepted accounting principles (Public Company Accounting Oversight Board).

j. When the matter is properly disclosed in the financial statements of a nonpublic company, the likely result of substantial doubt about the ability of the client to continue as a going concern is the issuance of which of the following audit opinions?

k. A nonpublic company’s change in accounting principles that the auditors believe is not justified is likely to result in which of the following types of audit opinions?

l. Which of the following is least likely to result in inclusion of an additional paragraph being added to an audit report?

(1) The company is a component of a larger business enterprise.

(2) An unusually important significant event.

(3) A decision not to confirm accounts receivable.

(4) A risk or uncertainty.

Transcribed Image Text:

Qualifled Adverse (1) (2) (3) (4) Yes Yes Yes No No Yes No No Unmodified with Qualifled Emphasis-of-Matter (1) (2) (3) (4) Yes Yes Yes No No Yes No No Unmodified with Qualified Emphasis-of-Matter (1) (2) (3) (4) Yes Yes Yes No No Yes No No

> During an audit engagement, Robert Wong, CPA, has satisfactorily completed an examination of accounts payable and other liabilities and now plans to determine whether there are any loss contingencies arising from litigation, claims, or assessments. What

> OA Company recently hired a payroll service provider to process its payroll—that service provider has essentially taken over the payroll function, and payroll represents OA’s largest expense. Comment on the following statement: OA’s auditors should make

> In your audit of the financial statements of Wolfe Company for the year ended April 30, you find that a material account receivable is due from a company in reorganization under Chapter 11 of the Bankruptcy Act. You also learn that on May 28 several form

> Valley Corporation established a stock option plan for its officers and key employees this year. Because the options granted have a higher option price than the stock’s current market price, the company has not recognized any cost for the options in the

> You are retained by Columbia Corporation to audit its financial statements for the fiscal year ended June 30. Your consideration of internal control indicates a fairly satisfactory condition, although there are not enough employees to permit an extensive

> Select the best answer for each of the following and explain fully the reason for your selection. a. Which of the following is least likely to be among the auditors’ objectives in the audit of inventories and cost of goods sold? (1) Det

> You are engaged in the audit of the financial statements of Armada Corporation for the year ended August 31, 20X0. The balance sheet, reflecting all your audit adjustments accepted by the client to date, shows total current assets, $8,000,000; total curr

> During your annual audit of Walker Distributing Co., your assistant, Jane Williams, reports to you that, although a number of entries were made during the year in the general ledger account Notes Payable to Officers, she decided that it was not necessary

> The only long-term liability of Range Corporation is a note payable for $1 million secured by a mortgage on the company’s plant and equipment. You have audited the company annually for the three preceding years, during which time the principal amount of

> Describe the audit steps that generally would be followed in establishing the propriety of the recorded liability for federal income taxes of a corporation you are auditing for the first time. Consideration should be given to the status of (a) the liabi

> During the course of any audit, the auditors are always alert for unrecorded accounts payable or other unrecorded liabilities. Required: For each of the following audit areas, (1) describe an unrecorded liability that might be discovered and (2) state w

> Early in your first audit of Star Corporation, you notice that sales and year-end inventory are almost unchanged from the prior year. However, cost of goods sold is less than in the preceding year, and accounts payable also are down substantially. Gross

> The subsequent period in an audit is the time extending from the balance sheet date to the date of the auditors’ report. Discuss the importance of the subsequent period in the audit of trade accounts payable.

> In the course of your initial audit of the financial statements of Sylvan Company, you determine that of the substantial amount of accounts payable outstanding at the close of the period, approximately 75 percent is owed to six creditors. You have reques

> Auditors usually send confirmations to obtain evidence about accounts receivable and accounts payable. a. Is confirmation presumptively required for accounts receivable, accounts payable, or both? b. Are accounts receivable requests, accounts payable req

> Shortly after you were retained to audit the financial statements of Case Corporation, you learned from a preliminary discussion with management that the corporation had recently acquired a competing business, the Mall Company. In your study of the terms

> Auditors report on the consistency of application of accounting principles. Assume that the following list describes changes that have a material effect on a client’s financial statements for the current year. (1) A change from the completed-contract me

