Question: The Brant Group reported total interest expense

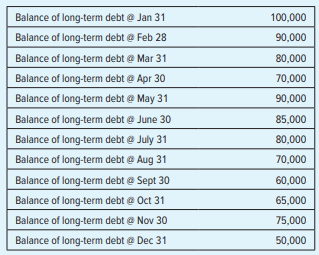

The Brant Group reported total interest expense for the year of $2,000. The table below provides the monthly balance of their long-term debt. Interest is paid monthly on the average daily balance during the month. The annual interest rate for the debt is 6%.

Required:

Based on the data provided, if you were auditing The Brant Group would you consider the reported interest expense fairly stated? Why or why not?

Transcribed Image Text:

Balance of long-term debt e Jan 31 100,000 Balance of long-term debt e Feb 28 90,000 Balance of long-term debt e Mar 31 80,000 Balance of long-term debt e Apr 30 70,000 Balance of long-term debt e May 31 90,000 Balance of long-term debt e June 30 85,000 Balance of long-term debt e July 31 80,000 Balance of long-term debt e Aug 31 70,000 Balance of long-term debt e Sept 30 60,000 Balance of long-term debt e Oct 31 65,000 Balance of long-term debt e Nov 30 75,000 Balance of long-term debt e Dec 31 50,000

> In February 2019, Ceramic Crucibles of America was notified by the state of Colorado that the state was investigating the company’s Durango facility to determine if there were any violations of federal or state environmental laws. In formulating your opi

> Wyly Waste Management (“WWM”) is an SEC registrant and your firm is its auditor. Overall materiality for the audit is $100,000. Shortly after the end of the year, WWM’s CFO is meeting with your audit partner to review the preliminary results of the audit

> Medical Products, Inc. (MPI) was created in 2016 and entered the optical equipment industry. Its made-to-order optical equipment requires large investments in research and development. To fund these needs, MPI made a public stock offering, which was comp

> How does the purchasing process affect prepaid insurance and property, plant, and equipment transactions?

> On January 15, 2018, Leno, Inc., which has a March 31 year-end, entered into a transaction to sell the land and building that contained its manufacturing operations for a total selling price of $19,750,000. The book value of the land and the building was

> Pierce, an independent auditor, was engaged to examine the financial statements of Wong Construction, Inc., for the year ended December 31. Wong’s financial statements reflect a substantial amount of mobile construction equipment used in the firm’s opera

> The long-term debt working paper shown below was prepared by entity personnel and audited by Andy Fogelman, an audit assistant, during the calendar year 2018 audit of American Widgets, Inc., a continuing audit client. The engagement supervisor is reviewi

> The FASB’s revised standard on leases, ASC 842, was effective for public companies beginning 2018. One significant implication of this standard is that operating leases that were previously kept off the balance sheet are now required to be recorded on th

> What types of services can be performed under Statements on Standards for Accounting and Review Services?

> For what types of actions are auditors liable to a client under common law? Why would the client prefer to sue the auditor for a tort action rather than for a breach of contract?

> The questions that follow are based on the Independence Rule of the AICPA Code of Professional Conduct as it relates to independence and family relationships. Check yes if the situation violates the rule, no if it does not. Situation Yes No a. A par

> To support financial statement assertions, an auditor develops specific audit procedures to satisfy or accomplish each assertion. Required: Items (a) through (c) represent assertions for investments. Select the most appropriate procedure from the follow

> Items 1 through 16 represent a series of unrelated statements, questions, excerpts, and comments taken from various parts of an auditor’s working paper file. Below items 1 through 16 is a list of the likely sources of the statements, questions, excerpts,

> To support financial statement assertions, an auditor develops specific substantive procedures to satisfy or address each assertion. Required: Items (a) through (c) represent assertions for the property and equipment accounts. Select the most appropriat

> The following client-prepared bank reconciliation is being examined by Zachary Kallick, CPA, during the examination of the financial statements of Simmons Company. Required: Items (a) through (e) represent items an auditor would ordinarily find on an e

> The tick mark ▲ most likely indicates that the amount was traced to the a. Deposit in transit of the applicable bank reconciliation. b. December cash receipts journal. c. January cash receipts journal. d. Year-end bank confirmations.

