Question: We projected financial statements for Walmart

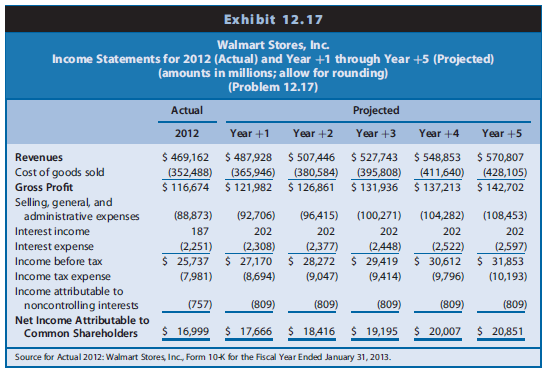

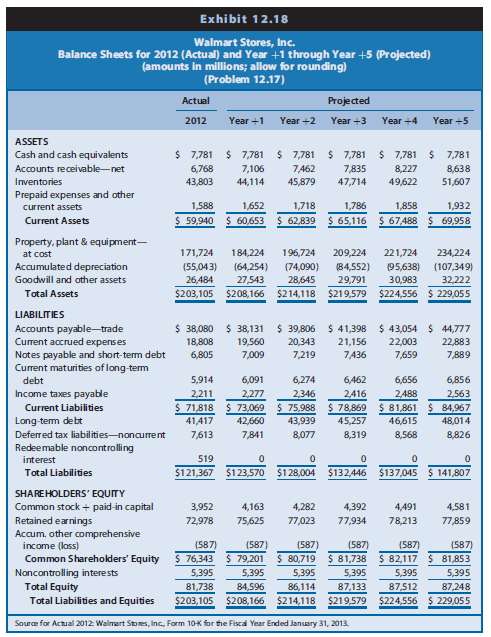

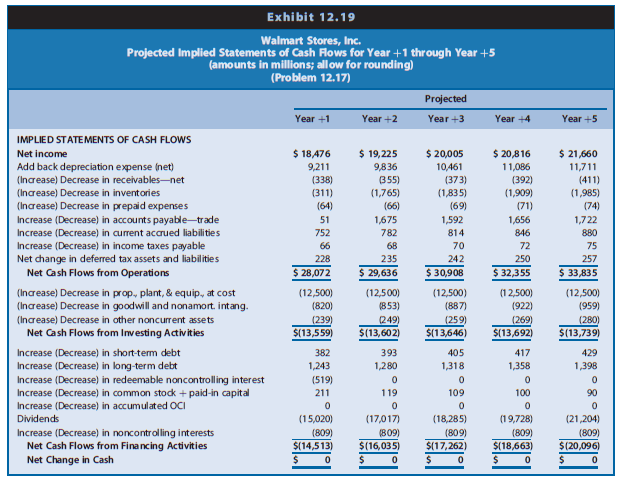

We projected financial statements for Walmart Stores for Years þ1 through +5. The data in Chapter 12 Exhibits 12.17–12.19 include the actual amounts for 2012 and the projected amounts for Year +1 to Year +5 for the income statements, balance sheets, and statements of cash flows for Walmart (in millions).

The market equity beta for Walmart at the end of 2012 was 1.00. Assume that the risk-free interest rate was 3.0% and the market risk premium was 6.0%. Walmart had 3,314 million shares outstanding at the end of 2012, and the share price was $69.09.

REQUIRED

Part I—Computing Walmart’s Value-to-Book Ratio Using the Value-to-Book Valuation Approach

a. Use the CAPM to compute the required rate of return on common equity capital for

Walmart.

b. Using the projected financial statements in Chapter 12 Exhibits 12.17–12.19, derive the projected residual ROCE (return on common shareholders’ equity) for Walmart for Years +1 through +5.

c. Assume that the steady-state, long-run growth rate will be 3% in Year +6 and beyond. Project that the Year +5 income statement and balance sheet amounts will grow by 3% in Year +6; then derive the projected residual ROCE for Year þ6 for Walmart.

d. Using the required rate of return on common equity from Requirement a as a discount rate, compute the sum of the present value of residual ROCE for Walmart for Years þ1 through +5.

e. Using the required rate of return on common equity from Requirement a as a discount rate and the long-run growth rate from Requirement c, compute the continuing value of Walmart as of the start of Year +6 based on Walmart’s continuing residual ROCE in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1.

f. Compute Walmart’s value-to-book ratio as of the end of 2012 with the following three steps:

(1) Compute the total sum of the present value of all future residual ROCE (from Requirements d and e).

