Question: For each term in the first column

For each term in the first column below, identify its definition (or partial definition). Each definition may be used once or not at all.

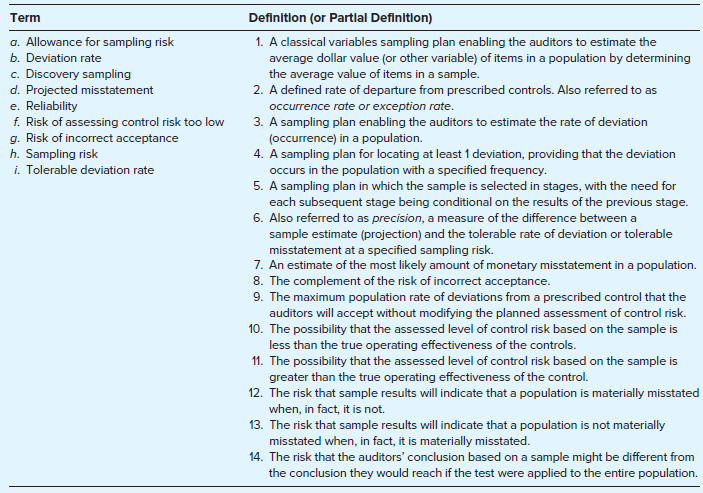

Transcribed Image Text:

Term Definition (or Partlal Definition) a. Allowance for sampling risk 1. A classical variables sampling plan enabling the auditors to estimate the b. Deviation rate c. Discovery sampling d. Projected misstatement average dollar value (or other variable) of items in a population by determining the average value of items in a sample. 2. A defined rate of departure from prescribed controls. Also referred to as e. Reliability f. Risk of assessing control risk too low g. Risk of incorrect acceptance h. Sampling risk i. Tolerable deviation rate occurrence rate or exception rate. 3. A sampling plan enabling the auditors to estimate the rate of deviation (occurrence) in a population. 4. A sampling plan for locating at least 1 deviation, providing that the deviation occurs in the population with a specified frequency. 5. A sampling plan in which the sample is selected in stages, with the need for each subsequent stage being conditional on the results of the previous stage. 6. Also referred to as precision, a measure of the difference between a sample estimate (projection) and the tolerable rate of deviation or tolerable misstatement at a specified sampling risk. 7. An estimate of the most likely amount of monetary misstatement in a population. 8. The complement of the risk of incorrect acceptance. 9. The maximum population rate of deviations from a prescribed control that the auditors will accept without modifying the planned assessment of control risk. 10. The possibility that the assessed level of control risk based on the sample is less than the true operating effectiveness of the controls. 11. The possibility that the assessed level of control risk based on the sample is greater than the true operating effectiveness of the control. 12. The risk that sample results will indicate that a population is materially misstated when, in fact, it is not. 13. The risk that sample results will indicate that a population is not materially misstated when, in fact, it is materially misstated. 14. The risk that the auditors' conclusion based on a sample might be different from the conclusion they would reach if the test were applied to the entire population.

> Today you had lunch with your friend Sarah Teasdale. Sarah has worked with Zaird & Associates, CPAs, for about two years. You’ve been with Zaird for only nine months. You discussed with her your difficulties in getting jobs done in the budgeted number of

> Give two reasons audit work on cash is likely to be more extensive than might appear to be justified by the relative amount of the balance sheet figure for cash.

> In selecting items for examination, an auditor considered three alternatives: (a) random number table selection, (b) systematic selection, and (c) random number generator selection. Which, if any, of these methods would lead to a random sample if properl

> On October 21, Rand & Brink, a CPA firm, was retained by Suncraft Appliance Corporation to perform an audit for the year ended December 31. A month later, James Minor, president of the corporation, invited the CPA firm’s partners, George Rand and Alice B

> You have worked with Zaird & Associates, CPAs, for a little more than a year and are beginning your second audit of Universal Air (UA). This year you even have an assistant reporting to you—Jane McClain. Jane has come to you with a concern. She noticed t

> You are an assistant auditor with Zaird & Associates, CPAs. Universal Air (UA), your fifth audit client in your eight months with Zaird, is a national airline based in your hometown. UA has continued to grow while remaining healthy financially over the e