> On September 10, Melinda Johnson was auditing the financial statements of a new audit client, Mother Earth Foods, a health-food chain that has a June 30 year-end. The company is privately held and has just gone through a leveraged buyout with long-term f

> Which of the following comparisons would be most useful to an auditor in evaluating the overall financial results of an entity’s operations? a. Prior-year accounts payable to current-year accounts payable. b. Prior-year payroll expense to budgeted curren

> Under which conditions would an online dating company be more likely to opt for a SOC 3 report over a SOC 2 report? a. The company wishes the report to be distributed only to a restricted set of users who understand the details of the IT system being rep

> Which of the following is true of a SOC 2 engagement? a. The report resulting from a SOC 2 engagement can be made available for general use. b. A SOC 2 engagement is based on criteria from COSO’s internal control framework. c. A SOC 2 engagement is based

> Which of the following assurances is not provided by compliance with Trust Services principles? a. There are procedures to protect the system against unauthorized physical access. b. The financial statements created by the system are free of material mis

> Which of the following is not a Trust Services principle? a. Processing integrity. b. Privacy. c. Digital certificate authorization. d. Availability.

> The four principles of the IIA Code of Ethics are a. Confidentiality, competency, objectivity, and integrity. b. Objectivity, independence, compliance, and due diligence. c. Honesty, integrity, independence, and competency. d. Integrity, confidentiality,

> Which of the following is not one of the general areas of the IIA’s International Standards for the Professional Practice of Internal Auditing? a. Performance standards. b. Implementation standards. c. Ethical standards. d. Attribute standards.

> The general accreditation granted by the Institute of Internal Auditors is known as a. CFE. b. CGAP. c. CFSA. d. CIA.

> Financial statements that have been reviewed by an accountant should be accompanied by a report stating that a. The scope of the inquiry and the analytical procedures performed by the accountant have not been restricted. b. All information included in th

> The standard report issued by an accountant after reviewing financial statements states that a. A review includes assessing the accounting principles used and significant estimates made by management. b. A review includes examining, on a test basis, evid

> Taylor, CPA, has been engaged to audit the financial statements of Palmer Company, a continuing audit client. Taylor is about to perform substantive audit procedures on Palmer’s goodwill (excess of cost over fair value of net assets purchased) and tradem

> Which of the following statements is correct concerning both an engagement to compile and an engagement to review a non-public entity’s financial statements? a. The accountant is not required to obtain an understanding of internal control. b. The account

> When compiling the financial statements of a non-public entity, an accountant should a. Review agreements with financial institutions for restrictions on cash balances. b. Understand the accounting principles and practices of the entity’s industry. c. In

> Which of the following statements concerning prospective financial statements is correct? a. Only a financial forecast would normally be appropriate for limited use. b. Only a financial projection would normally be appropriate for general use. c. Any typ

> An accountant may accept an engagement to apply agreed-upon procedures to prospective financial statements, provided that a. The prospective financial statements are also examined. b. Responsibility for the adequacy of the procedures performed is taken b

> Which of the following professional services would be considered an attest engagement? a. A management consulting engagement to provide IT advice to a client. b. An engagement to report on compliance with statutory requirements. c. An income tax engageme

> An assurance report on information can provide assurance about the information’s a. Reliability. b. Relevance. c. Timeliness. d. All of the above.

> Which of the following is a provision of the Foreign Corrupt Practices Act? a. It is a criminal offense for an auditor to fail to detect and report a bribe paid by an American business entity to a foreign official for the purpose of obtaining business. b

> Which of the following is not a provision of the Sarbanes-Oxley Act? a. A requirement to retain audit work papers for at least five years. b. It is a criminal offense to take any harmful action in retaliation against anyone who voluntarily comes forward

> Under the Private Securities Litigation Reform Act, Baker, CPA, reported certain uncorrected illegal acts to Super mart’s board of directors. Baker believed that failure to take remedial action would warrant a qualified audit opinion because the illegal