(2) To the total from Requirement f (1), add 1 (representing the book value of equity as of the beginning of the valuation as of the end of 2012).

(3) Adjust the total sum from Requirement f (2) using the midyear discounting adjustment factor.

g. Compute Walmart’s market-to-book ratio as of the end of 2012. Compare the value-to-book ratio to the market-to-book ratio. What investment decision does the comparison suggest? What does the comparison suggest regarding the pricing of Walmart shares in the market: underpriced, overpriced, or fairly priced?

h. Use the value-to-book ratio to project Walmart’s share value.

i. If you computed Walmart’s common equity share value using the dividends valuation approach in Problem 11.14 in Chapter 11, and/or the free cash flows to common equity valuation approach in Problem 12.17 in Chapter 12, and/or the residual income valuation approach in Problem 13.20 in Chapter 13, compare the value estimate you obtained in those problems with the estimate you obtained in this case. You should obtain the same value estimates under all four approaches. If you have not yet worked those problems, you would benefit from doing so now.

Part II—Analyzing Walmart’s Share Price Using the Value-Earnings Ratio, Price-Earnings Ratio, Price Differentials, and Reverse Engineering

j. Use the forecast data for Year +1 to project Year +1 earnings per share. To do so, divide Walmart’s projected comprehensive income available for common shareholders in Year +1 by the number of common shares outstanding at the end of 2012. Using this Year +1 earnings-per-share forecast and the share value computed in Requirement h, compute Walmart’s value-earnings ratio.

k. Using the Year +1 earnings-per-share forecast from Requirement j and using the share price of $69.09 at the end of 2012, compute Walmart’s price-earnings ratio. Compare Walmart’s value-earnings ratio with its price-earnings ratio. What does the comparison suggest regarding the pricing of Walmart shares in the market: underpriced, overpriced, or fairly priced? What investment decision does the comparison suggest? Does this comparison lead to the same conclusions you reached when comparing value-to-book ratios with market-to-book ratios in Requirement g?

l. Note: For this part only, assume Walmart’s long-run growth beginning in Year +6 will be 1% rather than 3%. With a 1% growth rate, Year +6 comprehensive income will be $21,059 million. Compute Walmart’s price differential at the end of 2012. Compute Walmart’s price differential as a percentage of Walmart’s risk-neutral value. What dollar amount and what percentage amount has the market discounted Walmart shares for risk?

m. Reverse engineer Walmart’s share price at the end of 2012 to solve for the implied expected rate of return. First, assume that value equals price and that the earnings and 3% long-run growth forecasts in Year þ6 and beyond are reliable proxies for the market’s expectations for Walmart. Then solve for the implied expected rate of return (the discount rate) the market has impounded in Walmart’s share price.

(Hint: Begin with the forecast and valuation spreadsheet you developed to value Walmart shares.

Vary the discount rate until you solve for the discount rate that makes your value estimate exactly equal the end-of-2012 market price of $69.09 per share.)

n. Reverse engineer Walmart’s share price at the end of 2012 to solve for the implied expected long-run growth. First, assume that value equals price and that the earnings forecasts through Year +5 are reliable proxies for the market’s expectations for Walmart. Also assume that the discount rate implied by the CAPM (computed in Requirement a) is a reliable proxy for the market’s expected rate of return. Then solve for the implied expected long-run growth rate the market has impounded in Walmart’s share price.

(Hint: Begin with the forecast and valuation spreadsheet you developed to value Walmart shares and use the CAPM discount rate. Set the long-run growth parameter initially to zero. Increase the long-run growth rate until you solve for the growth rate that makes your value estimate exactly equal the end-of-2012 market price of $69.09 per share.)

