Question: Arbortech, a designer, manufacturer, and marketer

Arbortech, a designer, manufacturer, and marketer of PC cards for computers, printers, telecommunications equipment, and equipment diagnostic systems, was the darling of Wall Street during Year 6. Its common stock price was the leading gainer for the year on the New York Stock Exchange. Its bubble burst during the third quarter of Year 7 when revelations about seriously misstated financial statements for prior years became known. This case seeks to identify signals of the financial shenanigans and to assess the likelihood of the firm’s future survival. Industry and Products Digital computing and processing have expanded now to include a broad array of mobile applications, including tablets, laptops, cell phones, digital cameras, and medical and automobile diagnostic equipment. A PC card is a rugged, lightweight, credit-card-sized device inserted into a dedicated slot in these products that provides programming, processing, and storage capabilities provided on hard drives in conventional desktop computers. The PC card has a high shock and vibration tolerance, low power consumption, a smaller size (relative to previous technologies), and a high access speed. At the time, the market for PC cards was one of the fastest growing segments of the electronics industry.

Arbortech designs PC cards for four principal industries: (1) communications (routers, cell phones, and local-area networks), (2) transportation (vehicle diagnostics and navigation), (3) mobile computing (handheld data collection terminals and notebook computers), and (4) medical (blood gas analysis systems and defibrillators). The firm targets its engineering and product development, all of which it conducts in-house, to these four industry groups. It works closely with original equipment manufacturers (OEMs) to design PC cards that meet specific needs of products aimed at these four industries. Arbortech also conducts its manufacturing in-house, which allows it to respond quickly to changing requirements and schedules of these OEMs. The firm markets its products using its own salesforce.

In Year 4, Arbortech was incorporated in Delaware. The firm made its initial public offering of common stock (1 million shares) on April 19, Year 4, at a price of $5.625 per share. Each common share issued included a redeemable common stock purchase warrant that permitted the holder to purchase one share of the firm’s common stock for $7.20. Prior to its initial public offering, Arbortech obtained a $550,000 bridge loan during Year 4, which it repaid with proceeds from the initial public offering. Holders of the stock purchase warrants exercised their options during Year 5 and Year 6. The firm obtained equity capital during Year 5 as a result of a private placement of its common stock at $5.83 a share. It issued additional shares to the public during Year 6 at $18 a share. Its stock price was $5.25 on June 30, Year 4; $22.625 on June 30, Year 5; $29.875 on June 30, Year 6; and $52 on December 31, Year 7.

Arbortech maintained a line of credit throughout Year 4 to Year 6 with a major Boston bank to finance its accounts receivables and inventories. The borrowing was at the bank’s prime lending rate. Substantially all of the assets of the firm collateralized this borrowing.

The firm’s chief executive officer, Daniel James, is also its major shareholder. The firm maintains an employment agreement with James under which it pays his compensation to a Swiss executive search firm, which then pays James.

Beginning in Year 6, Arbortech made minority investments in five corporations engaged in technology development, four of which the firm accounts for using the cost method and one of which it accounts for using the equity method. Products developed by these companies could conceivably use PC cards. Arbortech also advanced amounts to some of these companies using interest-bearing notes.