> Fritz Corporation, whose shares are publicly traded, engaged Hay Associates, CPAs, to audit its financial statements. Hay gave an unqualified opinion, despite knowing that the financial statements contained misstatements. Hay’s opinion was included in Fr

> Natherson, CPA, is engaged to audit the financial statements of Lewis Lumber for the year ended December 31. Natherson obtained and documented an understanding of internal control relating to the purchasing process and set control risk at the maximum lev

> If Hansen succeeds in the Section 11 suit against Dart, Hansen will be entitled to a. Damages of three times the original public offering price. b. Rescind the transaction. c. Monetary damages comparable to the loss suffered. d. Damages, but only if the

> In a suit against Jay and Dart under the Section 11 liability provisions of the Securities Act of 1933, Hansen must prove that a. Jay knew of the misstatements. b. Jay was negligent. c. The misstatements contained in Dart’s financial statements were mate

> To be successful in a civil action under Section 11 of the Securities Act of 1933 concerning liability for a misleading registration statement, the plaintiff must prove Defendant's Intent Plaintiff's Reliance on the to Deceive Registration Statemen

> How does the Securities Act of 1933, which imposes civil liability on auditors for misrepresentations or omissions of material facts in a registration statement, expand auditors’ liability to purchasers of securities beyond that of common law? a. Purchas

> Brown & Company, CPAs, issued an unqualified opinion on the financial statements of its client King Corporation. Based on the strength of King’s financial statements, Safe Bank loaned King $500,000. King Corporation and Safe Bank are both located in a st

> Jenna Corporation approved a merger plan with Cord Corporation. One of the determining factors in approving the merger was the financial statements of Cord, which had been audited by Frank & Company, CPAs. Jenna had engaged Frank to audit Cord’s financia

> Which of the following best describes whether a CPA has met the required standard of care in auditing an entity’s financial statements? a. Whether the client’s expectations are met with regard to the accuracy of audited financial statements. b. Whether t

> Cable Corporation orally engaged Drake & Company, CPAs, to audit its financial statements. Though the financial statements Drake audited included a materially overstated accounts receivable balance, Drake issued an unqualified opinion. Cable used the fin

> In connection with the element of engagement performance, a CPA firm’s system of quality control should ordinarily include procedures covering all of the following except a. Performance evaluation. b. Consistent, high-quality engagement performance. c. S

> One of a CPA firm’s basic objectives is to provide professional services that conform with professional standards. Reasonable assurance of achieving this basic objective is provided through a. A system of quality control. b. A system of peer review. c. C

> Without the consent of the entity, a CPA should not disclose confidential entity information contained in working papers to a(n) a. Authorized quality control review board. b. Successor CPA firm that has been engaged to audit the former audit entity. c.

> During the audit of Moon Co., the auditor disagrees with management’s estimation of collectible accounts receivable. The possible misstatement amount is material. Which of the statements below should weigh most heavily for the auditor in this instance? a

> Rick, an independent CPA, must make an ethical judgment related to the audit of an entity. If he primarily focuses on whether his decision might yield unfair advantages for some at the expense of others, he is using a. A utilitarian perspective. b. A rig

> A violation of the profession’s ethical standards is least likely to occur when a CPA a. Purchases another CPA’s accounting practice and bases the price on a percentage of the fees accruing from entities over a three-year period. b. Receives a percentag

> Which of the following legal situations would be considered to impair the auditor’s independence? a. An expressed intention by the present management to commence litigation against the auditor, alleging deficiencies in audit work for the entity, although

> An audited company has not paid its 2018 audit fees. According to the AICPA Code of Professional Conduct, for the auditor to be considered independent with respect to the 2019 audit, the 2018 audit fees must be paid before the a. 2018 report is issued. b

> In which of the following situations would a CPA’s independence be considered impaired according to the Code of Professional Conduct? 1. The CPA has a car loan from a bank that is an audit entity. The loan was made under the same terms available to all c

> The AICPA Code of Professional Conduct contains both general ethical principles that are aspirational in character and a a. List of violations that would cause the automatic suspension of a CPA’s license. b. Set of specific, mandatory rules describing mi