Transcribed Image Text:

Exhibit 12.17 Walmart Stores, Inc. Income Statements for 2012 (Actual) and Year +1 through Year +5 (Projected) (amounts in millions; allow for rounding) (Problem 12.17) Actual Projected 2012 Year +1 Year +2 Year +3 Year +4 Year +5 $ 469,162 $ 487,928 $ 527,743 $ 570,807 $ 507,446 (380,584) $ 126,861 Revenues $ 548,853 Cost of goods sold (352,488) (365,946) (395,808) $ 131,936 (411,640) (428,105) $ 137,213 $ 142,702 Gross Profit $ 116,674 $ 121,982 Selling, general, and administrative expenses (88,873) (92,706) (96,415) (100,271) (104,282) (108,453) Interest income 187 202 202 202 202 202 Interest expense (2,522) $ 30,612 (2,251) (2,308) $ 27,170 (2,377) $ 28,272 (9,047) (2,448) (2,597) $ 31,853 (10,193) Income before tax $ 25,737 $ 29,419 Income tax expense (7,981) (8,694) (9,414) (9,796) Income attributable to noncontrolling interests (757) (809) (809) (809) (809) (809) Net Income Attributable to Common Shareholders $ 16,999 $ 17,666 $ 18,416 $ 19,195 $ 20,007 $ 20,851 Source for Actual 2012: Walmart Stores, Inc, Form 10K for the Fiscal Year Ended January 31, 2013. Exhibit 12.18 Walmart Stores, Inc. Balance Sheets for 2012 (Actual) and Year +1 through Year +5 (Projected) (amounts in millions; allow for rounding) (Problem 12.17) Actual Projected 2012 Year +1 Year +2 Year +3 Year +4 Year +5 ASSETS $ 7,781 $ 7,781 $ 7,781 $ 7,781 $ 7,781 $ 7,781 7462 Cash and cash equivalents Accounts receivable-net 6,768 7,106 7,835 8,227 8,638 Inventories 43,803 44,114 45,879 47,714 49,622 51,607 Prepaid expenses and other current assets 1,588 1,652 1,718 1,786 1,858 1,932 current assets $ 59,940 $ 60,653 $ 62,839 $ 65,116 $ 67,488 $ 69,958 Property, plant & equipment- at cost 171,724 184,224 196,724 209,224 221,724 234,224 (84,552) Accumulated depreciation Goodwill and other assets (55,043) (64,254) (74,090) (95,638) (107,349) 28,645 $203,105 $208,166 $214,118 $219,579 $24,556 $ 229,055 26,484 27,543 29,791 30,983 32,222 Total Assets LIABILITIES Accounts payable-trade Current accrued expenses $ 38,080 $ 38,131 $ 39,806 $ 41,398 21,156 $ 43,054 $ 44,777 18,808 19,560 20,343 22,003 22,883 7,219 Notes payable and short-term debt Current maturities of long-term 6,805 7,009 7436 7,659 7,889 debt 5,914 6,091 6,274 6,462 6,656 6,856 2,488 2,563 $ 81,861 $ 84,967 Income taxes payable 2,211 $ 71,818 2,277 $ 73,069 2,346 $ 75,988 43,939 2416 $ 78,869 Current Liabilities Long-term debt 41,417 42,660 45,257 46,615 48,014 Deferred tax liabilities-noncurrent 7,613 7,841 8,077 8,319 8,568 8,826 Redeemable noncontrolling interest 519 Total Liabilities $121,367 $123,570 $1 28,004 $132,446 $137,045 $ 141,807 SHAREHOLDERS' EQUITY Common stock + paid-in capital Retained earnings 3,952 4,163 4,282 4,392 4,491 4,581 72,978 75,625 77,023 77,934 78,213 77,859 Accum. other comprehensive income (loss) (587) $ 76,343 (587 $ 79,201 (587) $ 80,719 5,395 (587) (587) (587) Common Shareholders' EQUITY $ 81,738 $ 82,117 $ 81,853 Noncontrolling interests Total EQUITY 5,395 5,395 5,395 5,395 5,395 87,248 81,738 $203,105 84,596 86,114 $214,118 87,133 $219,579 87,512 Total Liabilities and Equities $208,166 $224,556 $ 229,055 Source for Actual 2012 Walmart Stes, Inc., Form 10K for the Fiscal Year Ended January 31, 2013. Exhibit 12.19 Walmart Stores, Inc. Projected Implied Statements of Cash Rows for Year +1 through Year +5 (Problem 12.17) Projected Year +1 Year +2 Year +3 Year +4 Year +5 IMPLIED STATEMENTS OF CASH FLOWS $ 18,476 $ 20,005 10,461 Net income $ 19,225 $ 20,816 $ 21,660 Add back depreciation expense (net) (Increase) Decrease in receivables-net (Increase) Decrease in inventories (Increase) Decrease in prepaid expenses 9,211 9,836 11,086 11,711 (338) 355) (373) (392) (411) (1,985) (311) (1,765) (1,835) (69) (1,909) (64) (66) (71) (74) Increase (Decrease) in accounts payable-trade 51 1,675 1,592 1,656 1,722 Increase (Decrease) in current acaued liabilities 752 782 814 846 880 Increase (Decrease) in income taxes payable 66 68 70 72 75 Net change in deferred tax assets and liabilities 228 235 242 250 257 Net Cash Flows from Operations $ 28,072 $ 29,636 $ 30,908 $ 32,355 $ 33,835 (Increase) Decrease in prop, plant, & equip, at cost (Increase) Decrease in goodwill and nonamort. intang. (12,500) (12,500) (12,500) (12,500) (12,500) (820) (853) (887) (922) (959) (Increase) Decrease in other noncurrent assets (239) $(13,559) 249) $(13,602) (259) $(13,646) (269) $(13,692) (280) $(13,739) Net Cash Flows from Investing Activities Increase (Decrease) in short-term debt 382 393 405 417 429 Increase (Decrease) in long-term debt Increase (Decrease) in redeemable noncontrolling interest Increase (Decrease) in common stock + paid-in capital 1,243 1,280 1,318 1,358 1,398 (519) 211 119 109 100 90 Increase (Decrease) in accumulated OCI Dividends (15,020) (17,017) (18,285) (19,728) (21,204) Increase (Decrease) in noncontrolling interests Net Cash Flows from Financing Activities (809) B09) $(16,035) (809) (809) $(18,663) (809) $(14,513) $(17,262) $(20,096) Net Change in Cash

