Question: The following are independent situations for which

The following are independent situations for which you will recommend an appropriate audit report on internal control over financial reporting as required by PCAOB auditing standards:

1. During interim testing, the auditor identified and communicated to management a significant control deficiency. Management immediately corrected the deficiency and the auditor was able to sufficiently test the newly instituted internal control before the end of the fiscal period.

2. As a result of performing tests of controls, the auditor identified a significant deficiency in internal control over financial reporting; however, the auditor does not believe that it represents a material weakness in internal control.

3. The auditor determined that a deficiency in internal control exists that will not prevent or detect a material misstatement in the financial statements.

4. The auditor identified several significant deficiencies in internal control. Because of these significant deficiencies, the auditor believes that there is a reasonable possibility that internal control will not prevent or detect material misstatements on a timely basis.

5. The auditor was unable to obtain any evidence about the operating effectiveness of internal control over financial reporting.

6. The auditor identified a material misstatement in the financial statements that was not detected by management of the company.

Required:

For each situation, state the appropriate audit report from the following alternatives:

• Unqualified opinion on internal control over financial reporting

• Qualified or disclaimer of opinion on internal control over financial reporting

• Adverse opinion on internal control over financial reporting

Transcribed Image Text:

Date MEDIUM-SIZED MANUFACTURING COMPANY Prapared by FLOWCHART OF RAW MATERIALS PURCHASING FUNCTION Аpproved by MANUFACTURING DIVISION ACCOUNTS PAYABLE STORES PURCHASE OFFICE RECEIVING ROOM ICONTROLLER'S DIVISION Purchs quann Purches A quon Purchae By mquttkon raguation B Purca ordar raquition Purchase order vandon Purchane Purchaee nder order Purdue aquitition purdue order Purchase Arandar mquition. Purchwe ardar Purchan order Purchan ordar Reg D Rag- Prshe arder By purdan, order Purchass ordar Racaiving Explanatory Notas Racalving report A Prepre purchana requen Pcopiaa) a readad. B. Propare purchas rder Purchan order raport Inv. Reg C. Arach purche raquaken arde From Receing D purchan o Marchandan recaived, ad wd r grapere By vandor yandon repar Voucher with doom I copiea) prepared Eaned on cou and purchn order. Much purhan orda purchuan requtikion recalving raport, and invoica. F. Prepare voucheraftar comparing daa on purchaan ordeg invoica, recalving raport G. To auh daburem coneroller's diviaion for Ivaice Е. E Raclving Raaving raport raport PO. Pymen. Rag. Rag - Purcha reguition PO. - Rurchuan order Iw.- Ivoka Ey Aprdan order

> What types of sequences constitute most of a bacterial genome?

> What are the base-pairing rules for RNA?

> What types of bonds hold nucleotides together in an RNA strand?

> What are the structural differences between B DNA and Z DNA?

> Describe the major and minor grooves.

> What holds the DNA strands together?

> Which components of nucleotides form the backbone of a DNA strand?

> Which of these components of nucleotides are not found in DNA?

> What was the purpose of adding RNase or protease to a DNA extract?

> What is the role of peptidyl transferase during the elongation stage?

> Explain why a triploid individual is usually infertile.

> What are some common advantages of polyploidy in plants?

> Approximately how many copies of chromosome 2 are found in a polytene chromosome in Drosophila?

> Describe the imbalance in gene products that occurs in an individual with monosomy 2.

> Explain why the mouse in part (d) died.

> What adjectives can be used to describe a fruit fly that has a total of seven chromosomes because it is missing one copy of chromosome 3?

> Explain why these chromosomes form a translocation cross during prophase of meiosis I.

> If these segregation patterns are equally likely, what is the probability that a gamete produced by the individual who carries the translocated chromosome will result in a viable offspring with a normal phenotype?

> Which of these two mechanisms might be promoted by the presence of the same transposable element in many places in a species’ genome?

> Explain why these homologous chromosomes can synapse only if an inversion loop forms.

> Why does a bacterial mRNA bind specifically to the small ribosomal subunit?

> In this example, what is the underlying cause of nonallelic homologous recombination?

> Why is a chromosomal fragment without a centromere subsequently lost and degraded?

> Which of these changes in chromosome structure alter the total amount of genetic material?

> Why is it useful to stain chromosomes?

> Transduction is sometimes described as a mistake in the bacteriophage reproductive cycle. Explain how it can be viewed as a mistake.

> Which of these two genes is closer to the origin of transfer?

> Why is the scale of this map in minutes?

> With regard to the timing of conjugation, explain why the recipient cell at the top right is pro−, whereas the recipient cell in the bottom right is pro+.

> How is an F′ factor different from an F factor?

> What are the functions of relaxase, coupling factor, and the exporter in the process of conjugation?

> Explain how mRNA plays a role in all three stages of translation.

> Which disease occurs when homogentisic acid oxidase is defective?

