Question: Today is September 16, Year 2. You,

Today is September 16, Year 2. You, CPA, work for Garcia & Garcia LLP, a medium-sized firm located in Montreal. Jules Garcia calls you into his office. "CPA, I have a very special engagement for you. A friend of mine, Louise Martin, is starting a not-for-profit organization named MMB. MMB is going to be Quebec's first breast milk bank. Louise was unable to breastfeed her newborn and obtained donated breast milk for the first year of her daughter's life. She was lucky enough to live in British Columbia at the time, and had access to donated breast milk. She now lives in Montreal and hopes to give babies here the same access to breast milk that she and her daughter had." Jules provides you with information on breast milk banking that he received from Louise (Exhibit III).

"The Breast Milk Agency (the Agency) is a government body that regulates breast milk banks. The role of the Agency is to eliminate the risk that a disease or contaminant is transferred in milk by ensuring controls are established to preclude contamination."

Jules continues, "To receive grants, MMB is required to prepare financial statements that follow Canadian Accounting Standards for Not-for-Profit Organizations. Louise has limited accounting knowledge and is feeling overwhelmed with how to account for all the different types of donations. Please help her select appropriate accounting policies, where necessary, and draw her attention to accounting issues she might encounter."

Jules hands you notes from his meeting with Louise (Exhibit IV). "Please help her with any other issues that you identify."

Exhibit III:

Exhibit IV:

Transcribed Image Text:

