Question: You are conducting an audit of the

You are conducting an audit of the financial statements of a wholesale cosmetics distributor with an inventory consisting of thousands of individual items. The distributor keeps its inventory in its own distribution center and in two public warehouses. A perpetual inventory computer database is maintained on a computer disk. The database is updated at the end of each business day. Each record of the perpetual inventory database contains the following data:

Item number.

Location of item.

Description of item.

Quantity on hand.

Cost per item.

Date of last purchase.

Date of last sale.

Quantity sold during year.

You are planning to observe the distributor’s physical count of inventories as of a given date. The client will provide a computer file of the preceding items taken from its database as of the date of the physical count. Your firm has a computer audit plan that will be ideal for analyzing the inventory records.

Required:

List the basic inventory auditing procedures and, for each, describe how the use of CAATs and the computerized perpetual inventory database might be helpful to the auditor in performing such auditing procedures. (See Appendix 9B for substantive procedures for inventory.) Organize your answer as follows:

Transcribed Image Text:

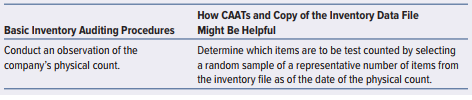

How CAATS and Copy of the Inventory Data File Basic Inventory Auditing Procedures Might Be Helpful Conduct an observation of the Determine which items are to be test counted by selecting a random sample of a representative number of items from the inventory file as of the date of the physical count. company's physical count.

> An auditor most likely would analyze inventory turnover rates to obtain evidence concerning management’s balance assertions about a. Existence. b. Rights and obligations. c. Completeness. d. Valuation and allocation.

> Which of the following auditing procedures probably would provide the most reliable evidence concerning the entity’s assertion of rights and obligations related to inventories? a. Trace test counts noted during the entity’s physical count to the entity’s

> Explain dual-direction sampling in the context of inventory test counts.

> What characteristics should be considered in reviewing a client’s inventory-taking instructions?

> ABC Company has 100 shares of IBM stock that it holds as an investment. The stock was purchased three years ago and has been in the client’s safe deposit box along with other investment securities. During an inspection of securities held by the client, t

> Why should receiving reports be prenumbered? What assertion would an auditor test using the receiving reports, and how would the auditor do this?

> To determine the client’s planned amount and timing of production of a product, the auditor reviews the a. Sales forecast. b. Inventory reports. c. Production plan. d. Purchases journal.

> The purpose of tracing a sample of inventory tags to a client’s computerized listing of inventory items is to determine whether the inventory items a. Represented by tags were included on the listing. b. Included on the listing were properly counted. c.

> Which of the following approaches is most suitable for auditing the finance and investment cycle? a. Perform extensive tests of controls and limit substantive procedures to analytical procedures. b. Ignore internal controls and perform extensive substant

> A portion of a client’s inventory is in public warehouses. Evidence of the existence of this merchandise can most efficiently be acquired through which of the following methods? a. Observation. b. Confirmation. c. Calculation. d. Inspection.

> Which of the following management assertions is an auditor most likely testing if the audit objective states that all inventory on hand is reflected in the ending inventory balance? a. The entity has rights to the inventory. b. Inventory is properly valu

> An auditor is examining a nonpublic company’s inventory procurement system and has decided to perform tests of controls. Under which of the following conditions do GAAS require tests of controls be performed by an auditor? a. Significant weaknesses were

> Your client counts inventory three months before the end of the fiscal year because controls over inventory are excellent. Which procedure is not necessary for the roll-forward? a. Check that shipping documents for the last three months agree with perpet

> What is a compensating control? Give some examples for finance and investment cycle accounts.

> What procedures do auditors employ to audit inventory when the physical inventory is taken on a cycle basis or on a statistical plan but never a complete count on a single date?

> An auditor selected items for test counts while observing a client’s physical inventory. The auditor then traced the test counts to the client’s inventory listing. This procedure most likely obtained evidence concerning management’s balance assertion of

> Describe the activities a company should perform to ensure appropriate reconciliation of marketable securities.

