Question: Swisscom AG, the principal provider of

Swisscom AG, the principal provider of telecommunications in Switzerland, prepares consolidated financial statements in accordance with International Financial Reporting Standards (IFRS). Until 2007, Swisscom also reconciled its net income and stockholders’ equity to U.S. GAAP. Swisscom’s consolidated financial statements from a recent annual report are presented in their original format in Column 1 of the following worksheet. Note 27, Differences between International Financial Reporting Standards and U.S. Generally Accepted Accounting Principles, which includes Swisscom’s U.S. GAAP reconciliation, also is provided.

Required:

1. Use the information in Note 27 to restate Swisscom’s consolidated financial statements in accordance with U.S. GAAP. Begin by constructing debit/credit entries for each reconciliation item, and then post these entries to columns 2 and 3 in the worksheets provided.

2. Calculate each of the following ratios under both IFRS and U.S. GAAP and determine the percentage differences between them, using IFRS ratios as the base:

Net income/Net revenues

Operating income/Net revenues

Operating income/Total assets

Net income/Total shareholders’ equity

Operating income/Total shareholders’ equity

Current assets/Current liabilities

Total liabilities/Total shareholders’ equity

Which of these ratios is most (least) affected by the accounting standards used?

Current Year Ended

(CHF in millions) December 31

Net income (loss) according to IFRS…………………………………………………. (415)

U.S. GAAP adjustments

a) Capitalization of interest cost…………….………………………………………………….8

b) Restructuring charges……………………………………………………………………….205

c) Depreciation expense…………………………………………………………………………. (5)

d) Capitalization of software…………………………………………………………………….182

e) Restructuring charges by afï¬liates………………………………………………………..50

Net income according to U.S. GAAP………………………………………………………….25

Reconciliation of shareholders’ equity from IFRS to U.S. GAAP

The following is a reconciliation of the signiï¬cant adjustments necessary to reconcile shareholders’ equity in accordance with U.S. GAAP to the amounts determined under IFRS as at December 31 of the current year.

Current Year Ended

(CHF in millions) December 31

Shareholders’ equity according to IFRS………………….………………………1,230

U.S. GAAP adjustments

a) Capitalization of interest cost…………………………………………………………54

b) Restructuring charges………………………………………………………………….205

c) Depreciation expense……………………………………………………………………. (5)

d) Capitalization of software……………………………………………………………. 475

e) Restructuring charges by afï¬liates………………………………………………….50

Shareholders’ equity according to U.S. GAAP…………………………………2,009

Current Year

(CHF in millions)

Restructuring charges in accordance with IFRS:

Personnel restructuring charges……………………………………………………………1,326

Write-down of long-lived assets………………………………………………………………. 316

Miscellaneous restructuring charges…………………………………………………………..84

Total in accordance with IFRS………………………………………………………………...1,726

Adjustments to restructuring charges to accord with U.S. GAAP…………….…. (205)

Restructuring charges in accordance with U.S. GAAP………………………………. 1,521

Current Year Ended

Reconciliation of restructuring charges December 31

Restructuring charges according to U.S. GAAP

are comprised of the following:

Personnel restructuring charges…………………………………………………………..1,228

Write-down of long-lived assets…………………………………………………..………….209

Miscellaneous restructuring charges ………………………………………………………..84

Restructuring charges in accordance with U.S. GAAP……………………...........1,521

Note: Assume the counterpart to the personnel restructuring charge affects “other long-term liabilities.â€

c) Depreciation Expense

Due to the difference in carrying value of long-lived assets after write-downs described in (b), there is a difference in the amount of depreciation expense taken under IFRS and U.S. GAAP. An adjustment is made for the current year to record an additional CHF 5 million of depreciation under U.S. GAAP.

d) Capitalization of software

Swisscom has expensed software costs as incurred. For U.S. GAAP purposes external consultant costs incurred in the development of software for internal use have been capitalized. These costs are being amortized over a three year period. The capitalization of software costs accords with common practice in the U.S. telecommunications industry. Swisscom has capitalized, as disclosed in the reconciliation of net income (loss) and shareholders’ equity to U.S. GAAP, CHF 220 million and amortized CHF 37 million in the previous year and capitalized CHF 370 million and amortized CHF 188 million in the current year.

e) Restructuring charges of afï¬liates

During the current year, Swisscom’s share of personnel and other restructuring charges recorded by afï¬liates amounted to CHF 50 million. These restructuring charges do not meet all the recognition criteria contained in EITF 94-3 and therefore cannot be expensed in the current year, under U.S. GAAP.