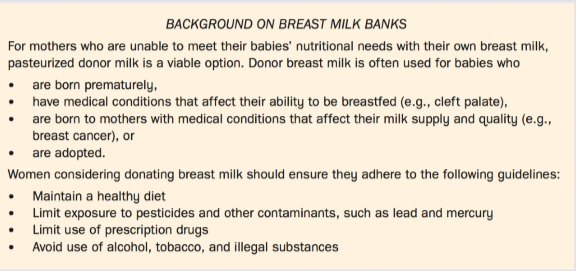

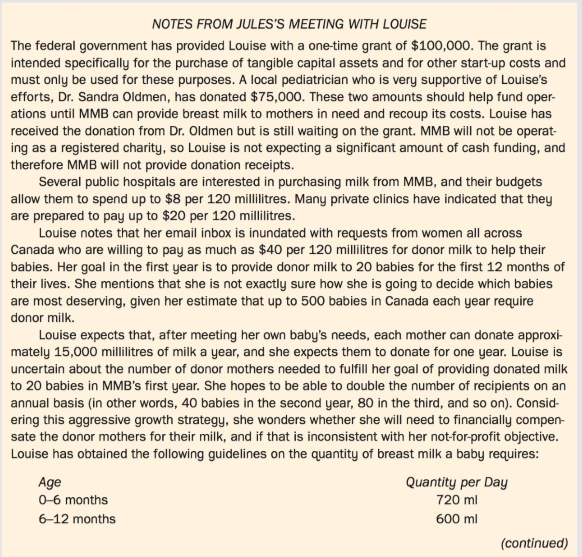

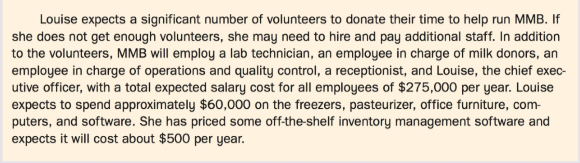

BACKGROUND ON BREAST MILK BANKS For mothers who are unable to meet their babies' nutritional needs with their own breast milk, pasteurized donor milk is a viable option. Donor breast milk is often used for babies who are born prematurely, have medical conditions that affect their ability to be breastfed (e.g., cleft palate), are born to mothers with medical conditions that affect their milk supply and quality (e.g., breast cancer), or • are adopted. Women considering donating breast milk should ensure they adhere to the following guidelines: Maintain a healthy diet Limit exposure to pesticides and other contaminants, such as lead and mercury Limit use of prescription drugs Avoid use of alcohol, tobacco, and illegal substances NOTES FROM JULES'S MEETING WITH LOUISE The federal government has provided Louise with a one-time grant of $100,000. The grant is intended specifically for the purchase of tangible capital assets and for other start-up costs and must only be used for these purposes. A local pediatrician who is very supportive of Louise's efforts, Dr. Sandra Oldmen, has donated $75,000. These two amounts should help fund oper- ations until MMB can provide breast milk to mothers in need and recoup its costs. Louise has received the donation from Dr. Oldmen but is still waiting on the grant. MMB will not be operat- ing as a registered charity, so Louise is not expecting a significant amount of cash funding, and therefore MMB will not provide donation receipts. Several public hospitals are interested in purchasing milk from MMB, and their budgets allow them to spend up to $8 per 120 millilitres. Many private clinics have indicated that they are prepared to pay up to $20 per 120 millilitres. Louise notes that her email inbox is inundated with requests from women all across Canada who are willing to pay as much as $40 per 120 millilitres for donor milk to help their babies. Her goal in the first year is to provide donor milk to 20 babies for the first 12 months of their lives. She mentions that she is not exactly sure how she is going to decide which babies are most deserving, given her estimate that up to 500 babies in Canada each year require donor milk. Louise expects that, after meeting her own baby's needs, each mother can donate approxi- mately 15,000 millilitres of milk a year, and she expects them to donate for one year. Louise is uncertain about the number of donor mothers needed to fulfill her goal of providing donated milk to 20 babies in MMB's first year. She hopes to be able to double the number of recipients on an annual basis (in other words, 40 babies in the second year, 80 in the third, and so on). Consid- ering this aggressive growth strategy, she wonders whether she will need to financially compen- sate the donor mothers for their milk, and if that is inconsistent with her not-for-profit objective. Louise has obtained the following guidelines on the quantity of breast milk a baby requires: Age Quantity per Day 720 ml 0-6 months 6-12 months 600 ml (continued) Louise expects a significant number of volunteers to donate their time to help run MMB. If she does not get enough volunteers, she may need to hire and pay additional staff. In addition to the volunteers, MMB will employ a lab technician, an employee in charge of milk donors, an employee in charge of operations and quality control, a receptionist, and Louise, the chief exec- utive officer, with a total expected salary cost for all employees of $275,000 per year. Louise expects to spend approximately $60,000 on the freezers, pasteurizer, office furniture, com- puters, and software. She has priced some off-the-shelf inventory management software and expects it will cost about $500 per year.

> How would the consolidation of a parent-founded subsidiary differ from the consolidation of a purchased subsidiary?

> Don Ltd. purchased 80% of the outstanding shares of Gunn Ltd. Before the purchase, Gunn had a deferred charge of $10.5 million on its balance sheet. This item consisted of organization costs that were being amortized over a 20-year period. What amount sh

> In whose accounting records are the consolidation elimination entries recorded? Explain.

> How is the net income earned by a subsidiary in the year of acquisition incorporated in the consolidated income statement?

> Explain whether the historical cost principle is applied when accounting for negative goodwill.

> What is negative goodwill, and how is it accounted for?

> Outline the Handbook's requirements for NFPOs with regard to accounting for the capital assets of NFPOs.

> Is a negative acquisition differential the same as negative goodwill? Explain.

> What is an acquisition differential, and where does it appear on the consolidated balance sheet?

> What part do irrevocable agreements, convertible securities, and warrants play in determining whether control exists? Explain.

> What criteria must be met for a subsidiary to be consolidated? Explain.

> If one company issued shares as payment for the net assets of another company, it would probably insist that the other company be wound up after the sale. Explain why this condition would be part of the purchase agreement.

> Briefly describe the accounting involved with the new-entity method.

> Outline the accounting involved with the acquisition method for a 100%-owned subsidiary.

> Explain how an acquirer is determined in a business combination for a 100%-owned subsidiary.

> Can a statutory amalgamation be considered a form of business combination? Explain.

> What are protective rights, and how do they affect the decision of whether one entity has control over another entity?

> It is common for an NFPO to receive donated supplies, equipment, and services. Do current accounting standards require the recording of donations of this kind? Explain.

> What are separate financial statements, and when can they be presented to external users in accordance with IFRS?