> Your new client, Ross Products, Inc., completed its first fiscal year March 31, 20X4. During the course of your audit you discover the following entry in the general journal, dated April 1, 20X3. Required: Under these circumstances, what steps should

> Allen Fraser was president of three corporations: Missouri Metals Corporation, Kansas Metals Corporation, and Iowa Metals Corporation. Each of the three corporations owned land and buildings acquired for approximately $500,000. An appraiser retained by F

> Kadex Corporation, a small manufacturing company, did not use the services of independent auditors during the first two years of its existence. Near the end of the third year, Kadex retained Jones & Scranton, CPAs, to perform an audit for the year ended

> Gruen Corporation is a large diversified company with a large amount of property, plant, and equipment and intangible assets, including goodwill. In the past year the company has experienced a significant decline in a number of its lines of business. Re

> An executive of a manufacturing company informs you that no formal procedures have been followed to control the retirement of machinery and equipment. A physical inventory of plant assets has just been completed. It revealed that 25 percent of the assets

> Assume that a continuing audit client has recorded Accounts Receivable and Equipment both in the amount of $1,000,000. In a typical audit, which account would take more time to audit?

> You are part of the audit team that is auditing Happy Chicken, Inc., a company that franchises Happy Chicken family restaurants. During the current year, management of Happy Chicken purchased for $2 million one of its franchised locations, a store that w

> Girard Corporation has just completed the acquisition of Williams, Inc., at a purchase price significantly higher than the fair values of the identifiable assets. Describe the audit issues caused by the acquisition and how the auditors would likely resol

> List and state the purpose of all audit procedures that might reasonably be applied by the auditors to determine that all property and equipment retirements have been recorded in the accounting records.

> Grandview Manufacturing Company employs standard costs in its cost accounting system. List the audit procedures that you would apply to ascertain that Grandview’s standard costs and related variance amounts are acceptable and have not distorted the finan

> Use the following to provide the type of audit report the auditors generally should issue in the situations presented below: 1. Unmodified—standard. 2. Unmodified—with an emphasis-of-matter paragraph. 3. Qualified. 4. Adverse. 5. Disclaimer Situation: a

> Assume that you are auditing Roberts Wholesale Supply Co. and that you have decided to use data analytics to test the inventory. Specifically, you would like to identify (1) excess and overvalued items in inventory (e.g., possibly obsolete, quantities we

> You are engaged in the audit of Reed Company, a new client, at the end of its first fiscal year, June 30, 20X1. During your work on inventories, you discover that all of the merchandise remaining in stock on June 30, 20X1, had been acquired July 1, 20X0,

> One of the problems faced by the auditors in their verification of inventory is the risk that slow-moving and obsolete items may be included in the goods on hand at the balance sheet date. In the event that such items are identified in the physical inven

> The City of Westmore is confused about the type of audit that it should obtain: an audit in accordance with generally accepted auditing standards, an audit in accordance with Generally Accepted Government Auditing Standards, or an audit in accordance wit

> North County School District expended $1,450,000 in federal financial assistance this year. Required: a. Is North County School District required to have an audit in accordance with the Single Audit Act? Explain. b. What are the requirements of an audit

> Wixon & Co., CPAs, is performing an audit of the City of Brummet for the year ended June 30, 200X, in accordance with Generally Accepted Government Auditing Standards. During the course of the audit, Gerald Yarnell, a senior auditor, discovers violations

> Matt Gunlock, CPA, is performing an audit of the City of Ryan in accordance with generally accepted auditing standards. Required: a. Must Matt be concerned with the city’s compliance with laws and regulations? Explain. b. How should Matt decide on the n

> CPAs may become involved in examinations of broker-dealers. a. Describe the information a broker-dealer who maintains custody of customer funds or securities is required to file in an annual compliance report. b. Which of the required information in part

> You are conducting the first audit of the marketing activities of your organization. Your preliminary survey has disclosed indications of deficient conditions of a serious nature. You expect your audit work to document the need for substantial corrective

> Throughout this book, emphasis has been placed on the concept of independence as the most significant single element underlying the development of the public accounting profession. The term “independent auditor” is sometimes used to distinguish the publi