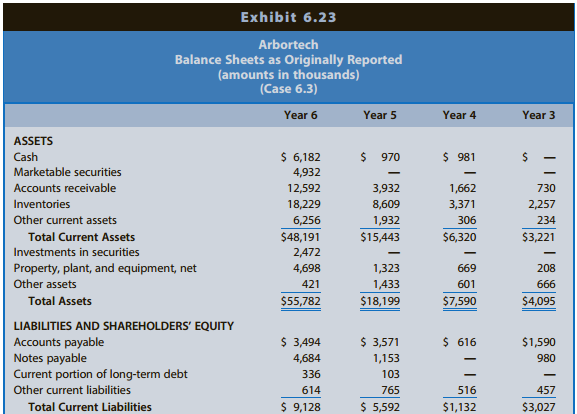

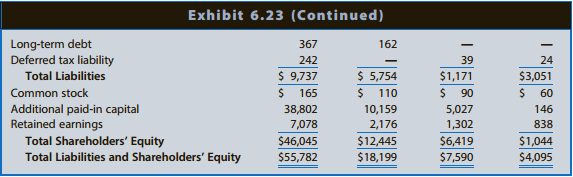

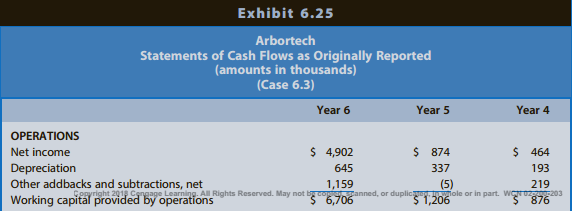

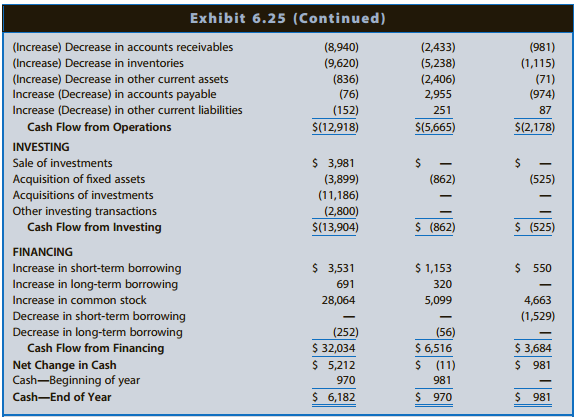

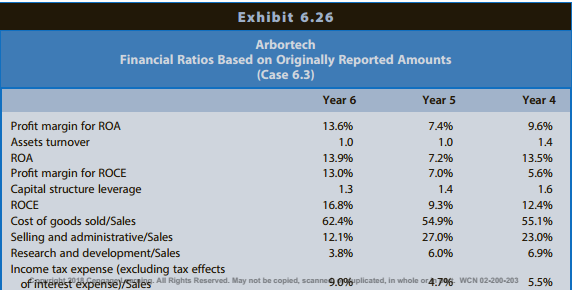

Exhibits 6.23 to 6.25 present Arbortech’s financial statements for the fiscal years ended June 30, Year 4, Year 5, and Year 6, based on the amounts originally reported for each year. Exhibit 6.26 presents selected financial statement ratios based on these reported amounts.

Exhibits 6.23:

Exhibits 6.24:

Exhibits 6.25:

Exhibits 6.26:

Financial Statement Irregularities

On February 10, Year 7, after receiving information regarding various accounting and reporting irregularities, the board of directors fired James and relieved the chief financial officer of his duties. The board formed a special committee of outside directors to investigate the purported irregularities, obtaining the assistance of legal counsel and the firm’s independent accountants. On February 21, Year 7, the New York Stock Exchange announced the suspension of trading in the firm’s common stock. The stock was delisted on April 25, Year 7. On February 14, Year 7, the major Boston bank providing working capital financing notified the firm that the firm had defaulted on its line of credit agreement. Although this bank subsequently extended the line of credit through July 31, Year 7, it increased the interest rate significantly above prime. Arbortech decided to seek a new lender.

The investigation by the board’s special committee revealed the following accounting and

reporting irregularities:

â— Recording of invalid sales transactions: The firm created fictitious purchase orders from regular customers using purchase order forms from legitimate purchase transactions. The firm then purportedly shipped empty PC card housings to these customers at bogus addresses. James apparently paid the accounts receivable underlying these sales with his personal funds.

â— Recording of revenues from bill and hold transactions: The firm kept its books open beyond June 30 each year and recorded as sales of each year products that were shipped in July and should have been recorded as revenues of the next fiscal year.

â— Manipulation of physical counts of inventory balances and inclusion of empty PC card housings in finished goods inventories.

â— Failure to write down inventories adequately for product obsolescence.

â— Inclusion of certain costs in property, plant, and equipment that the firm should have expensed in the period incurred.

â— Inclusion in advances to other technology companies of amounts that represented prepaid license fees. The firm should have amortized these fees over the license period. n Failure to provide adequately for uncollectible amounts related to advances to other technology companies.