> Does the historical cost principle or fair value reporting take precedence when preparing consolidated financial statements at the date of acquisition under the acquisition method? Explain.

> When must an intangible asset be shown separately from goodwill? What are the criteria for reporting these intangible assets separately from goodwill?

> How is goodwill determined at the date of acquisition? Describe the nature of goodwill.

> What are some reasons for the acquisition cost being in excess of the carrying amount of the acquiree's assets and liabilities? What does this say about the accuracy of the values used in the financial statements of the acquiree?

> What key element must be present in a business combination?

> Able Company holds a 40% interest in Baker Corp. During the year, Able sold a portion of this investment. How should this investment be reported after the sale?

> Ashton Inc. acquired a 40% interest in Villa Corp. for $200,000. In the first year after acquisition, Villa reported a loss of $700,000. Using the equity method, how should Ashton account for this loss assuming (a) Ashton has guaranteed the liabilities o

> Briefly outline how NFPOs differ from profit-oriented organizations.

> The following balance sheets have been prepared as at December 31, Year 6, for Kay Corp. and Adams Ventures: Additional Information • Kay acquired its 40% interest in Adams for $374,000 in Year 2, when Adams's retained earnings amount

> Fairchild Centre is an NFPO funded by government grants and private donations. It was established on January 1, Year 5, to provide counselling services and a drop-in center for single parents. On January 1, Year 5, the center leased an old warehouse in t

> Regina Communications Ltd. develops and manufactures equipment for technology and communications enterprises. Since its incorporation, it has grown steadily through internal expansion. In the middle of Year 14, Arthur Lajord, the sole owner of Regina, me

> When Conoco Inc. of Houston, Texas announced the CAD$7 billion acquisition of Gulf Canada Resources Limited of Calgary, Alberta, a large segment of the press release was devoted to outlining all of the expected benefits to be received from the assets acq

> Manitoba Peat Moss (MPM) was the first Canadian company to provide a reliable supply of high-quality peat moss to be used for greenhouse operations. Owned by Paul Parker, the company's founder and president, MPM began operations approximately 30 years ag

> The directors of Atlas Inc. and Beta Corp. have reached an agreement in principle to merge the two companies and create a new company called AB Ltd. The basics of the agreement confirmed so far are outlined below: • The new company will purchase all of

> On December 30, Year 7, Pepper Company agreed to form a business combination with Salt Limited. Pepper issued 4,640 of its common shares for all (5,800) of the outstanding common shares of Salt. This transaction increased the number of the outstanding Pe

> You are examining the consolidated financial statements of a European company, which have been prepared in accordance with IFRS. You determine that property, plant, and equipment is revalued each year to its current fair value, income and equity are adju

> In this era of rapidly changing technology, research and development (R&D) expenditures represent one of the most important factors in the future success of many companies. Organizations that spend too little on R&D risk being left behind by the competit

> An investor uses the equity method to report its investment in an investee. During the current year, the investee reports other comprehensive income on its statement of comprehensive income. How should this item be reflected in the investor's financial s

> Michael Metals Limited (MML) has been a private company since it was incorporated under federal legislation over 40 years ago. At the present time (September, Year 45), ownership is divided among four cousins, each of whom holds 25% of the 100 outstandin

> Canadian Computer Systems Limited (CCS) is a public company engaged in the development of computer software and the manufacturing of computer hardware. CCS is listed on a Canadian stock exchange and has a 40% non-controlling interest in Sandra Investment

> It is January 20, Year 13. Mr. Neely, a partner in your office, wants to see you, CPA, about Bruin Car Parts Inc. (BCP), a client requiring assistance. BCP prepares its financial statements in accordance with ASPE. Richard (Rick) Bergeron, Lyle Chara, an

> Floyd's Specialty Foods Inc. (FSFI) operates over 60 shops throughout Ontario. The company was founded by George Floyd when he opened a single shop in the city of Cornwall. This store sold prepared dinners and directed its products at customers who were

> Hil Company purchased 10,000 common shares (10%) of Ton Inc. on January 1, Year 4, for $345,000, when Ton's shareholders' equity was $2,600,000, and it classified the investment as a FVTPL security. On January 1, Year 5, Hil acquired an additional30,000