Transcribed Image Text:

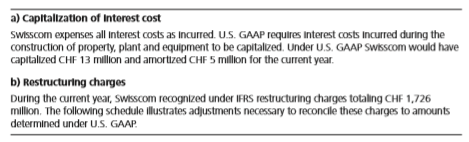

Worksheet for the Restatement of Swisscom's Financial Statements from IFRS to U.S. GAAP (2) (3) Reconciling Adjustments (1) IFRS (4) Debit Credit U.S. GAAP Consolidated Statement of Operations Net revenues 9,842 Capitalized cost and changes in inventories 277 Total 10,119 Goods and services purchased Personnel expenses Other operating expenses Depreciation and amortization 1,666 2,584 2,090 1,739 Restructuring charges. Total operating expenses Operating income . 1,726 9,805 314 Interest expense. (428) Financial income. 25 Income (loss) before income taxes and equity in net loss of affiliated companies Income tax expense (89) Income (loss) before equity in net loss of affiliated companies. (90) equity in net loss of affiliated 325) (415) соmpanies. Net income (loss). Consolidated Retained Earnings Statement Retained earnings, 1/1 (151) Net loss. (415) Profit distribution dedared (1,282) Conversion of loan payable to equity 3,200 Retained earnings, 12/31 1,352 Consolidated Balance Sheet Assets Current assets Cash and cash equivalents Securities available for sale 256 51 Trade accounts receivable. 2,052 Inventories 169 Other current assets 34 Total current assets 2,562 (2) Reconciling Adjustments (3) (4) (1) U.S. IFRS Debit Credit GAAP Non-current assets Property, plant and equipment 11,453 Investments 1,238 Other non-current assets. 220 Total non-current assets 12,911 Total assets 15,473 Liabilities and shareholders' equity Current liabilities Short-term debt Trade accounts payable 1,178 889 Accrued pension cost.. 789 Other current liabilities 2,213 Total current liabilities 5,069 Long-term liabilities Long-term debt .. Finance lease obligation 6,200 439 Accrued pension cost. Accrued liabilities 1,488 709 Other long-term liabilities. Total long-term liabilities 338 9,174 Total liabilities 14,243 Shareholders' equity Retained earnings .. 1,352 Unrealized market value adjustment on securities available for sale Cumulative translation adjustment Total shareholders' equity . 39 (161) 1,230 Total liabilities and shareholders equity 15,473 a) Capitalization of Interest cost Swisscom expenses all interest costs as Incurred. U.S. GAAP requires Interest costs Incurred during the construction of property, plant and equipment to be capitalized. Under U.S. GAAP SWISSCOM would have capitalized CHF 13 million and amortized CHF 5 million for the current year. b) Restructuring charges During the current year, Swisscom recognized under IFRS restructuring charges totaling CHF 1,726 million. The following schedule illustrates adjustments necessary to reconcile these charges to amounts determined under U.S. GAAP. .

> How important is international trade (imports and exports) to the world economy?

> The Financial Times, on Tuesday, April 13, 2004, made the following comment in its editorial “Parmalat: Perennial Lessons of European Scandal: Urgent need for better enforcement and investor scepticism”: After the accounting scandals in the US, there w

> T he objective of convergence between IFRS and U.S. GAAP is no longer a priority for the IASB. Required: Discuss the possible reasons for, and the consequences of, the IASB’s above decision.

> The SEC lifted the requirement for foreign companies that have used IFRS as the basis for preparing their financial statements: that to be eligible to list their shares in U.S. stock exchanges, they should reconcile their financial statements using U.S.

> “The IASB has been repeatedly accused of devising accounting standards that pay insufficient attention to the concerns and practices of companies. Some European banks and insurers complain about poor due process by the IASB, and Frits Bolkestein, Europea

> The IASB’s main objective is to develop a set of high-quality standards for financial reporting by companies at the international level. Required: Critically examine the possibility of achieving this objective.