> Under the SEC’s rules regarding independence, which of the following must an entity disclose? a. Only fees for the external audit. b. Only fees for internal and external audit services provided by the audit firm. c. Fees for the external audit, audit-rel

> All of the following non audit services are identified by the SEC as generally impairing an auditor’s independence with respect to an audited entity except a. Information systems design and implementation. b. Human resource services. c. Management functi

> Maslovskaya, CPA, has been engaged to examine the financial statements of Broadwall Corporation for the year ended December 31, 2018. During the year, Broadwall obtained a long-term loan from a local bank pursuant to a financing agreement that provided t

> Which of the following statements best explains why public accounting, as a profession, promulgates ethical standards and establishes means for ensuring their observance? a. Vigorous enforcement of an established code of ethics is the best way to prevent

> When an auditor is asked to express an opinion on an entity’s rent and royalty revenues, he or she may a. Not accept the engagement because to do so would be tantamount to agreeing to issue a piecemeal opinion. b. Not accept the engagement unless also en

> When reporting on financial statements prepared on the basis of accounting used for income tax purposes, the auditor should include in the report a paragraph that a. Emphasizes that the financial statements have not been examined in accordance with gener

> Which of the following best describes the auditor’s responsibility for “other information” included in the annual report to stockholders that contains financial statements and the auditor’s report? a. The auditor has no obligation to read the “other info

> When reporting on comparative financial statements, which of the following circumstances should ordinarily cause the auditor to change the previously issued opinion on the prior year’s financial statements? a. The prior year’s financial statements are re

> Comparative financial statements for a public company include the prior year’s financial statements, which were audited by a predecessor auditor. The predecessor’s report is not presented along with the comparative financial statements. If the predecesso

> King, CPA, was engaged to audit the financial statements of Chang Company, a private company, after its fiscal year had ended. King neither observed the inventory count nor confirmed the receivables by direct communication with debtors but was satisfied

> In which of the following circumstances would an auditor usually choose between issuing a qualified opinion or a disclaimer of opinion on a client’s financial statements? a. Departure from generally accepted accounting principles. b. Inadequate disclosur

> Tech Company has appropriately disclosed an uncertainty due to pending litigation. However, the auditor was unable to satisfy herself that all pending litigation had been identified. The auditor’s decision to issue a qualified opinion on Tech’s financial

> Eagle Company, a public company, had a computer failure and lost part of its financial data. As a result, the auditor was unable to obtain sufficient audit evidence relating to Eagle’s inventory account. Assuming the inventory account is at least materia

> How does the fair value evidence the auditor is likely to gather differ between Level 1 and Level 3 assets?

> Why does the auditor generally follow a substantive strategy when auditing long-term debt and capital accounts? Under what conditions might the auditor follow a reliance strategy?

> An auditor includes a separate paragraph in an otherwise unmodified financial statement audit report to emphasize that the entity being reported upon had significant transactions with related parties. The inclusion of this separate paragraph a. Is approp

> A public entity changed from the straight-line method to the declining balance method of depreciation for all newly acquired assets. This change has no material effect on the current year’s financial statements but is reasonably certain to have a substan

> Which of the following events occurring after the issuance of a set of financial statements and the accompanying auditor’s report would be most likely to cause the auditor to make further inquiries about the financial statements? a. A technological devel

> Which of the following matters should an auditor communicate to those charged with governance? Significant Audit Adjustments Management's Consultations with Other Accountants a. Yes Yes b. Yes No Yes С. No d. No No

> Auditing standards primarily encourage which of the following conversations between the auditor and another party about financial reporting? a. A conversation with those charged with governance to discuss matters pertaining to financial reporting. b. A c

> Which of the following audit procedures is most likely to assist an auditor in identifying conditions and events that may indicate substantial doubt about an entity’s ability to continue as a going concern? a. Review compliance with the terms of debt agr

> Final analytical procedures are generally intended to a. Provide the auditor with a final, overall evaluation of the relationships among financial statement balances. b. Test transactions to corroborate management’s financial statement assertions. c. Gat