◠Failure to write down or write off investments in other technology companies when their market value was less than the cost of the investment……

Transcribed Image Text:

Exhibit 6.23 Arbortech Balance Sheets as Originally Reported (amounts in thousands) (Case 6.3) Year 6 Year 5 Year 4 Year 3 ASSETS Cash $ 6,182 $ 970 $ 981 Marketable securities 4,932 - Accounts receivable 12,592 3,932 1,662 730 Inventories 18,229 8,609 3,371 2,257 234 Other current assets 6,256 1,932 306 Total current assets $48,191 $15,443 $6,320 $3,221 Investments in securities 2,472 Property, plant, and equipment, net 4,698 1,323 669 208 Other assets 421 1,433 601 666 Total Assets $55,782 $18,199 $7,590 $4,095 LIABILITIES AND SHAREHOLDERS' EQUITY $ 3,494 $ 3,571 $ 616 Accounts payable Notes payable Current portion of long-term debt $1,590 4,684 1,153 980 336 103 Other current liabilities 614 765 516 457 Total current liabilities $ 9,128 $ 5,592 $1,132 $3,027 Exhibit 6.23 (Continued) Long-term debt Deferred tax liability 367 162 242 $ 9,737 39 24 Total Liabilities $ 5,754 $1,171 $3,051 Common stock 165 %24 110 $ 90 $ 60 Additional paid-in capital Retained earnings Total Shareholders' EQUITY Total Liabilities and Shareholders' EQUITY 38,802 10,159 2,176 5,027 146 7,078 1,302 838 $46,045 $12,445 $6,419 $1,044 $55,782 $18,199 $7,590 $4,095 Exhibit 6.24 Arbortech Income Statements as Originally Reported (amounts in thousands) (Case 6.3) Year 6 Year 5 Year 4 Sales $ 37,848 $12,445 $ 8,213 Other revenues 353 10 9 Cost of goods sold Selling and administrative Research and development (23,636) (4,591) (1,434) (370) (3,268) $ 4,902 (6,833) (3,366) (752) (74) (4,523) (1,889) (567) (495)* (284) $ 464 Interest Income taxes (556) net Income 874 "Includes the cost of factoring receivables and interest on bridge financing obtained and repaid during the year. Exhibit 6.25 Arbortech Statements of Cash Flows as Originally Reported (amounts in thousands) (Case 6.3) Year 6 Year 5 Year 4 OPERATIONS net income $ 4,902 $ 874 $ 464 Depreciation 645 337 193 Other addbacks and subtractions, net Working capital provided by operations 219 gyright 2018 Cqngage Learning. All Rights Reserved. May not byco anned, or duplic, iole or in part. WGrozo203 $ 876 1,159 (5) S6,706 $ 1,206 Exhibit 6.25 (Continued) (Increase) Decrease in accounts receivables (Increase) Decrease in inventories (Increase) Decrease in other current assets Increase (Decrease) in accounts payable Increase (Decrease) in other current liabilities Cash Flow from Operations (8,940) (2,433) (5,238) (2,406) 2,955 (981) (1,115) (71) (974) (9,620) (836) (76) (152) 251 87 S(12,918) $(5,665) $(2,178) INVESTING $ 3,981 (3,899) (11,186) Sale of investments Acquisition of fixed assets Acquisitions of investments Other investing transactions Cash Flow from Investing (862) (525) (2,800) S(13,904) $ (862) $ (525) FINANCING $ 1,153 $ 550 Increase in short-term borrowing Increase in long-term borrowing $ 3,531 691 320 Increase in common stock 28,064 5,099 4,663 Decrease in short-term borrowing Decrease in long-term borrowing Cash Flow from Financing (1,529) (252) $ 32,034 $ 5,212 (56) $ 6,516 $ (11) $ 3,684 net Change in Cash Cash-Beginning of year $ 981 970 981 Cash-End of Year $ 6,182 $970 $ 981 Exhibit 6.26 Arbortech Financial Ratios Based on Originally Reported Amounts (Case 6.3) Year 6 Year 5 Year 4 Profit margin for ROA 13.6% 7.4% 9.6% Assets turnover 1.0 1.0 1.4 ROA 13.9% 7.2% 13.5% Profit margin for ROCE Capital structure leverage 13.0% 7.0% 5.6% 1.3 1.4 1.6 ROCE 16.8% 9.3% 12.4% Cost of goods sold/Sales Selling and administrative/Sales Research and development/Sales Income tax expense (excluding tax effects of interest expense)/Sales All Rights Reserved. May not be copled, scanne9.0%plicated, in whole or4:7% WCN 02-200-203 5.5% 62.4% 54.9% 55.1% 12.1% 27.0% 23.0% 3.8% 6.0% 6.9% Exhibit 6.26 (Continued) Accounts receivable turnover 4.6 4.4 6.9 Inventory turnover Fixed assets turnover 1.8 1.1 1.6 12.6 12.5 18.7 Current ratio 5.3 2.8 5.6 Quick ratio 2.6 0.9 2.3 Days accounts payable Operating cash flow to current liabilities ratio Long-term debt to long-term capital ratio 39 63 71 (1.755) (1.685) (1.047) 0.008 0.013 Liabilities to assets ratio 0.175 0.316 0.154 (1.636) Operating cash flow to total liabilities ratio Interest coverage ratio (1.668) (1.032) 23.1 20.3 2.5