> How could the AMT be calculated without using regular taxable income as a starting point? Be specific.

> Kelly recently was promoted and received a substantial raise. She talks to her tax adviser about the potential tax ramifications. After making some projections, her adviser “welcomes her to the AMT club.” Kelly believes that it is unfair that she must pa

> During the year, Rachel earned $18,000 of interest income on 2011 private activity bonds. She incurred interest expense of $7,000 in connection with amounts borrowed to purchase the bonds. What is the effect of these items on Rachel’s taxable income? On

> During the year, Ricardo made the following contributions to a qualified public charity: Cash……………………………………………………………………………………$220,000 Stock in Seagull, Inc. (a publicly traded corporation)………………280,000 Ricardo acquired the stock in Seagull, Inc., as an

> Joan is a self-employed consultant. What is her exposure to the Federal selfemployment tax? Discuss the tax rates that apply to Joan’s profits and the income base amounts for the year.

> A friend tells you that she does not worry about the AMT because she does not itemize deductions and, as a result, she does not generate many AMT adjustments. Evaluate your friend’s assertion.

> Wesley, who is single, listed his personal residence with a real estate agent on March 3, 2017, at a price of $390,000. He rejected several offers in the $350,000 range during the summer. Finally, on August 16, 2017, he and the purchaser signed a contrac

> Matt, who is single, always has elected to itemize deductions rather than take the standard deduction. In prior years, his itemized deductions always exceeded the standard deduction by a substantial amount. As a result of paying off the mortgage on his r

> Celine will be subject to the AMT in 2017. She owns an investment building and is considering disposing of it and investing in other realty. Based on an appraisal of the building’s value, the realized gain would be $85,000. Ed has offered to purchase the

> In 1998, Douglas purchased an office building for $500,000 to be used in a business. Douglas sells the building in the current tax year. Explain why the recognized gain or loss for regular income tax purposes is different from any recognized gain or loss

> Howard’s roadside vegetable stand (adjusted basis of $275,000) is destroyed by a tractor-trailer accident. He receives insurance proceeds of $240,000 ($300,000 fair market value $60,000 coinsurance). Howard immediately uses the proceeds plus additional c

> Evaluate the validity of the following statements: If the stock received under an incentive stock option (ISO) is sold in the year of exercise, there is no AMT adjustment. If the stock is sold in a later year, there will be an AMT adjustment then.