> Which of the following procedures would an auditor most likely perform to obtain evidence about the occurrence of any changes in internal control that might affect financial reporting between the end of the reporting period and the date of the auditor’s

> An auditor issued an audit report that was dual dated for a subsequent event occurring after the date on which the auditor has obtained sufficient appropriate audit evidence but before issuance of the financial statements. The auditor’s responsibility fo

> An auditor should request that an audited entity send a letter of inquiry to those attorneys who have been consulted concerning litigation, claims, or assessments. The primary reason for this request is to provide a. The opinion of a specialist as to whe

> What two presentation classification issues are important for the audit of debt investments?

> An auditor would be most likely to identify a contingent liability by obtaining a(n) a. Accounts payable confirmation. b. Bank confirmation of the entity’s cash balance. c. Letter from the entity’s general legal counsel. d. List of subsequent cash receip

> The audit firm’s valuation specialist would likely be brought in to assist in the audit of fair value measurements at an entity when the following is present: a. The entity is a new audit client. b. Significant uncertainty exists in key inputs to the ent

> An auditor would most likely verify the interest earned on bond investments by a. Vouching the receipt and deposit of interest checks. b. Confirming the bond interest rate with the issuer of the bonds. c. Re computing the interest earned on the basis of

> Which of the following is likely to be the most effective audit procedure for verifying dividends earned on investments in publicly traded equity securities? a. Trace deposits of dividend checks to the cash receipts book. b. Reconcile recorded earnings w

> To establish the existence and rights of a long-term investment in the common stock of a publicly traded company, an auditor ordinarily performs a security count or a. Relies on the entity’s internal controls if the auditor has reasonable assurance that

> An auditor testing long-term investments would ordinarily use substantive analytical procedures to ascertain the reasonableness of the a. Existence of unrealized gains or losses in the portfolio. b. Completeness of recorded investment income. c. Classifi

> Which of the following controls would most effectively ensure that the proper custody of assets in the investing process is maintained? a. Direct access to securities in the safe-deposit box is limited to one corporate officer. b. Personnel who post inve

> Which of the following cash transfers results in a misstatement of cash at December 31? Bank Transfer Schedule Disbursing Bank Account Receiving Bank Account Recorded in Client's Books Paid by Bank Recorded in Client's Books Recelved by Bank Transfe

> On receiving the cutoff bank statement, the auditor should vouch a. Deposits in transit on the year-end bank reconciliation to deposits in the cash receipts journal. b. Checks dated before year-end listed as outstanding on the year-end bank reconciliatio

> The primary evidence regarding year-end bank balances is documented in the a. Standard bank confirmations. b. Outstanding check listing. c. Interbank transfer schedule. d. Bank deposit lead schedule.

> How does an entity’s controls over cash receipts and disbursements affect the nature and extent of the auditor’s substantive tests of cash balances?

> An auditor ordinarily sends a standard confirmation request to all banks with which the entity has done business during the year under audit, regardless of the year-end balance. One purpose of this procedure is to a. Provide the data necessary to prepare

> Over the past 10 years it has become quite common for an accounting firm to withdraw its opinion on a set of previously issued financial statements. Search the Internet to find a recent example of a company that has had to restate its financials and whos

> The tick mark ⧫ most likely indicates that the amount was traced to the a. December cash disbursements journal. b. Outstanding check list of the applicable bank reconciliation. c. January cash disbursements journal. d. Year-end bank confirmations.

> Visit the SEC’s website (www.sec.gov), and identify a company that has been recently cited for problems related to property, plant, and equipment or lease accounting (e.g., in years past, many retail companies had to restate earnings to comply with the S

> An auditor compares the current-year revenues and expenses with those of the prior year and investigates all changes exceeding 5 percent. By this procedure, the auditor would be most likely to learn that a. Fourth-quarter payroll taxes in the current yea

> Although the quantity and content of audit working papers vary with each particular engagement, an auditor’s permanent files most likely include a. Schedules that support the current year’s adjusting entries. b. Prior years’ accounts receivable confirmat