> Baker, CPA, was engaged to audit Mill Company’s financial statements for the year ended December 31, 200X. After obtaining an understanding of Mill’s internal control, Baker decided to obtain audit evidence about the effectiveness of both the design and

> An improper cutoff of transactions around year-end occurs when journal entries are recorded in the wrong year. In this case, you are to determine the effects of various cutoff misstatements relating to recording cash receipts received on accounts receiva

> Listed below are eight interbank cash transfers for Steven Smith Co., indicated by the letters a through h, for late December 20X1 and early January 20X2. For each of the transfers a through h, (1) indicate whether cash is understated, overstated, or

> Ming, CPA, is engaged to audit the financial statements of Wellington Sales, Inc., for the year ended December 31, 20X0. Ming obtained and documented an understanding of the client’s business and environment, including internal control

> The July 31, 20X0, general ledger trial balance of Aerospace Contractors, Inc., reflects the following accounts associated with receivables. Balances of the accounts are after all adjusting journal entries proposed by the auditors and accepted by the cli

> You are conducting an annual audit of Granite Corporation, which has total assets of approximately $1 million and operates a wholesale merchandising business. The corporation is in good financial condition and maintains an adequate accounting system. Gra

> During your examination of the financial statements of Martin Mfg. Co., a new client, for the year ended March 31, 20X0, you note the following entry in the general journal dated March 31, 20X0: Your review of the contract for sale between Martin and A

> An audit client that has never before invested in securities recently acquired more than a million dollars in cash from the sale of real estate no longer used in operations. The president intends to invest this money in marketable securities until such t

> The following are typical questions that might appear on an internal control questionnaire for accounts receivable: 1. Are sales invoices checked for proper pricing, terms, and clerical accuracy? 2. Are shipping documents prenumbered and all numbers acco

> Halston Toy Manufacturing Co. introduced a number of new products in the last quarter of the year. The company has a liberal return policy allowing retail customers to return products within 120 days of purchase. a. Describe the audit problem indicated b

> In your audit of Ginko Company, you have received a cash confirmation and a cutoff statement from the bank on Ginko’s one bank account. Prepare a list of substantive procedures for Ginko’s cash.

> During the audit of Sunset Building Supply, you are given the following year-end bank reconciliation prepared by the client: According to the client’s accounting records, checks totaling $31,482 were issued between January 1 and Janu

> You are the senior auditor-in-charge of the July 31, 20X0, audit of Reliable Auto Parts, Inc. Your newly hired staff assistant reports to you that she is unable to complete the four-column roof of cash for the month of April 20X0, which you instructed he

> Following are typical questions that might appear on an internal control questionnaire for investments in marketable securities. 1. Is custody of investment securities maintained by an employee who does not maintain the detailed records of the securities

> The auditors wish to test the valuation of accounts receivable in the audit of Kaplan Corporation. The client has $1,000,000 of total recorded receivables, composed of 2,000 accounts. The auditors have decided to use structured nonstatistical sampling an

> The auditors of Landi Corporation wish to use a structured approach to nonstatistical sampling to evaluate the reasonableness of the accounts receivable. Landi has 15,000 receivable accounts with a total book value of $2,500,000. The auditors have assess

> To test the pricing and mathematical accuracy of sales invoices, the auditors selected a sample of 200 sales invoices from a total of 41,600 invoices that were issued during the year under audit. The 200 invoices represented total recorded sales of $22,8

> In the audit of Potomac Mills, the auditors wish to test the costs assigned to manufactured goods. During the year, the company has produced 2,000 production lots with a total recorded cost of $5.9 million. The auditors select a sample of 200 production

> What is the meaning of the term window dressing when used in connection with year end financial statements? How might the term be related to the making of loans by a corporation to one or more of its executives?

> You are the auditor of Jexel, an auto air-conditioner service and repair company, and you have decided to use the mean-per-unit method to test the existence and gross valuation of recorded accounts receivable. The client’s records include 10,000 accounts

> Scott Duffney, CPA, has randomly selected and audited a sample of 100 of Will-Mart’s accounts receivable. Will-Mart has 3,000 accounts receivable accounts with a total book value of $3,000,000. Duffney has determined that the account’s tolerable misstate

> As part of your audit of the Abba Company accounts payable function, your audit plan includes a test of controls addressing the company policy requiring that all vouchers be properly approved. You estimate the population deviation rate to be 3 percent.