> Evaluate the validity of the following statement: In a year in which depreciable personal property is sold, the amount of the AMT gain adjustment equals the amount of the current year’s AMT depreciation adjustment.

> Alfred is single, and his AMTI of $350,000 consists of the following. What tax rates are applicable in calculating Alfred’s TMT? Ordinary income………………..$250,000 Long-term capital gains…………70,000 Qualified dividends……………….30,000

> Andrew and Monica, unrelated individuals, use the same Federal income tax filing status (head of household). However, Monica’s AMT exemption amount is $52,800, while Andrew’s is $0. Explain.

> An AMT liability results if the tentative minimum tax (TMT) exceeds the regular income tax liability. But what happens if the regular income tax liability exceeds the TMT? Does this create a negative AMT that can be carried to other years? Explain.

> How might a taxpayer who cannot avoid engaging in activities that generate AMT adjustments minimize or eliminate such adjustments?

> Mark and Lisa are approaching an exciting time in their lives as their oldest son, Austin, graduates from high school and moves on to college. What are some of the tax issues that Mark and Lisa should consider as they think about paying for Austin’s coll

> Karl purchased his residence on January 2, 2016, for $260,000, after having lived in it during 2015 as a tenant under a lease with an option to buy clause. On August 1, 2017, Karl sells the residence for $315,000. On June 13, 2017, Karl purchases a new r

> Auralia owns stock in Orange Corporation and Blue Corporation. She receives a $10,000 distribution from both corporations. The instructions from Orange state that the $10,000 is a dividend. The instructions from Blue state that the $10,000 is not a divid

> Liz had AGI of $130,000 in 2017. She donated Bluebird Corporation stock with a basis of $10,000 to a qualified charitable organization on July 5, 2017. a. What is the amount of Liz’s deduction assuming that she purchased the stock on December 3, 2016, an

> A depreciable business dump truck has been owned for four years and is no longer useful to the taxpayer. What would have to be true for the disposition of the dump truck to generate at least some § 1231 loss?

> Jacob, age 42, and Jane Brewster, age 37, are married and file a joint return in 2017. The Brewsters have two dependent children, Ellen and Sean, 10-year-old twins. Jacob is a factory supervisor; he earned $95,000 in 2017. Jane is a computer systems anal

> Robert A. Kliesh, age 41, is single and has no dependents. Robert’s Social Security number is 111-11-1112. His address is 201 Front Street, Missoula, MT 59812. He does not contribute to the Presidential Election Campaign fund through the Form 1040. Rober

> This year, Brennen sold a machine used in his business for $180,000. The machine was put into service eight years ago for $340,000. Depreciation up to the date of the sale for regular income tax purposes was $210,000; it was $190,000 for AMT purposes. Wh

> In March 2017, Serengeti exercised an ISO that had been granted by his employer, Thunder Corporation, in December 2014. Serengeti acquired 5,000 shares of Thunder stock with a strike price of $65 per share. The fair market value of the stock at the date

> Compute the 2017 AMT exemption for the following taxpayers. a. Bristol, who is single, reports AMTI of $149,500. b. Marley and Naila are married and file a joint tax return. Their AMTI is $498,000.

> Elijah, who is single, holds a $12,000 AMT credit available from year 1. For year 2, Elijah’s regular tax liability is $28,000, and his TMT is $24,000. Does Elijah owe any AMT for year 2? If so, how much (if any) of the AMT credit can he use for that yea

> Yanni, a single individual, reports the following information for the tax year. Salary……………………………………….$80,000 State income taxes…………………...…..6,800 Mortgage interest expense…………….6,200 Charitable contributions…………………1,500 Interest income……………………………..1,30

> Dimitri owns a gold mine that qualifies for a 15% percentage depletion rate. The basis of the property at the beginning of the year, prior to any current year depletion deduction, is $21,000. Gross income from the property for the year is $200,000; taxab

> Kiki, who incurred intangible drilling costs (IDC) of $94,000 during the year, deducted that amount for regular tax purposes. Her net oil and gas income for the year was $110,000. Kiki has calculated her current-year IDC preference to be $9,400. Is this

> Wanda, a calendar year taxpayer, owned a building (adjusted basis of $250,000) in which she operated a bakery that was destroyed by fire in December 2017. She receives insurance proceeds of $290,000 for the building the following March. Wanda is consider

> An individual taxpayer had a net § 1231 loss in 2017. Could any of this loss be treated as a long-term capital loss? Why or why not?