> Goal Products Limited (GPL) is the official manufacturer and distributor of soccer balls for the North American League Soccer (NALS), a professional soccer association. GPL is a private company. It has always prepared its financial statements in accordan

> Roman Systems Inc. (RSI) is a Canadian private company. It was incorporated in Year 1 by its sole common shareholder, Marge Roman. RSI manufactures, installs, and provides product support for its line of surveillance cameras. Marge started the company wi

> John McCurdy has recently joined a consultant group that provides investment advice to the managers of a special investment fund. This investment fund was created by a group of NFPOs, all of which have endowment funds, and rather than investing their res

> The provincial government (50%) and three private companies (16.67% each) own Access Records Limited (ARL), which commenced operations on April 1, Year 1. The provincial government currently maintains, on a manual basis, all descriptive information on la

> The Sassawinni. First Nation is located adjacent to a town in northern Saskatchewan. The Nation is under the jurisdiction of the federal government’s Aboriginal Affairs and Northern Development Canada, and for years has received substantial funding from

> Because of the acquisition of additional investee shares, an investor may need to change from the fair value method for a FVTPL investment to the equity method for a significant influence investment. What procedures are applied to effect this accounting

> When and why would an NFPO use replacement cost rather than net realizable value to determine whether inventory should be written down?

> In the fall of Year 5, eight wealthy business people from the same ethnic background formed a committee (CKER committee) to obtain a radio license from the Canadian Radio-television and Telecommunications Commission (CRTC). Their goal is to start a non-p

> Confidence Private is a high school in the historic city of Jeanville. It engages students in a dynamic learning environment and inspires them to become intellectually vibrant, compassionate, and responsible citizens. The private school has been run as a

> You have just completed an interview with the newly formed audit committee of the Andrews Street Youth Centre (ASYC). This organization was created to keep neighborhood youth off the streets by providing recreational facilities where they can meet, exerc

> Beaucoup Hospital is located near Montreal. A religious organization created the not-for-profit hospital more than 70 years ago to meet the needs of area residents who could not otherwise afford adequate health care. Although the hospital is open to the

> Maple Limited (Maple) was incorporated on January 2, Year 1, and commenced active operations immediately in Greece. Common shares were issued on the date of incorporation for 100,000 euros (€), and no more common shares have been issued

> Athena Ltd. is a subsidiary located in Greece. It uses the euro for internal reporting purposes. At December 31, Year 11, the company's inventory on hand had a cost of €20,000 and a net realizable value of €21,000. The i

> On January 1, Year 4, P Company (a Canadian company) purchased 90% of S Company (located in a foreign country) at a cost of 15,580 foreign currency units (FC). The carrying amounts of S Company's net assets were equal to fair values on this date except f

> EVA Company was incorporated on January 2, Year 5, and commenced active operations immediately. Ordinary shares were issued on the date of incorporation and no new ordinary shares have been issued since then. On December 31, Year 9, PAL Company purchased

> Refer to Problem 11-3. All of the facts and data given in the problem are the same. Your answer to Problem 11-3 will be incorporated in the answer to this problem. Kelly Corporation's comparative balance sheets and Year 2 income statement are as follows:

> The Ralston Company owns 35% of the outstanding voting shares of Purina Inc. Under what circumstances would Ralston determine that it is inappropriate to report this investment using the equity method?

> On December 31, Year 1, Kelly Corporation of Toronto paid 13.7 million Libyan dinars (LD) for 100% of the outstanding common shares of Arkenu Company of Libya. On this date, the fair values of Arkenu's identifiable assets and liabilities were equal to th

> Refer to Problem 11-1. All of the facts and data given in the problem are the same except that PMI only purchased 40% of the outstanding ordinary shares of Sandora for US$6,400,000. Additional Information • PMI's 40% in Sandora gave it

> On January 1, Year 4, Par Company purchased all the outstanding common shares of Bayshore Company, located in California, for US$260,000. The carrying amount of Bayshore's shareholders' equity on January 1, Year 4, was US$202,000. The fair value of Baysh