> The use of statistical sampling techniques in an audit of financial statements does not eliminate judgmental decisions. Required: a. Identify and explain four areas in which judgment may be exercised by CPAs in planning a statistical test of controls. b

> This simulation, also available on online, presents the Memo re Sales Invoice Procedures/ Results relating to the Keystone Computers & Networks, Inc. (Keystone), audit. Background financial and other information on Keystone is included in Appendix 6C

> The auditors have determined that each of the following objectives will be a part of the audit of SSC Corporation. While several procedures will ordinarily address an audit objective, select the procedure most directly related to the audit objective. Eac

> An auditor may use confirmations of accounts receivable. Reply as to whether the following statements are correct or incorrect with respect to the confirmation process when applied to accounts receivable. a. The confirmation requests should be mailed to

> An assistant on the Carter Company audit has been working in the revenue cycle and has compiled a list of possible errors and fraud that may result in the misstatement of Carter Company’s financial statements and a corresponding list of

> An auditor’s working papers include the following narrative description of the cash receipts and billing portions of Southwest Medical Center’s internal control. Evaluate each condition following the narrative as being either (1) a strength, (2) a defici

> You are involved with the audit of Jelco Company for year 1 and have been asked to consider the confirmation reply results indicated below. For each confirmation reply, select the proper action to be taken from the following possible actions: (1) Excepti

> Explain two procedures by which auditors may verify the client’s cutoff of cash receipts.

> For each of the procedures described in the table below, identify the audit procedure performed and classification of the audit procedure using the following: Audit Procedures: Classification of Audit Procedure: (1) Analytical procedure (9) Substa

> During your audit of Carla Pang Inc., you prepared the following bank transfer schedule. Fill out the table below indicating the most likely situation as it relates to cash at year-end. Indicate the situation using one of the following: 1. Year-end tot

> Auditors perform a number of procedures relating to cash—some unique, some not unique. For each substantive procedure below, identify its primary objective or indicate that the procedure serves no purpose. Substantive Procedures: a. Prepare a bank trans

> Items a through f represent the items that an auditor ordinarily would find on a client-prepared bank reconciliation. The accompanying List of Auditing Procedures represents substantive auditing procedures. For each item, select one or more procedures, a

> Items a through l represent possible errors and fraud that you suspect may be present at Rex Company. The accompanying List of Auditing Procedures represents procedures that the auditor would consider performing to gather evidence concerning possible err

> You are working on your firm’s fifth audit of SSC. The previous audits have all resulted in standard unqualified audit reports. Read the following write-up from your audit files concerning SSC and its industry, and then reply to the questions that follow

> Select the best answer for each of the following situations and give reasons for your choice. a. Which of the following controls would most likely reduce the risk of diversion of customer receipts by a client’s employees? (1) A bank lockbox system. (2) P

> This simulation, also available online, presents the Keystone Computers & Networks, Inc. (Keystone) Cash Work Memo for the general account and petty cash. Background financial and other information on Keystone is included in Appendix 6C of Chapter 6.

> The auditor of Cubs obtained the following client-prepared bank reconciliation: The auditor for Cubs Co. has obtained the client-prepared bank reconciliation. The following information is available: ∙∙ Evan Monroe wa

> Use the replies presented in the preceding problem for this problem. a. Use the ratio method to calculate: (1) Projected misstatement. (2) Estimated total audited value. b. Use the difference estimation method to calculate: (1) Projected misstatement. (2

> Explain the objectives of each of the following audit procedures for cash: a. Obtain a cutoff bank statement subsequent to the balance sheet date. b. Compare paid checks returned with the bank statement to the list of outstanding checks in the previous r

> Smith, Inc. Rachel Robertson wishes to use mean-per-unit sampling to evaluate the reasonableness of the book value of the accounts receivable of Smith, Inc. Smith has 10,000 receivable accounts with a total book value of $1,500,000. Robertson estimates t