> Shontelle owns an apartment house that has an adjusted basis of $760,000 but is subject to a mortgage of $192,000. She transfers the apartment house to Dave and receives from him $120,000 in cash and an office building with a fair market value of $780,00

> Jorge owns two passive investments, Activity A and Activity B. He plans to sell Activity A in the current year or next year. Juanita has offered to buy Activity A this year for an amount that would produce a taxable passive activity gain to Jorge of $115

> In the current year, Bill Parker (54 Oak Drive, St. Paul, MN 55164) is considering making an investment of $60,000 in Best Choice Partnership. The prospectus provided by Bill’s broker indicates that the partnership investment is not a passive activity an

> In 2016, Fred invested $50,000 in a general partnership. Fred’s interest is not considered to be a passive activity. If his share of the partnership losses is $35,000 in 2016 and $25,000 in 2017, how much can he deduct in each year?

> Helen Derby borrowed $150,000 to acquire a parcel of land to be held for investment purposes. During the current year, she reported AGI of $90,000 and paid interest of $12,000 on the loan. Other items related to Helen’s investments include the following:

> In 2017, Kathleen Tweardy incurs $30,000 of interest expense related to her investments. Her investment income includes $7,500 of interest, $6,000 of qualified dividends, and a $12,000 net capital gain on the sale of securities. Kathleen asks you to comp

> Tonya sells a passive activity in the current year for $150,000. Her adjusted basis in the activity is $50,000, and she uses the installment method of reporting the gain. The activity has suspended losses of $12,000. Tonya receives $60,000 in the year of

> Commercial Bank has initiated an advertising campaign that encourages customers to take out home equity loans to pay for purchases of automobiles. Are there any tax advantages related to this type of borrowing? Explain.

> Dan, a self-employed individual taxpayer, prepared his own income tax return for the past year and has asked you to check it for accuracy. Your review indicates that Dan failed to claim certain business entertainment expenses. a. Will the correction of t

> Explain why market-to-book valuation multiples demonstrate less variance over time and across firms than do price-earnings valuation multiples.

> Identify three economic factors that will drive a firm’s price-earnings ratio to decrease over time. Identify three accounting factors that will drive a firm’s price-earnings ratio down in a given period.

> Identify three economic factors that will drive a firm’s price-earnings ratio to be higher than that of other firms in the same industry. Identify three accounting factors that will drive a firm’s price-earnings ratio in a given period to be higher than

> In practice, it is common to observe price-earnings ratios measured as current period price divided by trailing-twelve-months (or most recent annual) earnings per share. Identify and explain three potential flaws inherent in this measurement of the price

> In conceptual terms, explain the value-earnings ratio. Explain the difference between the value-earnings ratio and the price-earnings ratio. What is the critical assumption about future earnings in both the value-earnings and price-earnings ratio?

> Identify three economic factors that will drive a firm’s value-to-book ratio to decrease over time. Identify three accounting factors that will drive a firm’s value-to-book ratio to decrease over time.

> Identify three economic factors that will drive a firm’s value-to-book ratio to be higher than that of other firms in the same industry. Identify three accounting factors that will drive a firm’s value-to-book ratio to be higher than that of other firms

> In this chapter, we evaluated shares of common equity in PepsiCo using the value-to-book approach, market multiples, price differentials, and reverse engineering. The Coca-Cola Company competes directly with PepsiCo. The data in Chapter 12 Exhibits 12.14

> Explain the implications of a value to-book ratio that is greater than the market-to-book ratio. Explain the implications of a value to-book ratio that is less than the market-to-book ratio.