> On December 31, 2017, Pace Co. paid $3,000,000 to Sanders Corp. shareholders to acquire 100% of the net assets of Sanders Corp. Pace Co. also agreed to pay former Sanders shareholders $200,000 in cash if certain earnings projections were achieved over th

> Ormond Co. acquired all of the outstanding common stock of Daytona Co. on January 1, 2017. Ormond Co. gave shares of its common stock with a fair value of $312 million in exchange for 100% of the Daytona Co. common stock. Daytona Co. will remain a legall

> Exhibit 3.32 presents a statement of cash flows for Walmart for fiscal 2015, 2014, and 2013. This statement matches the Walmart statement of cash flows in Appendix A, and is an expanded version of the statement of cash flows for Walmart shown in Exhibit

> Lexington Corporation acquired all of the outstanding common stock of Chalfont, Inc., on January 1, 2016. Lexington gave shares of its no par common stock with a market value of $504 million in exchange for the Chalfont common stock. Chalfont will remain

> Bed and Breakfast (B&B), an Italian company operating in the Tuscany region, follows IFRS and has made the choice to re measure long-lived assets at fair value. B&B purchased land in 2016 for E150,000. At December 31 of the next four years, the land is w

> Alpha Computer Systems (ACS) designs, manufactures, sells, and services networked computer systems; associated peripheral equipment; and related network, communications, and software products. Exhibit 8.32 presents geographic segment data. ACS conducts s

> Exhibit 8.21 presents selected financial statement data for three chemical companies: Monsanto Company, Olin Corporation, and NewMarket Corporation. (NewMarket was formed from a merger of Ethyl Corporation and Afton Chemical Corporation.) Exhibit 8.21:

> Part A. Floral Delivery, Inc. (FD) acquired a fleet of vans on January 1, 2017, by issuing a $500,000, four-year, 4% fixed rate note, with interest payable annually on December 3. FD has the option to repay the note prior to maturity at the note’s fair v

> Exhibit 6.18 presents selected financial statement data for Enron Corporation as originally reported for 1997, 1998, 1999, and 2000. In 2001, Enron restated its financial statements for earlier years because it reported several items beyond the limits of

> Sunbeam Corporation manufactures and sells a variety of small household appliances, including toasters, food processors, and waffle grills. Exhibit 6.17 presents a statement of cash flows for Sunbeam for Year 5, Year 6, and Year 7. After experiencing dec

> Intel Corporation’s consolidated income statement appears in Exhibit 6.16. Note 15, which follows, explains the source of the restructuring charges, the breakdown of the charges into employee-related costs and asset impairments, and th

> Vulcan Materials Company, a member of the S&P 500 Index, is the nation’s largest producer of construction aggregates, a major producer of asphalt mix and concrete, and a leading producer of cement in Florida. Exhibit 6.15 presents V

> Henry Company is a marketer of branded foods to retail and foodservice channels. Exhibit 6.14 presents Henry’s income statements for Year 10, Year 11, and Year 12. Exhibit 6.14: Notes to the financial statements reveal the following

> Exhibits 1.19–1.21 of Integrative Case 1.1 (Chapter 1) present the financial statements for Walmart for 2012–2015. In addition, the website for this text contains Walmart’s December 31, 2015, Form 10-

> Recent years have witnessed some of the most significant accounting scandals in history. For each scandal listed in Exhibit 6.13, identify how balance sheet quality and earnings quality were impaired. Exhibit 6.13: Exhibit 6.13 Accounting Scandals

> Exhibit 5.23 presents selected financial data for The Tribune Company and The Washington Post Company for fiscal 2006 and 2007. The Washington Post Company is an education and media company. It owns, among others, Kaplan, Inc.; Cable ONE Inc.; Newsweek m

> Exhibit 5.22 presents selected financial data for ABC Auto and XYZ Comics for fiscal Year 5 and Year 6. ABC Auto manufactures automobile components that it sells to automobile manufacturers. Competitive conditions in the automobile industry in recent yea