> For each of the following brief scenarios, assume that you are reporting on a client’s financial statements. Reply as to the type(s) of opinion possible for the scenario. In addition: ∙ Unless stated otherwise, assume

> Steve Ankenbrandt, president of Beeb Corp., has been discussing the company’s internal operations with the presidents of several other multidivision companies. Ankenbrandt discovered that most of them have an internal audit staff. The activities of the s

> In order to function effectively, the internal auditor must often educate auditees and other parties bout the nature and purpose of internal auditing. Required: a. Define internal auditing. b. Briefly describe three possible benefits of an internal audi

> The third general attestation standard indicates that the subject matter of the engagement must be capable of reasonably consistent evaluation against criteria that are suitable and available to the user. Required: a. Explain why criteria are needed for

> The accounting profession has developed Trust Services to help entities differentiate themselves by demonstrating that they are attuned to the risks posed by their environment and that they are equipped with controls that address those risks. Present the

> The management of Williams Co. is considering issuing corporate debentures. To enhance the marketability of the bond issue, management has decided to include a financial forecast in the prospectus. Management has requested that your CPA firm examine the

> Match the following terms with the appropriate definition (or partial definition). Each definition may be used once or not at all. Term Definition (or Partial Definition) a. Compllance auditing b. Complance Supplement c. Government Auditing 1. A do

> In performing an audit in accordance with both generally accepted auditing standards and Generally Accepted Government Auditing Standards, the auditors are required to communicate information about weaknesses in the organization’s internal control. Howev

> In performing an audit in accordance with Generally Accepted Government Auditing Standards, the auditors are required to issue an additional combined report on compliance with laws and regulations and on internal control. Required: a. Describe the natur

> Devry Corporation has established an independent foundation for the purposes of community improvement. The foundation employs an executive director and eight staff people. The internal auditors of the company were requested to do an audit of the foundati

> You are the chief audit executive for the internal auditing function of a large municipal hospital. You receive monthly financial reports prepared by the accounting department, and your review of them has shown that total accounts receivable from patient

> Assume that you are a partner with the firm of Slater & Lowe LLP. You have been asked by Grayson, Inc., an industrial supply company, to provide assurance about the change in existing customer satisfaction over the last three years. Grayson’s management

> SysTrust and WebTrust are Trust Services developed by the AICPA and the CICA. Required: a. Present and describe the Trust Services principles. b. Present and describe the “criteria” related to Trust Services. c. What is the relationship between the prin

> Loman, CPA, who has audited the financial statements of the Broadwall Corporation, a publicly held company, for the year ended December 31, 20X6, was asked to perform a review of the financial statements of Broadwall Corporation for the period ending Mar

> Jiffy Clerical Services is a company that furnishes temporary office help to its customers. The company maintains its accounting records on a basis of cash receipts and cash disbursements. You have audited the company for the year ended December 31, 20X4

> Your working papers for an integrated audit being performed under PCAOB AS 2201 include the narrative description below of the cash receipts and billing portions of internal control of Slingsdale Building Supplies, Inc. Slingsdale is a single-store retai

> Assume that during the audit of the public Chandler Corporation the following critical audit matter was identified and summarized for purposes of inclusion in the audit report. Critique presentation and details of the matter. Critical Audit Matter

> Roscoe & Jones, Ltd., a CPA firm in Silver Bell, Arizona, has completed the audit of the financial statements of Excelsior Corporation as of, and for, the year ended December 31, 20X1. Findings related to the financial statements and the audit include ∙

> Sturdy Corporation (a nonpublic company) owns and operates a large office building in a desirable section of New York City’s financial center. For many years, management of Sturdy Corporation has modified the presentation of its financial statement by 1.