> Geneva Technology Company (GTC), a Swiss-based company founded in 1999, is considering the use of IFRS in preparing its annual report for the year ended December 31, 2013. You are the manager of GTC’s fixed assets accounting department. Required: Identi

> Five factors are often mentioned as affecting a country’s accounting practices: (a) legal system, (b) taxation, (c) providers of financing, (d) inflation, and (e) political and economic ties. Required: Consider your home country. Identify which of

> Refer to Nobes’s judgmental classification of accounting systems in Exhibit 2.5 and consider the following countries: Austria, Brazil, Finland, Ivory Coast, Russia, and South Africa. Required: Identify the family of accounting in which

> Cultural dimension index scores developed by Hofstede for six countries are reported in the following table: Required: Using Gray’s hypothesis relating culture to the accounting value of secrecy, rate these six countries as relative

> Refer to the income statements presented in Exhibits 2.9, 2.10, 2.11, 2.12, and 2 .13 for Callaway Golf Company, Südzucker AG, Cemex S.A.B. de CV, Sol Meliá SA, and Thai Airways. Required: a. Calculate gross profit margin (g

> Various attempts have been made to reduce the accounting diversity that exists internationally. This process is known as convergence and is discussed in more detail in Chapter 3. The ultimate form of convergence would be a world in which all countries fo

> As noted in the chapter, diversity in accounting practice across countries generates problems for a number of different groups. Required: Answer the following questions and provide explanations for your answers. a. Which is the greatest problem arising

> Astra Zeneca PLC, based in the United Kingdom, and Abbott Laboratories, based in the United States, are two of the largest pharmaceutical firms in the world. The following information was provided in each company’s 2012 annual report.

> The London Stock Exchange (LSE) provides a list of companies listed on the exchange on its Web site (www.londonstockexchange.com) under “Statistics” and “List of Companies.” Required: a. Determine the number of foreign companies listed on the LSE and th

> The New York Stock Exchange (NYSE) provides a list of non-U.S. companies listed on the exchange on its Web site (www.nyse.com). (Hint: Search the Internet for “NYSE List of Non-U.S. Listed Issuers.”) Required: a. Determine the number of foreign companie

> Global Electronics Company (GEC), a U.S. taxpayer, manufactures laser guitars in its Malaysian operation (LG-Malay) at a production cost of $120 per unit. LG Malay guitars are sold to two customers in the United States—Electronic Superstores (a GEC wholl

> Cooper Grant is the president of Acme Brush of Brazil, the wholly owned Brazilian subsidiary of U.S.-based Acme Brush Inc. Cooper Grant’s compensation package consists of a combination of salary and bonus. His annual bonus is calculated as a predetermine

> Sony Corporation reported the following in the Notes to Consolidated Financial Statements included in the company’s 2012 annual report on Form 20-F (p. F-49): Foreign Exchange Forward Contracts and Foreign Currency Option Contracts Foreign exchange forwa

> Sony Corporation reported the following in the summary of Significant Accounting Policies included in the company’s 2012 annual report on Form 20-F (p. F-16): Translation of Foreign Currencies All asset and liability accounts of foreign subsidiaries and

> The IRS has the authority to impose penalties on companies that significantly underpay taxes as a result of inappropriate transfer pricing. Acme Company transfers a product to a foreign affiliate at $15 per unit, and the IRS determines the correct price

> Ranger Company, a U.S. taxpayer, manufactures and sells medical products for animals. Ranger holds the patent on Z-meal, which it sells to horse ranchers in the United States. Ranger Company licenses its Bolivian subsidiary, Yery SA, to manufacture and s

> Denker Corporation has a wholly owned subsidiary in Sri Lanka that manufactures wooden bowls at a cost of $3 per unit. Denker imports the wooden bowls and sells them to retailers at a price of $12 per unit. The following information applies: Import dut

> ABC Company has subsidiaries in Countries X, Y, and Z. Each subsidiary manufactures one product at a cost of $10 per unit that it sells to each of its sister subsidiaries. Each buyer then distributes the product in its local market at a price of $15 per

> Guari Company, based in Melbourne, Australia, has a wholly owned subsidiary in Taiwan. The Taiwanese subsidiary manufactures bicycles at a cost equal to A$20 per bicycle, which it sells to Guari at an FOB shipping point price of A$100 each. Guari pays sh