> Exhibit 5.21 presents selected financial data for Best Buy Co., Inc., and Circuit City Stores, Inc., for fiscal 2008 and 2007. Best Buy and Circuit City operate as specialty retailers offering a wide range of consumer electronics, service contracts, prod

> Sun Microsystems, Inc., develops, manufactures, and sells computers for network systems. Exhibit 5.20 presents selected financial data for Sun Microsystems for each of the five years ending June 30, Year 1, to June 30, Year 5. The company did not go bank

> VF Corporation is an apparel company that owns recognizable brands like Timberland, Vans, Reef, and 7 For All Mankind. Exhibit 5.18 and 5.19 present balance sheets and income statements, respectively, for Year 1 and Year 2. (VF Corporation previously had

> Delta Air Lines, Inc., is one of the largest airlines in the United States. It has operated on the verge of bankruptcy for several years. Exhibit 5.17 presents selected financial data for Delta Air Lines for each of the five years ending December 31, 200

> Exhibit 5.16 presents risk ratios for Coca-Cola for Year 1 through Year 3. Exhibit 5.16: REQUIRED: a. Assess the changes in the short-term liquidity risk of Coca-Cola between Year 1 and Year 3. b. Assess the changes in the long-term solvency risk of C

> Refer to the financial statement data for Abercrombie & Fitch in Problem 4.25 in Chapter 4. Exhibit 5.15 presents risk ratios for Abercrombie & Fitch for fiscal Year 3 and Year 4. Financial statement in 4.25: Exhibit 5.15: REQUIRED: a. Comp

> Exhibit 5.24 presents balance sheets for Year 2 and Year 3 for Whole Foods Market, Inc.; Exhibit 5.25 presents income statements for Year 1 through Year 3. Exhibit 5.24: Exhibit 5.25: REQUIRED: a. For Year 3, prepare the standard decomposition of RO

> Nike, Inc.’s principal business activity involves the design, development, and worldwide marketing of athletic footwear, apparel, equipment, accessories, and services for serious and recreational athletes. Nike boasts that it is the largest seller of ath

> Refer to the financial statement data for Hasbro in Problem 4.24 in Chapter 4. Exhibit 5.14 presents risk ratios for Hasbro for Year 2 and Year 3. Financial statement in 4.24: Exhibit 5.14: REQUIRED: a. Calculate these ratios for Year 4. b. Assess t

> Kelly Services (Kelly) places employees at clients’ businesses on a temporary basis. It segments its services into (1) commercial, (2) professional and technical, and (3) international. Kelly recognizes revenues for the amount bille

> Selected data for The Hershey Company for Year 1 through Year 3 appear in Exhibit 4.29. Exhibit 4.29: REQUIRED: a. Compute ROA and its decomposition for Year 2 and Year 3. Assume a tax rate of 35%. b. Compute ROCE and its decomposition for Year 2 and

> In Integrative Case 10.1, we projected financial statements for Walmart Stores for Years +1 through +5. The data in Chapter 12 include the actual amounts for 2015 and the projected amounts for Year þ1 to Year þ5 for the income statements, balance sheets,

> In Integrative Case 10.1, we projected financial statements for Walmart Stores, Inc. (Walmart), for Years þ1 through þ5. The data in Chapter 12 include the actual amounts for 2015 and the projected amounts for Year þ1 to Year þ5 for the income statements

> Holmes Corporation is a leading designer and manufacturer of material handling and processing equipment for heavy industry in the United States and abroad. Its sales have more than doubled, and its earnings have increased more than six fold in the past f

> In Integrative Case 10.1, we projected financial statements for Walmart Stores, Inc. (Walmart), for Years þ1 through þ5. In this portion of the Walmart Integrative Case, we use the projected financial statements from Integra

> Since the early 1990s, woodstove sales have declined from 1,200,000 units per year to approximately 100,000 units per year. The decline has occurred because of (1) stringent new federal EPA regulations, which set maximum limits on stove emissions beginn

> Walmart Stores, Inc. (Walmart) is the largest retailing firm in the world. Building on a base of discount stores, Walmart has expanded into warehouse clubs and Supercenters, which sell traditional discount store items and grocery products. Exhibits 10.10

> Integrative Case 10.1 involves projecting financial statements for Walmart for Years þ1 through þ5. The following data for Walmart include the actual amounts for 2015 and the projected amounts for Years þ1 thr

> A sales-based ranking of software companies provided by Yahoo! Finance on November 5, 2008, places Oracle Corporation third behind sales leaders Microsoft Corporation and IBM Software. Typical of high-tech companies in the software industry, Oracle Corpo