> White Company was incorporated on January 2, Year 1, and commenced active operations immediately. Common shares were issued on the date of incorporation and no new common shares have been issued since then. On December 31, Year 5, Black Company purchased

> SPEC Co. is a Canadian investment company. It acquires real estate properties in foreign countries for speculative purposes. On January 1, Year 5, SPEC incorporated a wholly owned subsidiary, CHIN Limited. CIDN immediately purchased a property in Shangha

> The financial statements of Malkin Inc., of Russia, as at December 31, Year 11, follow: Additional Information • On January 1, Year 11, Crichton Corporation of Toronto acquired 40% of Malkin's common shares for RR800,000. â

> In Year 1, Victoria Textiles Limited decided that its Asian operations had expanded such that an Asian office should be established. The office would be involved in selling Victoria's current product lines; it was also expected to establish supplier cont

> On December 31, Year 1, Precision Manufacturing Inc. (PMI) of Edmonton purchased 100% of the outstanding ordinary shares of Sandora Corp. of Flint, Michigan. Sandora's comparative statement of financial position and Year 2 income statement are as follows

> EnDur Corp (EDC) is a Canadian company that exports computer software. On February l, Year 2, EDC contracted to sell software to a customer in Denmark at a selling price of 600,000 Danish krona (DK) with payment due 60 days after installation was complet

> On August 1, Year 3, Carleton Ltd. ordered machinery from a supplier in Hong Kong for HK$500,000. The machinery was delivered on October 1, Year 3, with terms requiring payment in full by December 31, Year 3. On August 2, Year 3, Carleton entered a forwa

> The equity method records dividends as a reduction in the investment account. Explain why.

> Hamilton Importing Corp. (HIC) imports goods from countries around the world for sale in Canada. On December 1, Year 3, HIC purchased 11,300 watches from a foreign wholesaler for DM613,000 when the spot rate was DM1 = $0.754. The invoice called for payme

> On October 1, Year 6, Versatile Company contracted to sell merchandise to a customer in Switzerland at a selling price of SF400,000. The contract called for the merchandise to be delivered to the customer on January 31, Year 7, with payment due on delive

> On January 1, Year 5, Ornate Company Ltd. purchased US$2,200,000 of the bonds of the Gem Corporation. The bonds were trading at par on this date, pay interest at 12% each December 31, and mature on December 31, Year 7. The following Canadian exchange rat

> Lamont Company is a Canadian company that produces electronic switches for the telecommunications industry. Lamont regularly imports component parts from Sousa Ltd., a supplier located in Mexico, and makes payments in Mexican pesos (MP). Based on past ex

> Moose Utilities Ltd. (MUL) borrowed $40,000,000 in U.S. funds on January 1, Year 1, at an annual interest rate of 12%. The loan is due on December 31, Year 4, and interest is paid annually on December 31. The Canadian exchange rates for U.S. dollars over

> Assume that all of the facts in Problem 1 remain unchanged except that MEl uses hedge accounting. Also, assume that the forward element and spot elements on the forward contract are accounted for separately. Required: (a) Prepare the journal entries fo

> As a result of its export sales to customers in Switzerland, the Lenox Company has had Swiss-franc-denominated revenues over the past number of years. In order to gain protection from future exchange rate fluctuations, the company decides to borrow its c

> Hull Manufacturing Corp. (HMC), a Canadian company, manufactures instruments used to measure the moisture content of barley and wheat. The company sells primarily to the domestic market, but in Year 3, it developed a small market in Argentina. In Year 4,

> On June 1, Year 3, Forever Young Corp. (FYC) ordered merchandise from a supplier in Turkey for Turkish lira (TL) 217,000. The goods were delivered on September 30, with terms requiring cash on delivery. On June 2, Year 3, FYC entered a forward contract a

> On May 1, Year 1, JDH orders equipment from a supplier in Germany for €100,000 with delivery scheduled for October 1, Year 1. Payment is due on December 31, Year 1. On May 2, Year 1 JDH enters into an 8-month forward contract with its ba

> What criteria would be used to determine whether the equity method should be used to account for a particular investment?