> You have been asked to test the effectiveness of Ingo Corporation’s control of manually approving all purchases over $25,000. During the year, Ingo Corporation has made 1,000,000 purchases, of which 3,000 were over $25,000. Jian Zhang,

> The professional development department of a large CPA firm has prepared the following illustration to familiarize the audit staff with the relationships of sample size to population size and variability and the auditors’ specifications

> The 10 following statements apply to unrestricted random sampling without replacement. Indicate whether each statement is true or false. Briefly discuss each false statement. a. When sampling from the population of accounts receivable for certain objecti

> Select the best answer for each of the following questions. Explain the reasons for your selection. a. Which of the following is an element of sampling risk? (1) Choosing an audit procedure that is inconsistent with the audit objective. (2) Concluding t

> Select the best answer for each of the following and explain fully the reason for your selection. a. Which of the following is least likely to be considered an inherent risk relating to receivables and revenues? (1) Restrictions placed on sales by laws a

> Hale Nelson, CPA, is engaged to audit the financial statements of Hollis Manufacturing, Inc. Hollis engages in very complex sales agreements that create issues with respect to revenue recognition. As a result, Nelson has identified revenue recognition as

> An assistant auditor was instructed to “test the aging of accounts receivable as shown on the schedule prepared by the client.” In making this test, the assistant traced all past-due accounts shown on the trial balance to the details in the accounts rece

> Walter Conn, CPA, is engaged to audit the financial statements of Bingo Wholesaling for the year ended December 31, 20X0. Conn obtained and documented an understanding of the client and its environment, including internal control over the business proces

> What action should be taken by the auditors when the count of cash on hand discloses a shortage?

> During the audit of Solar Technologies, Inc., the auditors sent confirmation requests to customers whose accounts had been written off as uncollectible during the year under audit. An executive of Solar protested, saying, “You people should be verifying

> Lakeside Company has retained you to conduct an audit so that it will be able to support its application for a bank loan with audited financial statements. The president of Lakeside states that you will have unlimited access to all records of the company

> During preliminary conversations with a new staff assistant, you instruct her to send out confirmation requests for both accounts receivable and notes receivable. She asks whether the confirmation requests should go to the makers of the notes or to the h

> In their work on accounts receivable and elsewhere in an audit, the independent auditors often make use of confirmation requests. a. What is an audit confirmation request? b. What characteristics should an audit confirmation response possess if a CPA fir

> Hayden Corp. uses an enterprise resource planning (ERP) system. In their audit of receivables and revenues, the auditors have identified the following data elements in the corporation’s database that may be used for data analytics applications: Customer

> Listed below are audit situations that may affect the audit of receivables and revenue. a. The audit of a machinery manufacturing company that engages in bill and hold transactions. b. The audit of a software company that engages in agreements with multi

> Based on an assessment of audit risk, the auditors are concerned with the following two risks: 1. The risk that that the client might be making duplicate payments to vendors. 2. The risk that the client’s accounting clerk might be making unauthorized pay

> During your audit of Miles Company, you prepared the following bank transfer schedule: Required: a. Describe the purpose of a bank transfer schedule. b. Identify those transfers that should be investigated and explain the reason. MILES COMPANY Ban

> During the current year, the management of Hanover, Inc., entered into a futures contract to hedge the price of silver that will be needed for next year’s production. The contract, which is held by Hanover’s commodity broker, is marketable and exchanged

> Explain how each of the following items would appear in a four-column proof of cash for the month of November. Assume the format of the proof of cash begins with bank balances and ends with the unadjusted balances per the accounting records. a. Outstandi

> How can the auditors corroborate compensating balance arrangements?