> In its December 31, 2008, Consolidated Financial Statements, The Cola-Cola Company (Coca-Cola) reports a substantial shift in its net pension liability ($1,328 million) relative to December 31, 2007 ($85 million). REQUIRED: a. Given a portion of Coca-Co

> Exhibits 1.26–1.28 of Integrative Case 1.1 (Chapter 1) present the financial statements for Walmart for 2012–2015. In addition, the website for this text contains Walmart’s December 31, 2015, Form 10-

> In August 2009, The Walt Disney Company announced that it would acquire Marvel Entertainment, Inc., in a $4 billion cash and common stock deal. On a per-share basis, the consideration given by Disney to Marvel shareholders represents a 29% premium over M

> Walmart makes significant investments in operating capacity, primarily via investments in property, plant, and equipment, but also via investments in wholly and partially owned subsidiaries. Walmart also has significant non-U.S. operations in its Walmart

> The first decade of the 21st century witnessed a flurry of losses, bankruptcies, acquisitions, and strategic partnerships in the airline industry. The heavily levered firms in the industry are particularly susceptible to increases in fuel prices, economi

> It is common practice for retail outlets to lease their store locations and distribution centers. Walmart is no exception. Note 11 to Walmart’s consolidated financial statements for the fiscal year ending January 31, 2016 (found online at the text websit

> Assume Boeing sold a 767 aircraft to American Airlines on January 1, 2016. The sales agreement required American Airlines to pay $10 million immediately and $10 million on December 31 of each year for 20 years, beginning on December 31, 2016. Boeing and

> Explain the implications of a value to-book ratio that is greater than the market-to-book ratio. Explain the implications of a value to-book ratio that is less than the market-to-book ratio.

> Using the evidence presented in Exhibit 14.8, describe the extent to which the market is efficient with respect to quarterly earnings surprises during the 60 trading days prior to quarterly earnings announcements. Using the evidence presented in Exhibit

> Identify three economic factors that will drive a firm’s value-to-book ratio to be higher than that of other firms in the same industry. Identify three accounting factors that will drive a firm’s value-to-book ratio to be higher than that of other firms

> Explain the implications of a value to-book ratio that is exactly equal to 1. Compare the implications of a value-to-book ratio that is greater than 1 to those of a value-to-book ratio that is less than 1.

> Explain the theory behind the residual income valuation approach. Why is residual income value relevant to common equity shareholders?

> Explain residual income. How is it measured? What does residual income represent?

> Conceptually, why should you expect a valuation based on dividends, a valuation based on the free cash flows for common equity shareholders, and a valuation based on residual income to yield equivalent value estimates for a given firm?

> Explain the theory behind the free-cash-flows valuation approaches. Why are free cash flows value-relevant to common equity shareholders when they are not cash flows to those shareholders but rather are cash flows into the firm?

> The chapter describes how firms must use flexible financial accounts to maintain equality between assets and claims on assets from liabilities and equities. Chapter 1 describes how some firms progress through different life-cycle stages—from introduction

> Use the following hypothetical data for Walgreens in 2014 and 2015 to project revenues, cost of goods sold, and inventory for Year þ1. Assume that Walgreens’s Year þ1 revenue growth rate, gross profit margi

> The chapter describes how the dividends-based valuation approach measures dividends to encompass various transactions between the firm and the common shareholders. What transactions should you include in measuring dividends for the purposes of implementi

> The chapter asserts that dividends are value relevant even though the firm’s dividend policy is irrelevant. How can that be true? What is the key assumption in the theory of dividend policy irrelevance?

> Why is the dividends based valuation approach applicable to firms that do not pay periodic (quarterly or annual) dividends?

> Explain why analysts and investors use risk adjusted expected rates of return as discount rates in valuation. Why do investors expect rates of return to increase with risk?