> What is the role of the shipping document in invoicing customers? What are the most important management assertions related to customer billing?

> Ann Donnelly is a senior audit manager in an East Coast office of a public accounting firm. Her prospects for promotion to partner are excellent if she continues to perform at the same high-quality level as in the past. Ann was recently married, and she

> Barbara Whitley had great expectations about her future as she sat in her graduation ceremony in May 2018. She was about to receive her Master of Accounting degree, and in the next week she would begin her career on the audit staff of Green, Thresher & C

> The information technology (IT) department at Jacobsons, Inc., consists of eight employees, including the IT manager, Melinda Cullen. Cullen is responsible for the day-to-day oversight of the IT function and reports to Jacobsons’ chief operating officer

> McClain Plastics has been an audit client of Belcor, Rich, Smith & Barnes, CPAs (BRS&B), for several years. McClain Plastics was started by Evers McClain, who owns 51 percent of the company’s stock. The balance is owned by about 20 stockholders, who are

> The Maguire Pharmaceutical Company, a drug manufacturer, has the following internal controls for billing and recording accounts receivable: 1. An incoming customer’s purchase order is received in the order department by a clerk who prepares a prenumbered

> Auditors develop overall audit plans to ensure that they obtain sufficient appropriate audit evidence. The timing and extent of audit procedures auditors use is a matter of professional judgment, which depends upon a number of factors. Decisions about th

> The following are examples of audit procedures: 1. Watch employees count inventory to determine whether company procedures are being followed. 2. Count a sample of inventory items and record the amount in the audit files. 3. Calculate the ratio of sales

> Most grocery stores use bar code scanning technologies that interface with cash registers used to process customer purchases. Cashiers use the scanners to read bar code labels attached to each product, which the system then uses to obtain unit prices, ca

> Discuss changes in accounting and business operations over the last decade that have increased the need for independent audits.

> The following are audit procedures from different transaction cycles: 1. Examine sales invoices for evidence of internal verification of prices, quantities, and extensions. 2. Select items from the client’s perpetual inventory records and examine the ite

> The following are audit procedures from different transaction cycles: 1. Trace a sample of shipping documents to entry in the sales journal. 2. Examine a sample of warehouse removal slips for signature of authorized official. 3. Examine contract terms fo

> Internal controls 1 through 5 were tested in prior audits. Evaluate each internal control independently and determine which controls must be tested in the current year’s audit of the December 31, 2019, financial statements. Be sure to explain why testing

> This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the ref

> The SEC issues Accounting and Auditing Enforcement Releases (AAERs) summarizing SEC actions concerning civil lawsuits brought by the SEC in federal court and related settlements from administrative proceedings. Visit the SEC’s website (www.sec.gov) and l

> Following are 10 key internal controls in the payroll cycle for Gilman Stores, Inc. Key Controls 1. To input hours workedpayroll accounting personnel input the employee’s identification number. The system does not allow input of hours worked for invalid

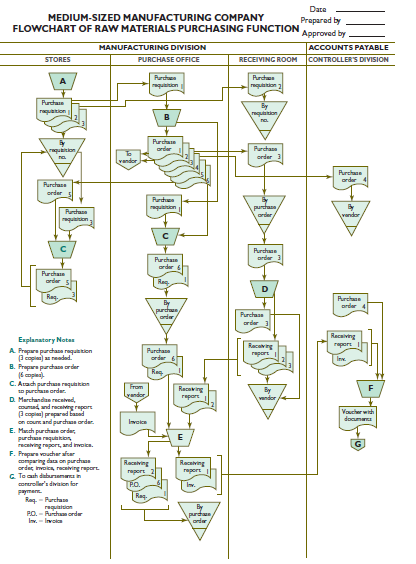

> Anthony Liu, CPA, prepared the flowchart on the next page that portrays the raw materials purchasing function of one of Anthony’s clients, Medium-Sized Manufacturing Company, from the preparation of initial documents through the vouching of invoices for

> Mark Hopper is planning the audit of the investments account for audit client Garden Supply Co. (GSC). GSC invests excess cash at the end of the summer sales season through an investment manager who invests in equity and debt securities for GSCâ

> This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the ref

> What is the role of the Public Company Accounting Oversight Board (PCAOB)? How does the PCAOB provide oversight of audit firms?