> In the audit of Wheat, Inc., for the year ended December 31, you discover that the client had been drawing checks as creditors’ invoices became due but had not been mailing the checks immediately. Because of a working capital shortage, some checks have b

> In the audit of a client with a fiscal year ending December 31, the CPAs obtain a January 10 bank statement directly from the bank. Explain how this cutoff bank statement will be used a. In the review of the December 31 bank reconciliation. b. To obtain

> “When auditors are verifying a client’s bank reconciliation, they are particularly concerned with the possibility that the list of outstanding checks may include a nonexistent or fictitious check, and they also are concerned with the possibility of omiss

> An assistant auditor received the following instructions from her supervisor: “Here is a cutoff bank statement covering the first seven business days of January. Compare the paid checks returned with the statement and dated December 31 or earlier with th

> You are the auditor in charge of the audit of Steffens Corporation. In the audit of investments, you have just been given the following list of securities held by Steffens Corporation at December 31, 20X3. Required: a. Identify the potential audit pro

> During an audit of Rottel Company, an auditor needs to estimate the total value of the 5,000 invoices processed during June. She estimates the standard deviation of the population to be $30. Determine the size of the sample the auditor would select when

> Bill Jones wishes to use nonstatistical sampling to select a sample of his client’s 3,000 accounts receivable, which total $330,000. He believes that $30,000 represents a reasonable tolerable misstatement. He also has assessed both the combination of inh

> Ratio estimation and difference estimation are two widely used variables sampling plans. Required: a. Under what conditions are ratio estimation or difference estimation appropriate sampling plans for estimating the total dollar value of a population? b

> Cathy Williams is auditing the financial statements of Westerman Industries. In the performance of mean-per-unit estimation of credit sales, Williams took a sample of 200 of the 10,000 items in the population (book value $3,000,000). The sample’s average

> An auditor used a nonstatistical sampling plan to audit the inventory of an auto supply company. The auditor tested the recorded cost of a sample of inventory items by reference to vendors’ invoices. In performing the test, the auditor verified all the i

> What information do CPAs request from a financial institution on the standard confirmation form?

> An auditor has reason to suspect that fraud has occurred through forgery of the treasurer’s signature on company checks. The population under consideration consists of 3,000 checks. Can discovery sampling rule out the possibility that any forged checks e

> In performing a test of controls for sales order approvals, the CPAs stipulate a tolerable deviation rate of 8 percent with a risk of assessing control risk too low of 5 percent. They anticipate a deviation rate of 2 percent. Required: a. What type of s

> CPAs may decide to apply nonstatistical or statistical techniques to audit testing. a. List and explain the advantages of applying statistical sampling techniques to audit testing. b. List and discuss the decisions involving professional judgment that mu

> During the first few months of the year, John Smith, the cashier in a small company, was engaged in lapping operations. However, he was able to restore the amount of cash “borrowed” by March 31, and he refrained from any fraudulent acts after that date.

> Henry Mills is responsible for preparing checks, recording cash disbursements, and preparing bank reconciliations for Signet Corporation. While reconciling the October bank statement, Mills noticed that several checks totaling $937 had been outstanding f

> Fluid Controls, Inc., a manufacturing company, has retained you to perform an audit for the year ended December 31. Prior to the year-end, you begin to obtain an understanding of the new client’s controls over business processes related to the cash accou

> You have been assigned to the audit of Processing Solutions, Inc., a privately held corporation that develops and sells computer systems. The systems are sold under one- to five-year contracts that provide for a fixed price for licensing, delivery, and s

> Describe how the organizational status of the internal audit department affects its independence.

> Evaluate this statement: “Internal auditors cannot be independent of the activities that they audit.”

> Identify the 11 categories of the IIA’s International Standards for the Professional Practice of Internal Auditing.

> During your reconciliation of bank accounts in an audit, you find that a number of checks for small amounts have been outstanding for more than a year. Does this situation call for any action by the auditor? Explain.

> Compare the objectives of internal auditors with those of external auditors.

> “The principal distinction between public accounting and internal auditing is that the latter activity is carried on by an organization’s own salaried employees rather than by independent professional auditors.” Criticize this quotation.

> Identify the knowledge and skills that are necessary to the performance of modern internal auditing.

> Identify the 12 requirements that may be applicable to federal financial assistance programs.

> Distinguish between a subrecipient and a primary recipient. Provide an example of each.

> Describe what is meant by a questioned cost.

> Explain how major federal assistance programs are identified.

> Nearly every large corporation now maintains an internal auditing department, but 50 years ago relatively few companies carried on a formal program of internal auditing. What have been the principal factors responsible for this rapid expansion?

> When is an organization required to have an audit in accordance with the Single Audit Act?

> What is the purpose of the Single Audit Act?