> The notes to a firm’s financial statements reveal that the obligations for postretirement health care benefits at the end of 2017 total $2.1 billion. The fair value of plan assets for these benefits at the end of 2017 is reported at zero, with an unrecog

> Given the following information, compute December 31, 2017, projected benefit obligation (PBO) and fair market value (FMV) of plan assets for Lee Company. What amount of asset or liability will be reported on the balance sheet at December 31, 2017? Prio

> Citigroup Inc. (Citi) is a leading global financial services company with over 200 million customer accounts and operations in more than 140 countries. Its operating units Citicorp and Citi Holdings provide a broad range of financial products and service

> HeavyEQ produces large conveyor belt systems for heavy manufacturing. HeavyEQ signs a $2 million fixed-price contract under which it makes three promises: ● Install a conveyor belt system: fair value $1.6 million ● Service the system over a five-year per

> Bookman Co. develops digital accounting systems and provides accounting-related consulting services. a. On January 1, 2017, Bookman signs a contract with Brock Florists to install a system and provide consulting services over a two-year period ending in

> Financial reporting classifies derivatives as (a) speculative investments, (b) fair value hedges, or (c) cash flow hedges. However, firms revalue all derivatives to market value each period regardless of the firm’s reason for acquiring the derivatives

> New lease standards become effective January 1, 2019. These standards affect the accounting for operating leases. Assume Swift Company acquires a machine with a fair value of $100,000 on January 1 of Year 1 by signing a five-year lease. Swift must make p

> Assume that Circuit City owes Synovus Bank $1,000,000 on a four-year, 7% note originally issued at par. After one year of making scheduled payments, Circuit City faces financial difficulty. At the end of the second year, Circuit City owes Synovus $1,000,

> Assume that on December 31, 2017, The Coca-Cola Company borrows money from a consortium of banks by issuing a $900 million promissory note. The note matures in four years on December 31, 2021, and pays 3% interest once a year on December 31. The consorti

> Nestle ´ Group, a multinational food products firm based in Switzerland, recently issued its financial statements. The auditor’s opinion attached to the financial statements stated the following: ‘‘In our opinion, the financial statements for the year en

> Checkpoint Systems, a leading provider of source tagging, handheld labeling systems, retail merchandising systems, and bar-code labeling systems, stated the following in a press release: GAAP reported net loss for the fourth quarter of 2004 was $29.3 mil

> Rock of Ages, Inc., a large North American integrated granite quarrier, manufacturer, and retailer of finished granite memorials, reported a net loss for 2004 of $3.2 million. In 2004, the firm reported a pretax litigation settlement loss of $6.5 million

> Valero Energy, a petroleum company, reported net income (amounts in millions) of $1,803.8 on revenues of $54,618.6 for Year 4. Interest expense totaled $359.7, and preferred dividends totaled $12.5. Average total assets for Year 4 were $17,527.9. The inc

> Exhibits 1.26–1.28 of Integrative Case 1.1 (Chapter 1) present the financial statements for Walmart for 2012 to 2015. In addition, the website for this text contains Walmart’s December 31, 2015, Form 10-K. You should r

> Firms often provide supplemental disclosures that report and discuss income figures that do not necessarily equal bottom-line net income from the income statement. For example, in Twitter’s initial public offering filings with the SEC, the company report

> iRobot designs and manufactures robots for consumer, commercial, and military use. For the fiscal year ended January 2, 2016, the company reported the following on its balance sheet and income statement (amounts in thousands): ● Accounts receivable, net

> ‘‘The ordering of the three sections of the statement of cash flows is ‘backwards’ for start-up firms, but it is more appropriate for businesses once they are up and running.’’ Explain.

> The chapter demonstrates how to prepare a statement of cash flows from information on the balance sheet and income statement. If this is possible, why are managers required to provide a statement of cash flows?

> A firm’s income tax return shows income taxes for 2017 of $35,000. The firm reports deferred tax assets before any valuation allowance of $24,600 at the beginning of 2017 and $27,200 at the end of 2017. It reports deferred tax liabilities of $18,900 at t

> A firm’s income tax return shows $50,000 of income taxes owed for 2017. For financial reporting, the firm reports deferred tax assets of $42,900 at the beginning of 2017 and $38,700 at the end of 2017. It reports deferred tax liabilities of $28,600 at th

> Apply the economic attributes framework discussed in the chapter to the specialty retailing apparel industry, which includes such firms as Gap, Limited Brands, and Abercrombie & Fitch.