> A client maintains perpetual inventory records in quantities and in dollars. If the assessed control risk is high, an auditor would probably a. Apply gross profit tests to ascertain the reasonableness of the physical counts. b. Increase the extent of tes

> You have been assigned to trace the results of the observation of Brightware China’s physical inventory count to its pricing and compilation. You note the following conditions. 1. The last inventory tag documented by Mark Hulse, the auditor who observed

> Which of the following internal control activities most likely addresses the completeness assertion for inventory? a. The work-in-process account is periodically reconciled with subsidiary inventory records. b. Employees responsible for custody of finish

> Follow the instructions preceding Problem 9.61. Write the audit approach section following the case in the chapter. SueCan Corporation manufactured electronic and other equipment for private customers and government defense contracts. It deferred costs u

> From the auditors’ point of view, inventory counts are more acceptable prior to the year-end when a. Internal control is weak. b. Accurate perpetual inventory records are maintained. c. Inventory is slow moving. d. Significant amounts of inventory are he

> A retailer’s physical count of inventory was higher than that shown by the perpetual records. Which of the following could explain the difference? a. Inventory items had been counted, but the tags placed on the items had not been taken off and added to t

> An auditor usually traces the details of the test counts made during the observation of physical inventory counts to a final inventory compilation. This audit procedure is undertaken to provide evidence that items physically present and observed by the a

> The diagram in Exhibit 9.51.1 describes several cost accounting tests of controls. It shows the direction of the tests, leading from samples of cost accounting analyses, management reports, and the general ledger to blank squares. Required: For each bla

> Mattel Inc., a manufacturer of toys, failed to write off obsolete inventory, thereby overstating inventory and improperly deferred tooling costs, both of which understated cost of goods sold and overstated income. “Excess” inventory was identified by co

> The list of vouchers payable for Potter’s Magic Shoppe at December 31 is as follows: Checks written in the following January are: Required a. Prepare an audit plan for the audit of unrecorded liabilities for Potter’

> What documents would a company need to correctly account for its investment securities, and what information would they obtain from these documents?

> You are supervising the audit fieldwork of Sparta Springs Company and need certain information from Sparta’s equipment records, which are maintained on a computer file. The particular information is (1) net book value of assets so that your assistant can

> Each of the following tests of controls could be performed during the audit of the controls in the production cycle. Required: For each procedure, identify (a) the internal control activity (strength) being tested and (b) the assertion(s) being addresse

> A client has a large and active investment portfolio that is kept in a bank safe deposit box. If the auditors are unable to count securities at the balance sheet date, they most likely will a. Request the bank to confirm to the auditors the contents of t

> Following are the four assertions about account balances that can be applied to the audit of a company’s PP&E, including assets the company has constructed itself: existence, rights and obligations, completeness, and valuation and allocation. Required:

> This question contains three items that are management assertions about property and equipment. Following them are several substantive procedures for obtaining evidence about management’s assertions. Assertions 1. The entity has legal right to property

> Bart’s Company has prepared the PP&E and depreciation schedule shown in Exhibit 8.50.1. The following information is available. (Assume the beginning balance has been audited :) The land was purchased eight years ago whe

> This case is designed like the ones in the chapter. Your assignment is to write the “audit approach” portion of the case organized around these sections: Objective. Express the objective in terms of the facts supposedly asserted in financial records, acc

> Maine Construction builds office buildings. The buildings generally cost between $5 million and $8 million to build, and the plumbing can cost between $300,000 and $600,000 depending on the building requirements. Therefore, Maine always sends the plumb

> The following case is designed like the ones in the chapter. Your assignment is to write the audit approach portion of the cases organized around these sections: Objective. Express the objective in terms of the facts supposedly asserted in financial rec

> C. Marsh, CPA, is the independent auditor for Compufast Corporation, which sells personal computers, peripheral equipment (printers, data storage), and a wide variety of programs for business and games. From experience on Compufast’s previous audits, Mar

> Who is normally responsible for the authorization of investment activities? Why is the authorization normally performed at this level?

> An audit plan to examine long-term debt most likely would include steps that require a. Comparing the carrying amount of held-to-maturity securities with their year-end market values. b. Correlating interest expense recorded for the period with outstandi

> Partners Clark and Kent, both CPAs, are preparing their audit plan for the audit of accounts payable on Marlboro Corporation’s annual audit. Saturday afternoon they reviewed the thick file of last year’s documentation, and they both remembered too well t

> You are in the final stages of your audit of the financial statements of Ozine Corporation for the year ended December 31, 2017, when the corporation’s president consults you. The president believes there is no point to your examining the 2015 voucher re

> What assertions found in PP&E, investments, and intangibles accounts are of interest to an auditor during the examination of the expenditure and acquisition cycle?