> Smith-Jones Company, a U.S.-based corporation, owns 100 percent of Joal SA, located in Guadalajara, Mexico. Joal manufactures premium leather handbags at a cost of 500 Mexican pesos each. Joal sells its handbags to SmithJones, which sells them under Joal

> Akku Company imports die-cast parts from its German subsidiary that are used in the production of children’s toys. Per unit, part 169 costs the German subsidiary $1.00 to produce and $0.20 to ship to Akku Company. Akku Company uses part 169 to produce a

> Litchfield Corporation is a U.S.-based manufacturer of fashion accessories that produces umbrellas in its plant in Roanoke, Virginia, and sells directly to retailers in the United States. As chief financial officer, you are responsible for all of the com

> Superior Brakes Corporation manufactures truck brakes at its plant in Mansfield, Ohio, at a cost of $10 per unit. Superior sells its brakes directly to U.S. truck makers at a price of $15 per unit. It also sells its brakes to a wholly owned sales subsidi

> Lahdekorpi OY, a Finnish corporation, owns 100 percent of Three-O Company, a subsidiary incorporated in the United States. Required: Given the limited information provided, determine the best transfer pricing method and the appropriate transfer price in

> Bush Inc. has total income of $500,000. Bush’s Polish branch has foreign source income of $200,000 and paid taxes of $38,000 to the Polish government. The U.S. corporate tax rate is 35 percent. What is Bush’s overall f

> The exchange rate between the U.S. dollar (US$) and the euro (€) remained constant at €1.00 5 US$1.50 throughout 2013. Elizabeth Welch (a U.S. citizen) lives and works in France. In 2013, she earned income in France of €100,000, and paid taxes to the l

> The exchange rate between the U.S. dollar (US$) and the Hong Kong dollar (HK$) remained constant at HK$8.00 5 US$1.00 throughout 2013. Horace Gardner (a U.S. citizen) lives and works in Hong Kong. In 2013, Gardner earned income in Hong Kong of HK$960,000

> Brown Corporation has an affiliate in France (Brun SA) that sells products manufactured at Brown’s factory in Columbia, South Carolina. In the current year, Brun SA earned €10 million before tax. Assume that the effective tax rate Brun SA pays in France

> Use the information provided in problem 25. Now assume that Intec Corporation’s Chinese operation is organized as a branch, and repatriates after-tax profits of RMB 200,000 to Intec on October 1. Required: Determine the following related to the income e

> Intec Corporation (a U.S.-based company) has a wholly owned subsidiary located in Shanghai, China, that generated income before tax of 500,000 Chinese renminbi (RMB) in the current year. The Chinese subsidiary paid Chinese income taxes at the rate of 25

> The corporate income tax rates in two countries, A and B, are 40 percent and 25 percent, respectively. Additionally, both countries impose a 30 percent withholding tax on dividends paid to foreign investors. However, a bilateral tax treaty between A and

> Heraklion Company (a U.S.-based company) is considering making an equity investment in an Australian manufacturing operation. The total amount of capital, in Australian dollars (A$), that Heraklion would need to invest is A$1,000,000. Heraklion has three

> .S. International Corporation (USIC), a U.S. taxpayer, has investments in Foreign Entities A–G. Relevant information for these entities for the current fiscal year appears in the following table: Additional Information 1. USICâ&

> Eastwood Company (a U.S.-based company) has subsidiaries in three countries: X, Y, and Z. All three subsidiaries manufacture and sell products in their host country. Corporate income tax rates in these three countries over the most recent three-year peri

> Pendleton Company (a U.S. taxpayer) is a highly diversified company with wholly owned subsidiaries located in South Korea and Japan. The South Korean operation manufactures electric generators that are sold in the Asian market. It generated pretax income

> Daisan Company is in the process of deciding where to establish a European manufacturing operation: France, Spain, or Sweden. Daisan’s home country does not have a tax treaty with any of these countries. Regardless of location, the operation is expected

> Avioco Limited has two branches located in Hong Kong and Australia, each of which manufactures goods primarily for export to countries in the Asia Pacific region. The corporate income tax rate in Avioco’s home country is 20 percent. The