> Aer Lingus is an international airline based in Ireland. Exhibit 3.24 provides the statement of cash flows for Year 1 and Year 2, which includes a footnote from the financial statements. Year 2 was characterized by weakening consumer demand for air trave

> The Apollo Group is one of the largest providers of private education and runs numerous programs and services, including the University of Phoenix. Exhibit 3.23 provides statements of cash flows for 2010 through 2012. REQUIRED: Discuss the relations bet

> Montgomery Ward operates a retail department store chain. It filed for bankruptcy during the first quarter of Year 12. Exhibit 3.22 presents a statement of cash flows for Montgomery Ward for Year 7 to Year 11. Exhibit 3.22: The firm acquired Lechmere,

> Douglas C. Mather, founder, chair, and chief executive of Fly-by-Night International Group (FBN), lived the fast-paced, risk-seeking life that he tried to inject into his company. Flying the company’s Learjets, he logged 28 world speed

> The first case at the end of this chapter and numerous subsequent chapters is a series of integrative cases involving Wal-Mart Stores, Inc. (Walmart). The series of cases applies the concepts and analytical tools discussed in each chapter to Walmart&acir

> Jeff, a single individual, receives $5,000 interest income from Treasury bills and $18,000 in Social Security benefits. What is Jeff’s gross income?

> Julie wins $15 million in the lottery payable over 30 years. In years 1 through 4, she receives annual installments of $500,000. At the beginning of year 5, Julie sells her right to receive the remaining 26 payments to a third party for a lump-sum paymen

> The Board of Directors of CYZ Corporation votes to issue two shares of stock for each share held as a stock dividend to shareholders. Just prior to the dividend, Cheryl owns 100 shares of CYZ Corporation stock that she purchased for $10 per share. She re

> Carl paid $40,000 to the City of Hollywood for general revenue bonds. During the current year, he received $2,300 interest income from the bonds. Market interest rates drop, causing the value of the bonds to increase so Carl sells the bonds for $43,000.

> Jose (SSN 150-45-6789) and Rosanna (SSN 123-45-7890) Martinez are a married couple who reside at 1234 University Drive in Coral Gables, FL 33146. They have two children: Carmen, age 19 (SSN 234-65-4321), and Greg, age 10 (SSN 234-65-5432). Carmen is a fu

> Janice Morgan is 17 and in her senior year of high school. She lives with her parents at 7829 Dowry Lane, Boston, MA 02112, and they are her primary source of support and claim her as a dependent on their tax return. She is covered under their health ins

> Go to the IRS Web site (www.irs.gov) and print Form 1040 and Schedule A. Using the information in problem 70, complete these forms to the extent possible.

> George owns 1,000 shares of ABC common stock and 3,000 shares of Brightstar mutual fund. George elects to participate in Brightstar’s dividend reinvestment plan, reinvesting his annual dividends and capital gains distributions in additional Brightstar sh

> Go to the IRS Web site (www.irs.gov) and print Form 1040 and Schedule A. Using the information in problem 69, complete these forms to the extent possible.

> In January, Susan’s employer transferred her from Chicago to Houston (where she continues to work for the remainder of the year). Her expenses were: Transportation for household goods………….$2,300 Airfare from Chicago to Houston……………………200 Pre-move house-h

> Go to the IRS Web site (www.irs.gov) and print Schedule A: Itemized Deductions. Using the following information, complete this form for Simon and Ellen, both age 48 and married filing jointly, who have adjusted gross income of $60,000. They paid the foll

> Go to www.irs.gov (the IRS Web site) and click on Careers under Work at IRS. Look under Resources, then under Job Descriptions, and finally look under Accounting, Budget & Finance to learn more about Internal Revenue Agent positions. a. If you are a rec

> Go to the IRS Web site (www.irs.gov). Print the first page of Form 1040 and compute Pierre Lappin’s adjusted gross income by entering the following information: $60,000 salary, $5,000 qualified dividend income, $3,000 interest income from corporate bonds

> Go to the IRS Web site (www.irs.gov) and print Form 2106: Employee Business Expenses. Use the following information to complete this form. Carl is an employee of Intelligent Devices, Inc. in San Jose. In a typical week, Carl spends the majority of his

> Jordan (SSN 150-66-7788) and Diana (SSN 15067-4321) Diego are a married couple who reside at 111 Coral Drive in Miami, FL 33156. They have one dependent daughter, Emily (SSN 155-88-4321), age 18, who lives at home. Jordan is a manager at Big Box Corpor

> Go to the IRS Web site (www.irs.gov) and print Schedule C: Profit or Loss for Business (Sole Proprietorship), Schedule SE: Self-Employment Tax, and Form 8829: Expenses for Business Use of Your Home. Use the information in problem 47 to complete these for

> Go to the IRS Web site (www.irs.gov) and print the page of Form 1120: U.S. Corporate Income Tax Return that includes Schedule M-1. Use the information in example 6.42 to complete Schedule M-1.