> The Coca-Cola Company is a global soft-drink beverage company that is a primary and direct competitor with PepsiCo. The data in Chapter 12 Exhibits 12.14–12.16 include the actual amounts for 2012 and projected amounts for Year +1 to Yea

> In 2000, Enron enjoyed remarkable success in the capital markets. During that year, Enron’s shares increased in value by 89%, while the S&P 500 index fell by 9%. At the end of 2000, Enron’s shares were trading at roughly $83 per share and all of the sell

> This problem explores the sensitivity of the value-earnings and value-to-book models to changes in underlying assumptions. We recommend that you design a computer spreadsheet to perform the calculations, particularly for the value-to-book ratio. REQUIRE

> Exhibit 14.12 presents data on market-to-book ratios, ROCE, the cost of equity capital, and price-earnings ratios for seven pharmaceutical companies. (Note that price-earnings ratios for these firms typically fall in the 30–35 range.) E

> Problem 13.18 and Exhibit 13.7 in Chapter 13 present selected hypothetical data from projected financial statements for Steak ‘n Shake for Year +1 to Year +11. The amounts for Year +11 reflect a long-term growth assumption of 3%. The co

> Using the evidence presented in Exhibit 14.10, describe the extent to which the market is efficient with respect to quarterly earnings surprises during the 60 trading days prior to quarterly earnings announcements. Using the evidence presented in Exhibit

> Explain the role of analysts in increasing capital market efficiency.

> What does market efficiency mean? What does market efficiency not mean? Explain how market efficiency relates to the amount of information that affects share prices and the speed with which information affects share prices.

> Explain reverse engineering of share prices in conceptual terms. How does reverse engineering of share prices enable an analyst to infer (or deduce) the assumptions that the capital markets appear to impound in share price?

> What does a price differential measure? How does a price differential relate to risk?

> In Integrative Case 10.1, we projected financial statements for Starbucks for Years +1 through +5. In this portion of the Starbucks Integrative Case, we use the projected financial statements from Integrative Case 10.1 and apply the techniques in Chapter

> Each column presents financial information taken from one of four different companies, with one or more items of data missing. Required: Use your understanding of the relationships among financial statements and financial statement items to find the mi

> Parker Renovation Inc. renovates historical buildings for commercial use. During 2019, Parker had $763,400 of revenue from renovation services and $5,475 of interest income from miscellaneous investments. Parker incurred $222,900 of wages expense, $135,0

> Information for TTL Inc. is given below. Required: Use the relationships in the balance sheet, income statement, and retained earnings statement to determine the missing values. Total assets at the beginning of the year S (a) Total assets at the en

> At the beginning of 2019, Huffer Corporation had total assets of $232,400, total liabilities of $94,200, common stock of $50,000, and retained earnings of $88,200. During 2019, Huffer had net income of $51,750, paid dividends of $10,000, and issued addit

> Carson Corporation reported the following amounts for assets and liabilities at the beginning and end of a recent year. Required: Calculate Carson’s net income or net loss for the year in each of the following independent situations: 1.

> Data from the financial statements of four different companies are presented in separate columns in the table below. Each column has one or more data items missing. Required: Use your understanding of the relationships among the financial statement item

> The following information relates to Ashton Appliances for 2019. Accounts payable $ 16,800 Income taxes expense $ 16,650 Accounts receivable 69,900 Income taxes payable 12,000 Accumulated depreciation (building) 104,800 Insurance expense 36,

> The table below presents the retained earnings statements for Bass Corporation for 3 successive years. Certain numbers are missing. Required: Use your understanding of the relationship between successive retained earnings statements to calculate the miss

> Dittman Expositions has the following data available: Dividends, 2019 $ 10,250 Retained earnings, 12/31/2018 $ 20,900 Dividends, 2020 12,920 Revenues, 2019 407,500 Expenses, 2019 382,100 Revenues, 2020 451,600 Expenses, 2020 418,600 Required

> The following information for Rogers Enterprises is available at December 31, 2019, and includes all of Rogers’ financial statement amounts except retained earnings: Accounts receivable $72,920 Property, plant, and equipment $ 90,000 Cash 13,240

> What types of questions are answered by the financial statements?

