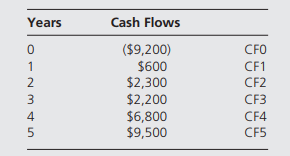

Question: Smith invests in a limited partnership that

Smith invests in a limited partnership that requires an outlay of $9,200 today. At the end of years 1 through 5, he will receive the after-tax cash flows shown below. The partnership will be liquidated at the end of the fifth year. Smith is in the 28 percent tax bracket.

A. The after-tax IRR of this investment is

1. 17.41 percent.

2. 19.20 percent.

3. 24.18 percent.

4. 28.00 percent.

5. 33.58 percent.

B. Which of the following is/are correct?

1. The IRR is the discount rate that equates the present value of an investment’s expected costs with the present value of the expected cash inflows.

2. The IRR is 24.18 percent, and the present value of the investment’s expected cash flow is $9,200.

3. The IRR is 24.18 percent. For Smith to actually realize this rate of return, the investment’s cash flows will have to be reinvested at the IRR.

4. If the cost of capital for this investment is 9 percent, the investment should be rejected because its net present value will be negative.

a. (2) and (4) only

b. (2) and (3) only

c. (1) only

d. (1), (2) and (3) only

e. (1) and (4) only

Transcribed Image Text:

Years Cash Flows ($9,200) $600 CFO 1 CF1 2 $2,300 $2,200 $6,800 $9,500 CF2 CF3 4 CF4 CF5

> Modern “asset allocation” is based upon the model developed by Harry Markowitz. Which of the following statements is/are correctly identified with this model? 1. The risk, return, and covariance of assets are important input variables in creating portfol

> Which of the following are non diversifiable risks? 1. Business risk. 2. Management risk. 3. Company or industry risk. 4. Market risk. 5. Interest rate risk. 6. Purchasing power risk. a. 1 and 3 only b. 1 and 4 only. c. 2 and 4 only. d. 4 only. e. 1, 2,

> If the market risk premium were to increase, the value of common stock (everything else being equal) would a. Not change because this does not affect stock values. b. Increase in order to compensate the investor for increased risk. c. Increase due to hig

> If the client needs to accumulate wealth but is risk-averse, which of the following is the most crucial action the planner must take to have the client achieve the goal of wealth accumulation? Advise investing the client’s current assets a. In the produc

> Stock prices adjust rapidly to the release of all new public information.” This statement is an expression of which one of the following ideas? a. Random walk hypothesis. b. Arbitrage pricing theory c. Semi strong form of the EMH d. Technical analysis

> Marcia had a choice of two washing machines of equal performance. One cost $400 and had a present value (PV) of $230 in savings over having clothes done through an outside service. The second cost $600 and had a PV of $450. Which one should she select?

> A CFP® professional meets with two new clients who would like advice about their mortgage. In the review, the CFP® professional finds that their essential expenses exceed their income. Mortgage rates have come down significantly and they intend to refina

> A young couple would like to purchase a new home using one of the following mortgages: Mortgage no. 1: 10.5 percent interest with 5 discount points to be paid at time of closing Mortgage no. 2: 11.5 percent interest with 2 discount points to be paid at t

> The Moores recently found out that they can reduce their mortgage interest rate from 12 percent to 8 percent. The value of homes in their neighborhood has been increasing at the rate of 7.5 percent annually. If the Moores were to refinance their house wi

> A cash-basis taxpayer includes income from a service business when a. The services are performed. b. The client is invoiced for the services. c. The client’s check is deposited in the bank. d. The client’s check is received.

> A client provides a current balance sheet to the financial planner during the initial data gathering phase of the financial planning process. This financial statement will enable the financial planner to gain an understanding of all of the following exce

> Why is integration so important in financial planning?

> Describe some similarities and differences between a financial planning practitioner and a physician.

> Contrast a segmented and a comprehensive financial plan.

> Describe the personal financial planning process and relate it to planning procedures.

> Explain the terms PV and FV.

> Helen, a sociologist, is considering buying a new power lawn mower. It would save her 30 minutes of work a week, which she would use to see another client. Her fee is $16 per hour and she works 50 weeks a year. The lawn mower would cost $1,400. What woul

> Why does personal financial planning involve other disciplines as shown in Figure 1.3? Give some practical examples of their use. Figure 1.3: FINANCE TOOLS OTHER DISCIPLINES AND TOOLS Micro and macroeconomics - Time value of money - Cash flow analy

> Why did it take until the 1970s for the field of financial planning to begin?

> Explain withdrawal risk.

> Why is it advisable to have a significant amount of a retirement portfolio invested in equity?

> How does investing for retirement differ from investing after retirement? Why?

> What are the similarities and differences between retirement needs and insurance?

> Why should a family have umbrella insurance?

> Identify and briefly explain the principal types of social insurance.

> Why is an own occupation definition for disability so valuable?

> Contrast an HMO and a PPO.

> Laurence was presented with a capital expenditure for a furnace that would cost $12,000 today and would generate the following savings. Year ………………..Amount 1 ……………………………$2,000 2 ……………………………$3,000 3 …………………………….$2,000 4 ……………………………$4,000 5 ……………………………$5,

> Define adverse selection and give an example of it.

> What is longevity risk and explain the two different scenarios that exist?

> Identify the three parts of an insurance policy?

> What is indexed universal life insurance and how is it different from the other whole life policies?

> How does portfolio management enter into the risk management process?