> The auditors’ report that follows was drafted by a staff accountant of Smith & Co., CPAs, at the completion of the audit of the financial statements of Lenses Co. (a public company) for the year ended December 31, 20X7. Required:

> Robertson Company had accounts receivable of $200,000 at December 31, 20X0, and had provided an allowance for uncollectible accounts of $6,000. After performing all normal auditing procedures relating to the receivables and to the valuation allowance, th

> During your observation of the November 30, 20X0, physical inventory of Jay Company, you note the following unusual items: a. Electric motors in finished goods storeroom not tagged. Upon inquiry, you are informed that the motors are on consignment to Jay

> Rowe Manufacturing Company has about 50 production employees and uses the following payroll procedures. The factory supervisor interviews applicants and on the basis of the interview either hires or rejects the applicants. After being employed, the appli

> In connection with an audit of the financial statements of Olympia Company, the auditors are reviewing procedures for accumulating direct labor-hours. They learn that all production is by job order and that all employees are paid hourly wages, with time

> The following are typical questions that might appear on an internal control questionnaire for payroll activities: 1. Is there adequate separation of duties between employees who maintain human resources records and employees who approve payroll disburse

> Your client is a company that owns a shopping center with 30 store tenants. All leases with the store tenants provide for a fixed rent plus a percentage of sales, net of sales taxes, in excess of a fixed dollar amount computed on an annual basis. Each le

> Rita King, your staff assistant on the April 30, 20X2, audit of Maxwell Company, was transferred to another assignment before she could prepare a proposed adjusting journal entry for Maxwell’s Miscellaneous Revenue account, which she ha

> You are engaged in the audit of Phoenix Corp., a new client, at the close of its first fiscal year, April 30, 20X1. The accounts had been closed before the time you began your year-end fieldwork. You review the following stockholders’ e

> You have received confirmations from the transfer agent and the registrar of Lowe Company as to the number of authorized and outstanding shares as of December 31, 20X1, Lowe’s year-end. a. Which financial statement assertions do these confirmations most

> Robert Hopkins was the senior office employee at the Griffin Equipment Company. He enjoyed the complete confidence of the owner, William Barton, who devoted most of his attention to sales, engineering, and production problems. All financial and accountin

> Your client, Software and Stuff (Software), has developed a new electronic game. One part of the game uses software developed by another company, Component of Yuma (Component). Software signed an agreement with Component that provides that Software will

> Marshall and Wyatt, CPAs, has been the independent auditor of Interstate Land Development Corporation for several years. During these years, Interstate prepared and filed its own annual income tax returns. During 20X4, Interstate requested Marshall and W

> The observation of a client’s physical inventory is a mandatory auditing procedure when possible for the auditors to carry out and when inventories are material. Required: a. Why is the observation of physical inventory a mandatory auditing procedure? E

> The audit staff of Adams, Barnes & Co. (ABC), CPAs, reported the following audit findings in their 20X5 audit of Keystone Computers & Networks (KCN), Inc.: 1. Unrecorded liabilities in the amount of $6,440 for purchases of inventory. These inventory item

> As part of your first audit of the financial statements of Marina del Rey, Inc., you have decided to confirm some of the accounts payable. You are now in the process of selecting the individual companies to whom you will send accounts payable confirmatio

> The following are typical questions that might appear on an internal control questionnaire for accounts payable. 1. Are monthly statements from vendors reconciled with the accounts payable listing? 2. Are vendors’ invoices matched with receiving reports

> You are the senior accountant in the audit of Granger Grain Corporation, whose business primarily involves the purchase, storage, and sale of grain products. The corporation owns several elevators located along navigable water routes and transports its g

> Western Trading Company is a sole proprietorship engaged in the grain brokerage business. On December 31, 20X0, the entire grain inventory of the company was stored in outside bonded warehouses. The company’s procedure of pricing inventories in these war

> You have been with Zaird & Associates for approximately three months and are completing your work on the BizCaz audit. BizCaz produces pullover knit shirts to address the business casual market for both men and women. Although your experience has been li

> Hovington, CPA, knows that while audit objectives relating to inventories may be stated in terms of the assertions as presented in this chapter, they also may be subdivided and stated more specifically. He has chosen to do so and has prepared the second

> Smith is the partner in charge of the audit of Blue Distributing Corporation, a wholesaler that owns one warehouse containing 80 percent of its inventory. Smith is reviewing the working papers that were prepared to support the firm’s opinion on Blue’s fi

> For each of the following independent cases, state the highest level of deficiency that you believe the circumstances represent: a control deficiency, a significant deficiency, or a material weakness. Explain your decision in each case. Case 1: The comp