> Gemella Ltd. manufactures construction equipment for sale throughout eastern Canada and northeastern United States. Its year-end is June 30. The following foreign currency transactions occurred during the Year 11 calendar year: 1. On January 10, Gemella

> Manitoba Exporters Inc. (MEl) sells Inuit carvings to countries throughout the world. On December 1, Year 5, MEl sold 10,000 carvings to a wholesaler in a foreign country at a total cost of 600,000 foreign currency units (FCs) when the spot rate was FC1

> The following are the December 31, Year 9, balance sheets of three related companies: Additional Information • On January 1, Year 5, Pro purchased 40% of Forma for $116,000. On that date, Forma's shareholders' equity was as follows:

> Access the 2014 consolidated financial statements for Rogers Communications Inc. by going to the investor relations section of the company's website. Answer the questions below. For each question, indicate where in the financial statements you found the

> The following information has been assembled about Casbar Corp. as at December 31, Year 5 (amounts are in thousands): Required: Determine which operating segments require separate disclosures. Operating Segment Revenues Profit Assets $12,000 9,600

> On January 1, Year 6, HD Ltd., a building supply company, JC Ltd., a construction company, and Mr. Saeid, a private investor, signed an agreement to carry out a joint operation under the following terms and conditions: • JC would buy an

> The statements of financial position of Hui Inc. and Kozikowski Ltd. on December 31, Year 11, were as follows: Kozikowski's manufacturing facility is old and very costly to operate. For the year ended December 31, Year 11, the company lost money for th

> Assume that all of the facts in Problem 3 remain unchanged except that Green paid $211,800 for 60% of the voting shares of Mansford. Required: (a) Prepare a consolidated balance sheet at January 1, Year 5. (b) Calculate goodwill and non-controlling int

> On January 1, Year 5, Green Inc. purchased 100% of the common shares of Mansford Corp. for $353,000. Green's balance sheet data on this date just prior to this acquisition were as follows: The balance sheet and other related data for Mansford are as fo

> On January 1, Year 5, AB Company (AB) purchased 80% of the outstanding common shares of Dandy Limited (Dandy) for $8,000. On that date, Dandy's shareholders' equity consisted of common shares of $1,000 and retained earnings of $6,000. In negotiating the

> Distinguish between the financial reporting for FVTPL investments and that for investments in associates.

> On January 1, Year 5, Wellington Inc. owned 90% of the outstanding common shares of Sussex Corp. Wellington accounts for its investment using the equity method. The balance in the investment account on January 1, Year 5, amounted to $244,800. The unamort

> Jager Ltd., a joint venture, was formed on January 1, Year 3. Clifford Corp., one of the three founding venturers, invested equipment for a 40% interest in the joint venture. The other two venturers invested land and cash for their 60% equity. All of the

> The following are the Year 9 income statements of Poker Inc. and Joker Company: Additional Information • Poker acquired a 60% interest in the common shares of Joker on January 1, Year 4, at a cost of $420,000 and uses the cost method

> On January 1, Year 1, Amco Ltd. and New star Inc. formed Bearcat Resources, a joint venture. New star contributed miscellaneous assets with a fair value of $844,000 for a 65% interest in the venture. Amco contributed plant and equipment with a carrying a

> Albert Company has an investment in the voting shares of Prince Ltd. On December 31, Year 5, Prince reported a net income of $860,000 and declared dividends of $200,000. During Year 5, Albert had sales to Prince of $915,000, and Prince had sales to Alber

> The following are the Year 9 income statements of Kent Corp. and Laurier Enterprises. Additional Information $1,380,000 88,000 118,000 1,586,000 605,000 318,000 13q,ooo 168,000 1,230,000 $ 356,000 • Kent acquired its 40% interest in

> Pharma Company (Pharma) is a pharmaceutical company operating in Winnipeg. It is developing a new drug for treating multiple sclerosis (MS). On January 1, Year 3, Benefit Ltd. (Benefit) signed an agreement to guarantee the debt of Pharma and guarantee a

> Parent Co. owns 9,500 shares of Sub Co. and accounts for its investment by the equity method. On December 31, Year 5, the shareholders' equity of Sub was as follows: On January 1, Year 6, Parent sold 1,900 shares from its holdings in Sub for $66,500. O