> Lionais Company has a foreign branch that earns income before income taxes of 500,000 currency units (CU). Income taxes paid to the foreign government are CU 150,000 (30 percent). Sales and other taxes paid to the foreign government are CU 50,000. Lionai

> Mama Corporation (a U.S. taxpayer) has a wholly owned sales subsidiary in the Bahamas (Bahamamama Ltd.) that purchases finished goods from its U.S. parent and sells those goods to customers throughout the Caribbean basin. In the most recent year, Bahamam

> Assume that Yankee’s operation in Great Britain is incorporated as a subsidiary. Required: Determine the amount of U.S. taxable income, U.S. foreign tax credit, and net U.S. tax liability related to the British subsidiary (all in U.S. dollars).

> Assume that Yankee’s operation in Great Britain is registered with the British government as a branch. Required: Determine the amount of U.S. taxable income, U.S. foreign tax credit, and net U.S. tax liability related to the British branch (all in U.S.

> Bay City Rollers Inc., a U.S. company, has a branch located in São Antonio and another in the Bahian Islands. The foreign source income from the São Antonio branch is $150,000, and the foreign source income from the Bahian Island branch is $225,000. The

> Gamma Holding NV, a Dutch textile company, presented the following calculation of operating profit in its 2009 consolidated income statement: € × 1,000,000 2009 Net turnover……&

> Gamma Holding NV, a Dutch textile company, provided the following information in its consolidated income statement for the year 2009 (note that “result” is equivalent to “income”):

> The following excerpts were taken from the notes to consolidated financial statements in the 2006 annual report of the Novartis Group, the Swiss pharmaceutical company: Required: a. Determine whether the adjustments described in Note 33.9, Share-Based

> China Eastern Airlines (CEA) Corporation Limited prepares a set of financial statements in accordance with IFRS (in Chinese renminbi—RMB). Until 2007, the company also provided a reconciliation of IFRS net income and net assets to U.S.

> China Eastern Airlines (CEA) Corporation Limited presents two sets of financial statements in its annual report; one set is prepared in accordance with Chinese (PRC) accounting regulations, and one set is prepared in accordance with International Financi

> The parent company balance sheet for Babcock International Group PLC at March 31, 2010, is as follows: Required: Transform Babcock’s March 31, 2010, balance sheet to a U.S. format. Balance Sheet As at 31 March 2009 2009 2008 Notes

> SABMiller PLC was formed when U.S.-based Miller Brewing Company merged with South African Breweries in 2002. SABMiller uses IFRS in preparing its financial statements. The following is taken from the March 31, 2010, consolidated balance sheet of SABMille

> China Petroleum & Chemical Corporation (Sinopec) provides two sets of financial statements in its annual report. One set of financial statements is prepared in accordance with Chinese (PRC) Accounting Rules and Regulations, and the other is prepared

> Refer to the following information provided in the chapter for Arcot Company: • Consolidated financial statements in Exhibits 10.8 and 10.9. • Differences between Local GAAP and U.S. GAAP in Exhibit 10.10.

> Refer to the following information provided in the chapter for Arcot Company: • Consolidated financial statements in Exhibits 10.8 and 10.9. • Differences between Local GAAP and U.S. GAAP in Exhibit 10.10.

> Vale S.A., a Brazilian mineral products company, provided the following note on a voluntary basis in its 2009 annual report: 11—Cash Generation (Unaudited) Consolidated operating cash generation measured by EBITDA (earnings before fi na

> Palmers town Company established a subsidiary in a foreign country on January 1, Year 1, by investing 8,000,000 pounds when the exchange rate was $1.00/pound. Palmers town negotiated a bank loan of 4,000,000 pounds on January 5, Year 1, and purchased pla

> The consolidated income statement for Babcock International Group PLC is presented here: The income statement does not disclose any detail on the operating expenses that were subtracted in determining operating profit, but refers readers to several not

> The following Statement of Added Value (in millions of Brazilian reals) was presented in the 2009 annual report of Vale S.A., a Brazilian mineral products company: Required: a. Identify the external parties who might be interested in the information p

> Neopost SA is a French company operating mainly in Europe and the United States that sells and leases mailroom equipment. In accordance with IFRS, the company capitalizes development costs when certain criteria are met. The company reported the following

> Refer to the worksheets in Exhibits 10.12 and 10.13 in which the financial statements of Arcot Company have been restated to U.S. GAAP. Required: a. Calculate each of the ratios listed below using (1) the Local GAAP amounts in Column 1, and (2) the U.S.