> Name three strengths and weaknesses of whole life and term insurance.

> Julian was considering whole life and term insurance for his 20-year need. Which one should he select?

> Why can term insurance be deducted from whole life to determine the return on the whole life policy?

> Describe the insurance needs approach.

> List the types of risks to human assets and briefly explain how to reduce them.

> Louis had the following cash flow items: Cash flow from operations ………………………$40,000 Interest payments ………………………………………6,000 Total interest and debt payments …………………9,000 If Louis is in the 30 percent tax bracket, how many times are fixed payments earned

> What are the significant factors in selecting an insurance company?

> How can insurance modify portfolio risk?

> What are the weaknesses of mutual funds?

> In what cause would you to suggest direct ownership over private partnership? Why?

> Compare and contrast the value in owning a home versus investing in real estate investment trusts (REITs).

> Why is a home a good inflation hedge? Should a home be included as an asset if its occupants aren’t sure they could sell it? Explain.

> Why is the home often a better investment than renting? Under what circumstances would renting be preferred?

> What are the significant characteristics of a mortgage?

> Contrast life cycle human-asset valuations for skilled and unskilled workers.

> What are the strengths and weaknesses of the net present value (NPV) and internal rate of return (IRR) methods?

> Why should capital expenditures be treated separately on a cash flow statement?

> Briefly explain total portfolio management (TPM).

> Discuss the advantages and disadvantages of leasing a car.

> What factors should you consider when you aren’t sure whether to buy or lease a car?

> Describe the three approaches to decision making for capital expenditures.

> Contrast the strengths and weaknesses of a fixed-rate mortgage with those of a variable-rate mortgage.

> List and explain the borrowing factors.

> Why is operating leverage as it pertains to risk important?

> Contrast the interests of young people and seniors.

> What is the difference between debt and fixed obligations?

> Investment A costs $10,000,000 and offers a single cash inflow of $13,000,000 after one year. Investment B costs $1,000,000 and will be worth $2,000,000 at the end of the year. The appropriate discount rate or required rate of return is 10 percent compou

> Richard e-mailed me that he and Monica differed about the impact of his extra spending over the past 15 years. He calculated it at about $3,000 a year. He said the total cost of $45,000 was well within his capability to make up. Monica said the cost was

> How would you interact and advise a client with goals you personally find outlandish but that the client values greatly. Creating a mock dialogue could be helpful.

> What would you consider to be the financial equivalent of Maslow’s hierarchy of needs? What are the basics? What comes last?

> What is the difference between feeling sympathy and empathy for the client? Is one more valuable than the other? Why?

> Which types of data should be gathered at an initial interview and which should be left for future meetings?

> What are two pieces of data that are needed in each of the six financial planning areas?

> In calculating the ratio times fixed payments earned, after-tax interest payments are added back in the denominator. Why?

> What is the difference between debt and fixed obligations?

> Jeremy is in financial difficulty. He owes $5,000 and cannot pay it back now. Should he declare bankruptcy? Why? What do you think he should do?

> What are some attractive interviewing techniques?

> What are some of the broad financial goals of people with whom you will come in contact?

> This case allows students to develop solutions themselves. It begins with an extensive background that will assist in the decisions that are asked for in subsequent chapters. BACKGROUND—FIRST INTERVIEW Brad and Barbara arranged to come in to see me. The

> How can financial planning goals be broken down into minimum, satisfactory, and higher-level components according to parts of the financial plan?

> Credit cards are a grossly inefficient way to borrow money. True or false? Explain and discuss their advantages.

> Why is preplanning for an interview important?

> How should resistance to a question or recommended course of action be handled?

> Alexis wants to buy a large home relative to her income and thinks that she may not qualify for a mortgage for 80 percent of the price. She expects interest rates to rise and anticipates staying in the home for many years. Explain the strengths and weakn

> Contrast the views of finance and accounting on recording operating results.

> Outline some expenses of a pro forma statement that cannot use inflation to project their growth and indicate what rate should be used.

> Is an increase in debt a plus or minus from a cash flow standpoint? Explain.

> Why segregate a balance sheet by type of asset and type of liability?

> Elaborate on the two approaches to making projections for a cash flow statement.

> In working out the capital needs analysis, it became apparent that there was need for an additional $17,000 of savings annually over what was previously calculated. The first reason had to do with a recent job development that resulted in a projected mod

> What are reasons that a person may have a poor net cash flow yet be considered to be in good financial health?

> In your opinion, which presents results more fairly, finance or accounting? Explain.

> What makes the household an enterprise?

> Define the term opportunity cost of time.

> What does life cycle theory say a household should have in savings at the end of its life? Is that practical? Explain your answer.

> List some of the advantages and disadvantages of various organizational structures for the individual.

> What is TPM and why is it valuable in the framework of household planning?

> When would it be beneficial for the household enterprise to outsource some activities, for example, cooking?

> Are any of the outlays in preferable to the others? Support your answer.

> What is the importance of the theory of financial planning?

> Richard came in with his cash flow statistics and very helpful notes on projections. His list included He said to assume that his salary will rise 6 percent a year, and his investment income is 11 percent a year (the investment loss came a year ago). H

> Outline the similarities and differences between a household and a business.

> Why is it important to differentiate among the various types of household expenditures?

> Describe household operations according to household finance.

> What is rate of return and why do we use inflation-adjusted return?

> Explain regular annuity versus annuity due and give examples.

> How does household finance tie into financial planning?