> Each column presents financial information taken from one of four different companies, with one or more items of data missing. Required: Use your understanding of the relationships among financial statements and financial statement items to determine t

> Powers Wrecking Service demolishes old buildings and other structures and sells the salvaged materials. During 2019, Powers had $425,000 of revenue from demolition services and $137,000 of revenue from salvage sales. Powers also had $1,575 of interest in

> Information for Beethoven Music Company is given below. Total assets at the beginning of Equity at the beginning of the year $ (b) the year $145,200 Equity at the end of the year 104,100 Total assets at the end of the year (a) Divid

> Which of the following statements is true? a. The auditor’s opinion is typically included in the notes to the financial statements. b. The notes to the financial statements are an integral part of the financial statements that clarify and expand on the i

> Which of the following sentences regarding the statement of cash flows is false? a. The statement of cash flows describes the company’s cash receipts and cash payments for a period of time. b. The statement of cash flows reconciles the beginning and endi

> Which of the following statements concerning retained earnings is true? a. Retained earnings is the difference between revenues and expenses. b. Retained earnings is increased by dividends and decreased by net income. c. Retained earnings represents accu

> For the most recent year, Grant Company reported revenues of $182,300, cost of goods sold of $108,800, inventory of $8,500, salaries expense of $48,600, rent expense of $12,000, and cash of $12,300. What was Grant’s net income? a. $9,400 b. $12,900 c. $2

> Which of the following statements regarding the income statement is true? a. The income statement provides information about the profitability and growth of a company. b. The income statement shows the results of a company’s operations at a specific poin

> Refer to the information for Marker above. What is Marker’s stockholders’ equity? a. $7,500 b. $17,500 c. $19,100 d. $25,000

> Refer to the information for Marker above. What is the total of Marker’s current assets? a. $12,100 b. $13,700 c. $14,500 d. $25,000

> Name and briefly describe the purpose of the four financial statements.

> Which of the following is not shown in the heading of a financial statement? a. The title of the financial statement b. The name of the company c. The time period covered by the financial statement d. The name of the auditor

> What type of questions do the financial statements help to answer? a. Is the company better off at the end of the year than at the beginning of the year? b. What resources does the company have? c. For what did a company use its cash during the year? d.

> Which of the following is not one of the four basic financial statements? a. Balance sheet b. Income statement c. Statement of cash d. Auditor’s report

> At December 31, Pitt Inc. has assets of $12,900 and liabilities of $6,300. What is the stockholders’ equity for Pitt at December 31? a. $6,600 b. $6,300 c. $18,100 d. $19,200

> Cam and Anna met during their freshman year of college as they were standing in line to buy tickets to a concert. While waiting in line, the two shared various aspects of their lives. Cam, whose father was an executive at a major record label, was raised

> Refer to the 10-K reports of Under Armour, Inc., and Columbia Sportswear that are available for download from the companion website at CengageBrain.com. Required: Answer the following questions: 1. Describe each company’s business and list some of the m

> Obtain Apple Inc.’s 2016 annual report either through the ‘‘Investor Relations’’ portion of their website (do a web search for Apple investor relations) or go to www.sec.gov and click ‘‘Company Filings Search’’ under ‘‘Filings.’’ Required: Answer the fo

> Lola, the CEO of JB Inc., and Frank, the accountant for JB Inc., were recently having a meeting to discuss the upcoming release of the company’s financial statements. Following is an excerpt of their conversation: Lola: These financial statements don’t s

> Professional ethics guide public accountants in their work with financial statements. Required: Why is ethical behavior by public accountants important to society? Be sure to describe the incentives that public accountants have to behave ethically and u

> Reproduced below are portions of the president’s letter to stockholders and selected income statement and balance sheet data for the Wright Brothers Aviation Company. Wright Brothers is a national airline that provides both passenger se

> Define the terms revenue and expense. How are these terms related?

> Agency Rent-A-Car Inc. rents cars to customers whose vehicles are unavailable due to accident, theft, or repair (‘‘Wheels while your car heals’’). The company has a fleet of more tha

> Which of the following statements regarding business activities is true? a. Operating activities involve buying the long-term assets that enable a company to generate revenue. b. Financing activities include obtaining the funds necessary to begin and ope

> The accounting profession is organized into three major groups: (a) Accountants who work in nonbusiness entities, (b) Accountants who work in business entities, and (c) Accountants in public practice. The periodical literature of accounting includes

> Jim Hadden is a freshman at Major State University. His earnings from a summer job, combined with a small scholarship and a fixed amount per term from his parents, are his only sources of income. He has a new MasterCard that was issued to him the week he

> Which of the following statements is false concerning forms of business organization? a. A corporation has tax advantages over the other forms of business organization. b. It is easier for a corporation to raise large sums of money than it is for a sole