> Geographic segment information can be used to determine how multinational a company is and the extent to which a company is diversified internationally. Refer to the geographic segment information provided by three U.S. companies in Exhibit 9.9. Require

> Iskender Corporation is a Turkish conglomerate with operations located throughout Europe and the Middle East. The company recently adopted International Financial Reporting Standards and has prepared disclosures to comply with IFRS 8, Operating Segments.

> Horace Jones Company consists of six business segments. The consolidated income statement as well as information about each of the segments for Year 1 as reported to the chief executive officer is as follows: HORACE JONES COMPANY Consolidat

> Sandestino Company contributes cash of $170,000 and Costa Grande Company contributes net assets of $170,000 to create Grand Sand Company on January 1, Year 1. Sandestino and Costa Grande each receive a 50 percent equity interest in Grand Sand. Grand Sand

> Auroral Company had the following investments in shares of other companies on December 31, Year 1: Required: Determine the appropriate method for including each of these investments in Auroral Company’s consolidated financial statem

> Petrodat Company provides data processing services for companies operating in the petroleum extraction business. On January 1, Year 1, Petrodat established two foreign subsidiaries—one in Mexico and the other in Venezuelaâ€&

> Columbia Corporation, a U.S.-based company, acquired a 100 percent interest in Swoboda Company in Lodz, Poland, on January 1, Year 1, when the exchange rate for the Polish zloty (PLN) was $0.25. The financial statements of Swoboda as of December 31, Year

> Doner Company Inc. begins operations on January 1, Year 1. The company’s unadjusted financial statements for the year ended December 31, Year 1, appear as follows: Revenues and expenses occur evenly throughout the year; revenues and o

> Antalya Company borrows 1,000,000 Turkish lire (TL) on January 1, Year 1, at an annual interest rate of 60 percent by signing a two-year note payable. During Year 1, the Turkish inflation index changed from 250 at January 1 to 387.5 at December 31. Req

> The following geographic segment information is provided in the 2012 annual report by two German automakers, BMW and Volkswagen: Required: Use the 2012 segment information provided by BMW and Volkswagen to answer the following questions: a. Which

> Sorocaba Company is located in a highly inflationary country and in accordance with IAS 29 prepares financial statements on a general purchasing power (inflation-adjusted) basis through reference to changes in the general price index (GPI). The company h

> The Year 1 financial statements of the Brazilian subsidiary of Artemis Corporation (a Canadian company) revealed the following: Brazilian Reals (BRL) Beginning inventory………………………………………………..100,000 Purchases………………………………………………………………500,000 Ending inventor

> Selected balance sheet accounts of a foreign subsidiary of the Pacter Company have been translated into parent currency ( F - ) as follows: Required: a. Assuming that the foreign subsidiary is determined to have the foreign currency as its functional

> To complete the requirements of this exercise, access the most recent Form 10-K for both Exxon Mobil and Chevron. Required: a. Determine whether each company’s foreign operations have a predominant functional currency. Discuss the implication this has f

> Brookhurst Company (a U.S.-based company) established a subsidiary in South Africa on January 1, Year 1, by investing 300,000 South African rand (ZAR) when the exchange rate was US$0.09/ZAR 1. On that date, the foreign subsidiary borrowed ZAR 500,000 fro

> Gramado Company was created as a wholly owned subsidiary of Porto Alegre Corporation on January 1, Year 1. On that date, Porto Alegre invested $42,000 in Gramado’s capital stock. Given the exchange rate on that date of $0.84 per cruzeiro, the initial inv

> Alexander Corporation (a U.S.-based company) acquired 100 percent of a Swiss company for 8.2 million Swiss francs on December 20, Year 1. At the date of acquisition, the exchange rate was $0.70 per franc. The acquisition price is attributable to the foll

> Better Food Corporation (BFC) regularly purchases nutritional supplements from a supplier in Japan with the invoice price denominated in Japanese yen. BFC has experienced several foreign exchange losses in the past year due to increases in the U.S.-dolla