> Your firm audits Metropolitan Power Supply (MPS). The issue under consideration is the treatment in the company’s financial statements of $700 million in capitalized construction costs relating to Eagle Mountain, a partially completed nuclear power plant

> Many companies employ outside service companies that specialize in counting, pricing, extending, and footing inventories. These service companies usually furnish a certificate attesting to the value of the physical inventory. Required: Assuming that the

> For each of the following brief scenarios, assume that you are reporting on a client’s current-year financial statements. Reply as to the type or types of opinion possible in the circumstance. S Unmodified—standard U Unmodified with emphasis-of-matter or

> You are a young CPA just starting your own practice in Hollywood, California, after five years’ experience with a “Big 4” firm. You have several connections in the entertainment industry and hope to develop a practice rendering income tax, auditing, and

> The auditors’ working paper that relates control strengths and weaknesses to the assertions about purchases and accounts payable is presented in Appendix 14A. This working paper also presents the auditors’ planned assessed level of control risk for each

> As indicated on the control risk assessment working paper in Appendix 14A, the auditors identified two weaknesses in internal control over the acquisition cycle of KCN. Describe the implications of each of the two weaknesses in terms of the type of error

> A summary of the controls for the acquisition cycle of Keystone Computers & Networks, Inc., appears in Appendix 14A. Required: a. For the following three controls over the acquisition cycle, indicate one type of error or fraud that the control serve

> Chem-Lite, Inc., maintains its accounts on the basis of a fiscal year ending March 31. At March 31, 20X1, the Equipment account in the general ledger appeared as shown below. The company uses straight-line depreciation, a 10-year life, and 10 percent sal

> Robert Myers, CPA, has been engaged to audit the City of Mystic in accordance with the Single Audit Act. Robert is aware that the Single Audit Act requires additional tests of major federal financial assistance programs, and he is trying to identify thos

> You are reviewing the property, plant, and equipment working papers of Mandville Corporation, a company that publishes travel guides. The lead schedule for the account is included in the chapter as Figure 13.1. The following are among the findings relati

> For each of the following brief scenarios, assume that you are the CPA reporting on the financial statements of a nonpublic company. Using the form included with this problem, describe the reporting circumstance involved, the type or types of opinion pos

> Assume that you are a CPA interested in expanding your services to provide System and Organization Controls Control (SOC) reports. Access the AICPA store website (aicpastore. com) and find guidance that will help you achieve your goal. Skim through the a

> Webstar, a nonpublic company, is owned by Ben Williams and three of his friends. Previously, the company’s financing has been internally generated, with limited equity contributions by the owners. The company has not been audited in the past, and William

> You have just been assigned as a member of the audit team of Bozarkana Company (a new client) and are considering accounts payable. Bozarkana Company uses a computerized voucher system for payables. As a starting point, you asked Bill Bozarkana, the cont

> Nancy Howe, your staff assistant on the April 30, 20X2, audit of Wilcox Company, was transferred to another audit engagement before she could complete the audit of unrecorded accounts payable. Her working paper, which you have reviewed and are satisfied

> Taylor, CPA, is engaged in the audit of Rex Wholesaling for the year ended December 31. Taylor obtained an understanding of internal control relating to the purchasing, receiving, trade accounts payable, and cash disbursement cycles and has decided not t

> You are engaged in the audit of the financial statements of Holman Corporation for the year ended December 31, 20X6. The accompanying analyses of the Property, Plant, and Equipment and related accumulated depreciation accounts have been prepared by the c

> Assume that you are auditing the financial statements of Agee Corporation. During the course of the audit, you discover the following circumstances. 1. Management of Agee has decided to discontinue the production of consumer electronics, which represents

> You are an audit manager of the rapidly growing CPA firm of Raye and Coye. You have been placed in charge of three new audit clients, which have the following inventory features: 1. Canyon Cattle Co., which maintains 15,000 head of cattle on a 1,000-squa

> You are involved in your CPA firm’s first audit of Zorostria, a retailer of artwork, primarily paintings and photographs purchased from artists in Southeast Asia (particularly Vietnam, Cambodia, and Laos). Zorostria has stores in seven cities throughout