> Refer to the internal control questionnaire for the production cycle (Appendix Exhibit 9A.1) and assume that the answer to each question is “no.” Prepare a table matching questions to errors or frauds that could occur

> Following is a selection of items from internal control questionnaires. 1. Are purchase orders above a certain level approved by an officer? 2. Are the quantity and quality of goods received determined at the time of receipt by receiving personnel indepe

> Which of the following tests of details most likely would help an auditor determine whether accounts payable have been misstated? a. Examining reported purchase returns that appear too low. b. Examining vendor statements for amounts not reported as purch

> A company employs three accounts payable clerks and one treasurer. Their responsibilities are as follows: Which of the following would indicate a weakness in the company’s internal control? a. Clerk 1 opens all of the incoming mail. b

> In a test of controls, auditors may trace receiving reports to vouchers recorded in the voucher register. This is a test for a. Occurrence. b. Completeness. c. Classification. d. Cutoff.

> When auditing account balances of liabilities, auditors are most concerned with management’s assertion about a. Existence. b. Rights and obligations. c. Completeness. d. Valuation and allocation.

> Which of the following accounts would most likely be audited in connection with a related balance-sheet account? a. Property Tax Expense. b. Payroll Expense. c. Research and Development. d. Legal Expense.

> An audit team would most likely examine the detail support for charges to which of the following accounts? a. Payroll expense. b. Cost of goods sold. c. Supplies expense. d. Legal expense.

> Curtis, a maintenance supervisor, submitted maintenance invoices from a phony repair company and received the checks at a post office box. This should have been prevented by a. Comparison of the company name to the approved vendor list by the check signe

> In auditing for unrecorded long-term bonds payable, an audit team most likely will a. Perform analytical procedures on the bond premium and discount accounts. b. Examine documentation of assets purchased with bond proceeds for liens. c. Compare interest

> How do audit procedures for prepaid expenses and accrued liabilities also provide audit evidence about related expense accounts?

> A furniture company ordered 84 tables from a supplier. The supplier accidentally sent only 48 tables, but the receiving department at the furniture company accepted the tables. The invoice was eventually received but was for the original 84 tables. The f

> You are auditing Martha’s Prison Clothes Inc. as of December 31, 2014. The inventory for orange jumpsuits shows 1,263 suits at $782 for a total of $987,666. When you look at the invoices for the jumpsuits, you see the following: Requi

> When verifying debits to the perpetual inventory records of a nonmanufacturing company, auditors would be most interested in examining a sample of purchase a. Approvals. b. Requisitions. c. Invoices. d. Orders.

> To determine whether accounts payable are complete, auditors perform a test to verify that all merchandise received has been recorded. The population for this test consists of all a. Vendors’ invoices. b. Purchase orders. c. Receiving reports. d. Cancele

> Which of the following procedures is least likely to be performed before the balance-sheet date? a. Observation of inventory. b. Review of internal control over cash disbursements. c. Search for unrecorded liabilities. d. Confirmation of receivables.

> How should an audit team assess the reasonableness of a film studio’s estimate of film revenues? (Refer to the No Treasure in This Treasure Planet case.)

> Which of the following is the best audit procedure for determining the existence of unrecorded liabilities? a. Examine confirmation requests returned by creditors whose accounts are on a subsidiary trial balance of accounts payable. b. Examine a sample o

> Budd, the purchasing agent of Lake Hardware Wholesalers, has a relative who owns a retail hardware store. Budd arranged for hardware to be delivered by manufacturers to the retail store on a cash-on-delivery (C.O.D.) basis, thereby enabling his relative

> When auditing inventories, an auditor would least likely verify that a. All inventory owned by the client is on hand at the time of the count. b. The client has used proper inventory pricing. c. The financial statement presentation of inventories is appr

> A client’s purchasing system ends with the recording of a liability and its eventual payment. Which of the following best describes auditors’ primary concern with respect to liabilities resulting from the purchasing system? a. Accounts payable are not ma

> Which of the following would not overstate current-period net income? a. Capitalizing an expenditure that should be expensed. b. Failing to record a liability as an expense. c. Failing to record a check paying an item in Vouchers Payable. d. All of the a

> Why is it important for auditors to obtain control information over inventory count sheets or tickets?

> For which of the following accounts would the matching concept be the most appropriate? a. Cost of goods sold. b. Research and development. c. Depreciation expense. d. Sales.

> An audit team testing long-term investments would ordinarily use analytical procedures to ascertain the reasonableness of the a. Existence of unrealized gains or losses. b. Completeness of recorded investment income. c. Classification as available-for-sa

> Which of the following audit procedures would not likely be performed for audits of investments? a. Read board of directors’ minutes for authorization of investment strategies. b. Confirm investments with registrar. c. Confirm investments with broker or

> Which of the following accounts does not appear in the acquisition and expenditure cycle? a. Cash. b. Purchases returns. c. Sales returns. d. Prepaid insurance.