> Zesto Company (a U.S. company) establishes a subsidiary in Mexico on January 1, Year 1. The subsidiary begins the year with 1,000,000 Mexican pesos (MXN) in cash and no other assets or liabilities. It immediately uses MXN600,000 to acquire equipment. Inv

> Alliance Corporation (an Australian company) invests 1,000,000 marks in a foreign subsidiary on January 1, Year 1. The subsidiary commences operations on that date, and generates net income of 200,000 marks during its first year of operations. No dividen

> Simga Company’s Turkish subsidiary reported the following amounts in Turkish lire (TL) on its December 31, Year 4, balance sheet: Equipment…………â€

> What is the net impact on Black Lion Company’s Year 1 net income as a result of this hedge of a forecasted foreign currency purchase? a. $0. b. A $200 increase in net income. c. A $300 decrease in net income. d. An $800 decrease in net income.

> What was the net increase or decrease in cash flow from having purchased the foreign currency option to hedge this exposure to foreign exchange risk? a. $0. b. A $1,000 increase in cash flow. c. A $1,700 decrease in cash flow. d. A $2,300 increase in cas

> What was the net impact on Keefer Company’s Year 1 income as a result of this fair value hedge of a firm commitment? a. $0. b. An $860.60 decrease in income. c. An $1,100.00 increase in income. d. A $1,960.60 increase in income.

> Assuming a forward contract to sell 100,000 Israeli shekels was entered into on December 1, Year 1, as a fair value hedge of a foreign currency receivable, what would be the net impact on net income in Year 1 resulting from a fluctuation in the value of

> Given its experience, Garnier Corporation expects that it will sell goods to a foreign customer at a price of 1 million lire on March 15, Year 2. To hedge this forecasted transaction, a three-month put option to sell 1 million lire is acquired on Decembe

> The Zermatt Company ordered parts from a foreign supplier on November 20 at a price of 100,000 francs when the spot rate was $0.80 per peso. Delivery and payment were scheduled for December 20. On November 20, Zermatt acquired a call option on 100,000 fr

> On June 1, Year 1, Tsanumis Corporation (a U.S.-based manufacturing fi rm) received an order to sell goods to a foreign customer at a price of 1 million euros. The goods will be shipped and payment will be received in three months on September 1, Year 1.

> Portofi no Company made purchases on account from three foreign suppliers on December 15, 2012, with payment made on January 15, 2013. Information related to these purchases is as follows: Portofi no Company’s fiscal year ends Decem

> After evaluating the risk of the investment described in Exercise 25-8, B2B Co. concludes that it must earn at least an 8% return on this investment. Compute the net present value of this investment. (Round the net present value to the nearest dollar.)

> Keith Riggins expects an investment of $82,014 to return $10,000 annually for several years. If Riggins earns a return of 10%, how many annual payments will he receive? (Use Table B.3.) Table B.3: ТАBLE B.3t p = | 1 /i (1 + i)". Present Value of an

> Jones expects an immediate investment of $57,466 to return $10,000 annually for eight years, with the first payment to be received one year from now. What rate of interest must Jones earn? (Use Table B.3.) Table B.3: ТАBLE B.3t p = | 1 /i (1 + i)".

> Catten, Inc., invests $163,170 today earning 7% per year for nine years. Use Table B.2 to compute the future value of the investment nine years from now. (Round the amount to the nearest dollar.) Table B.2: ТABLE B.2** f = (1 + i)" Future Value of

> Mark Welsch deposits $7,200 in an account that earns interest at an annual rate of 8%, compounded quarterly. The $7,200 plus earned interest must remain in the account 10 years before it can be withdrawn. How much money will be in the account at the end

> Bill Padley expects to invest $10,000 for 25 years, after which he wants to receive $108,347. What rate of interest must Padley earn? (Use Table B.2.) Table B.2: ТABLE B.2** f = (1 + i)" Future Value of 1 Rate Periods 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

> Tom Thompson expects to invest $10,000 at 12% and, at the end of a certain period, receive $96,463. How many years will it be before Thompson receives the payment? (Use Table B.2.) Table B.2: ТABLE B.2** f = (1 + i)" Future Value of 1 Rate Periods