> The following audit procedures are included in the audit program because of heightened risks of material misstatements due to fraud. 1. Use audit software to search purchase transactions to identify any with nonstandard vendor numbers or with vendor name

> Your new audit client, Hardwood Lumber Company, has a computerized accounting system for all financial statement cycles. During planning, you visited with the information systems vice president and learned that personnel in information systems are assign

> This problem requires you to access PCAOB Auditing Standards (pcaobus.org) to answer each of the following questions. You can access those standards by viewing content found under the link “Standards.” Review PCAOB auditing standards related to the audit

> The following are misstatements that can occur in the sales and collection cycle: 1. A customer order was filled and shipped to a former customer, which had already filed for bankruptcy. 2. For a sale, a data entry operator erroneously failed to enter th

> The division of the following duties is meant to provide the best possible controls for the Meridian Paint Company, a small wholesale store: †1. Approve credit for customers included in the customer credit master file. †2. Input shipping and billing info

> The following are misstatements that have occurred in Fresh Foods Grocery Store, a retail and wholesale grocery company: 1. On the last day of the year, a truckload of beef was set aside for shipment but was not shipped. Because it was still on hand, the

> The following are internal controls related to various cycles. 1. Checks are signed by the company president, who compares the checks with the underlying supporting documents. 2. Sales invoices are matched with shipping documents by the computer system a

> Why is it important to distinguish the auditor’s assessment of the risk of material misstatement due to fraud from the assessment of the risk of material misstatement due to error?

> Indicate the four phases of the audit process. In which phase does the auditor perform tests of controls?

> What are the benefits derived from planning audits?

> Identify two examples of acts or behavior by CPAs that would be considered acts discreditable to the profession.

> An audit client is creating a Web-based sales ordering system for customers to purchase products using personal credit cards for payment. Identify three risks related to an online sales system that management should consider. For each risk, identify an i

> Assume that Xinran Wang, CPA, is using 5 percent of net income before taxes, current assets, or current liabilities as her major guideline for evaluating materiality. What qualitative factors should she also consider in deciding whether misstatements may

> Compare the risks associated with network systems and database systems to those associated with centralized IT functions.

> Identify the traditionally segregated duties in IT systems.

> Describe which two factors of the audit risk model relate to the risk of material misstatement at the assertion level.

> Explain how control risk assessment differs for an integrated audit versus a financial statement-only audit.

> What do auditing standards require the auditor to consider when assessing the risk of material misstatements in revenue?

> What is the primary focus of the monitoring component of internal control?

> What three auditor actions are required to address the potential for management override of controls?

> Describe the types of overall responses by auditors to address fraud risk.

> What is meant by the term quality control as it relates to a CPA firm?

> In addition to inquiring of individuals among management who are involved in financial reporting positions, such as the CFO and controller, which additional individuals should you consider making inquiries of as part of your risk assessment procedures? B

> Assume that you are concerned that your client has recorded revenues that did not occur. What audit objective would you assess as having a high risk of material misstatement?

> Identify the management assertion and general balance-related audit objective for the specific balance-related audit objective: Read the fixed asset footnote disclosure to determine that the types of fixed assets, depreciation methods, and useful lives a

> Describe the types of information that should be included in the auditor’s working papers as evidence of the auditor’s fraud assessment procedures.

> The following is an example of a CPA firm’s quality control procedure requirement: “Any person being considered for employment by the firm must have completed a basic auditing course and have been interviewed and approved by an audit partner of the firm

> Explain why liquidity activity ratios ratios are useful to auditors.

> Describe examples of characteristics of transactions and balances that might cause an auditor to determine that a risk of material misstatement is a significant risk.

> Auditing standards require that the engagement team members engage in discussion about the susceptibility of the financial statements to the risk of fraud. How does this discussion relate to the required discussion about the risk of material misstatement

> Auditing standards require that the engagement team members engage in discussion about the risk of material misstatement. Describe the nature of this required discussion and who should be involved.

> Why is it important for the auditor to consider the risk of material misstatement at the overall financial statement level?

> This problem requires the use of ACL software, which can be accessed through the textbook website. Information about downloading and using ACL and the commands used in this problem can also be found on the textbook website. You should read all of the ref

> For how long does the Sarbanes–Oxley Act require auditors of public companies to retain audit documentation?

> What constitutes a significant risk?

> What types of inquiries should the auditor make when considering the risk of material misstatement due to fraud?

> How should the auditor consider risks related to revenue recognition when assessing the risk of material misstatement due to fraud?

> What are the five elements of an effective professional judgment process?

> What are the six elements of professional skepticism? Describe two of those six elements.

> What is the auditor’s responsibility when noncompliance with laws or regulations is identified or suspected?

> In recent years, globalization of business and factors such as technological disruption, tax reform, trade policies, and changing demographics in the workforce cause uncertainty and volatility in stock and bond markets. Why might it be important for you

> What four circumstances are required for a standard unmodified opinion audit report to be issued?

> Who is considered the client when auditing public companies?

> Describe some of the reasons why there have been calls for mandatory rotation of audit firms. How could an investor of a public company determine how long an audit firm has served as that company’s auditor?

> Describe what is meant by an audit procedure. Why is it important for audit procedures to be carefully worded?

> The Responsibilities principle requires that auditors be responsible for having appropriate competence and capabilities to perform the audit. What are the various ways in which auditors can fulfill this principle?

> Provide two examples of when an auditor might set a lower level of performance materiality for a particular class of transactions, account balance, or disclosure.