> How could auditors have discovered the off-balance-sheet financing described in the Off-Balance-Sheet Inventory Financing case?

> Which of the following procedures would best prevent or detect the theft of valuable items from an inventory that consists of hundreds of different items selling for $1 to $10 and a few items selling for hundreds of dollars? a. Maintain a perpetual inven

> What features of the cost accounting system would be expected to prevent the omission of recording materials used in production?

> An audit team would most likely verify the interest earned on bond investments by a. Vouching the receipt and deposit of interest checks. b. Confirming the bond interest rate with the issuer of the bonds. c. Recomputing the interest earned on the basis o

> What primary functions should be separated in the acquisition and expenditure cycle?

> What makes the recording of inventory at its proper amount difficult on the financial statements?

> What are the short-term effect and the long-term effect of improperly capitalizing expenditures on the financial statements?

> Why is a service expense a good account for recording a fictitious expense?

> To make a year-to-year comparison of inventory turnover most meaningful, the auditor performs the analysis a. For the company as a whole. b. By division. c. By product. d. All of the above.

> If the actual sales for the year are substantially lower than the sales forecasted at the beginning of the year, what potential valuation problems could arise in the production cycle accounts?

> How might an auditor use a client’s sales forecast for general familiarity with the production cycle or for evaluation of slow-moving inventory?

> What unfortunate lesson did the auditors learn from the situation in the Unregistered Sale of Securities case? What should auditors do when a violation of U.S. securities laws is suspected?

> Why is a “blind” purchase order used as a receiving report document?

> How can purchasing managers use their position to defraud the company? What can be done to prevent it?

> Your client, Boos & Becker Inc., is a medium-size manufacturer of products for the leisure-time activities market (camping equipment, scuba gear, bows and arrows, and the like). During the past year, a computer system was installed, and inventory records

> What is a voucher? What is a voucher package?

> What are some of the important assertions found in investment accounts?

> When an entity uses a trust company as custodian of its marketable securities, the possibility of concealing fraud most likely would be reduced if the a. Trust company has no direct contact with the entity employees responsible for maintaining investment

> What documentation should an auditor inspect when a client has paid off a bank note? How could an employee defraud the company if the bank note has no indication of being paid?

> You are engaged in the audit of the financial statements of Bass Corporation for the year ended December 31 and you are about to begin an audit of the investment securities. Bass’s records indicate that the company owns various bearer bonds as well as 25

> When the client holds a large amount of negotiable securities, auditors need to plan to guard against a. Unauthorized negotiation of the securities before they are counted. b. Unrecorded sales of securities after they are counted. c. Substitution of secu

> What are some specific transactions that an auditor would expect to be approved by the board of directors? How would it affect the audit if these transactions were not required to be approved by the board?

> Cassandra Corporation, a manufacturing company, periodically invests large sums in marketable equity securities. The investment committee of the board of directors established the investment policy. The treasurer is responsible for carrying out the inves

> Follow the instructions preceding the case in problem 10.60. Write the audit approach section like the cases in the chapter. Rogue Trader In February 1989, 22-year-old Nicholas Leeson joined Barings Investment Bank. In 1993, he began trading on behalf o

> Follow the instructions preceding the case in problem 10.60. Write the audit approach section like the cases in the chapter. In Plane View Whiz Corporation owned 160,000 shares of Wing Company stock, carried on the books as an investment in the amount o

> Hide the Loss under the Goodwill Gulwest Industries, a public company, decided to discontinue its unprofitable line of business of manufacturing sporting ammunition. Gulwest had capitalized the startup cost of the business, and with its discontinuance, t

> You have been engaged to audit the financial statements of Hardy Hardware Distributors Inc., as of December 31. In your review of the corporate nonfinancial records, you have found that Hardy Hardware owns 15 percent of the outstanding voting common stoc

> You are a CPA engaged in an audit of the financial statements of Pate Corporation for the year ended December 31. The financial statements and records of Pate Corporation have not been audited by a CPA in prior years. The stockholders’ equity section of

> Sammy Smith is the partner in charge of the audit of Blue Distributing Corporation, a wholesaler that owns one warehouse containing 80 percent of its inventory. Smith is reviewing the audit documentation that was prepared to support the firm’s opinion on

> You are the continuing auditor of Sussex Inc. and are beginning the audit of the common stock and treasury stock accounts. You have decided to design substantive procedures with reliance on internal controls. Sussex has no-par, no-stated-value common sto