Question: Choose the best answer. 1. Under GASB

Choose the best answer.

1. Under GASB standards, which of the following would be considered an example of an intangible asset?

a. A lake located on city property.

b. Water rights associated with the springs that supply the water to the lake.

c. The city’s irrigation system, which uses water from the lake.

d. None of the above would be considered an intangible asset.

2. Two new copiers were purchased for use by the city clerk’s office using General Fund resources. The copiers cost $15,000 each; the city’s capitalization threshold is $5,000. Which of the following entries would be required to completely record this transaction?

3. Maxim County just completed construction of a new town hall to be used for its governmental offices. The employees have moved in and the new building is officially in use. The county used a capital projects fund to account for the construction of the building, and the building came in under budget. There is a fund balance of $12,000. The county should:

a. Transfer the remaining funds to the General Fund to pay operating expenses.

b. Transfer the remaining funds to the debt service fund which will be handling the long-term debt incurred for the construction of the building.

c. Return the excess to the source of the restricted funding.

d. All of the above may be appropriate ways to treat the fund balance.

4. A capital projects fund would probably not be used for which of the following assets?

a. Construction and installation of new shelving in the mayor’s office.

b. Financing and construction of three new fire substations.

c. Purchase and installation of an entity-wide integrated computer system (such as SAP).

d. Replacing a bridge.

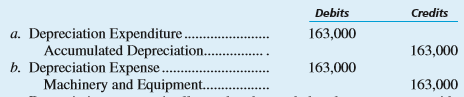

5. Machinery and equipment depreciation expense for general capital assets totaled $163,000 for the reporting period. Which of the following correctly defines the recording of depreciation for general capital assets?

c. Depreciation expense is allocated and recorded at the government-wide level with a debit to the functions or programs of government and a credit to accumulated depreciation.

d. Since depreciation does not involve the use of financial resources it is not necessary for the government to record it at the fund level or government-wide level.

6. Which of the following is a correct statement regarding the use of the modified approach for accounting for eligible infrastructure assets?

a. Depreciation on eligible infrastructure assets need not be recorded if the assets are being maintained at or above the established condition level.

b. Depreciation on eligible infrastructure assets must still be recorded for informational purposes only.

c. The government must document that it is maintaining eligible infrastructure assets at the condition level prescribed by the GASB.

d. All of the above are correct statements.

7. The City of Deauville entered into a service concession arrangement (SCA) with Water Wonders, Inc. to operate the city pool for the next 20 years. Water Wonders has agreed to pay the city $3,000,000 up front as a part of this agreement. According to the agreement, Water Wonders will be responsible for operating the pool, and the city will continue to be responsible for costs related to maintaining it. In addition, Water Wonders has the right to collect fees from the public for their use of the pool, although the rates are subject to approval by the city. The city should:

a. Remove the cost of the pool and the related accumulated depreciation from its records because it has effectively transferred the asset to Water Wonders.

b. Record the receipt of the cash payment, a liability for the cost of required future maintenance, and a deferred inflow of resources for the difference between the cash payment and the liability.

c. Record the payment as a cash receipt and as another financing source for the General Fund. d. Set up a proprietary fund to record all transactions related to the SCA.

8. Callaway County issued $10,000,000 in bonds at 101 for the purpose of constructing a new County Recreation Center. State law requires that any premium on bond issues be deposited directly in a debt service fund for eventual repayment of bond principal. The journal entry to record issuance of the bonds will require a (an):

a. Credit to bonds Payable in the capital projects fund.

b. Credit to Other Financing Sources—Proceeds of bonds in the capital projects fund.

c. Credit to Other Financing Sources—Premium on bonds in the debt service fund.

d. Both b and c are correct.

9. Centerville enters into a capital lease for new copiers in all its city hall offices. In the General Fund, it should report:

a. Equipment balances equal to the lease payments made during the year.

b. Capital expenditures equal to the lease payments made during the year.

c. Equipment balances equal to the capitalizable cost of the fixed assets regardless of the amount of lease payments made during the year.

d. Capital expenditures equal to the capitalizable cost of the fixed asset regardless of the amount of lease payments made during the year.

10. The following balances are included in the subsidiary records of Sinclair:

Town hall building ............................................................. $5,000,000

Town pool (supported by user fees) ..................................... 1,000,000

Town pool maintenance equipment .......................................... 25,000

Police cars .................................................................................. 200,000

Equipment .................................................................................... 75,000

Office supplies ............................................................................... 10,000

What is the total amount of general capital assets held by the town?

a. $5,275,000.

b. $5,285,000.

c. $6,275,000.

d. $6,285,000.

Transcribed Image Text:

> Following is a list of fund names and descriptions from comprehensive annual financial reports (CAFRs). Required: Indicate which of the following are fiduciary funds. If not a fiduciary fund, identify which type of fund should be used to account for th

> Residents of Green Acres, a gated community located in the City of Foothills, voted to form a local improvement district to fund the construction of a neighborhood park. The city agreed to administer the bonded debt; however, residents of Green Acres a

> The county collector of Suncoast County is responsible for collecting all property taxes levied by funds and governments within the boundaries of the county. To reimburse the county for estimated administrative expenses of operating the tax agency fund,

> Bluff County’s schedule of changes in net pension liability and related ratios is shown below. Required: Compute the missing amounts.

> Inglis City had a beginning cash balance in its enterprise fund of $895,635. During 2017, the following transactions occurred: 1. Interest received on investments totaled $42,400. 2. The city acquired additional equity investments totaling $75,000. 3. A

> Following is the June 30, 2017, statement of net position for the City of Bay Lake Water Utility Fund. Required: a. For fiscal year 2017, prepare general journal entries for the Water Utility Fund using the following information. (1) The amount in the

> The Town of Elizabeth operates the old train station as an enterprise fund. The train station is on the national register of historic buildings. Since the town has held the building for such a long time, the Central Station Fund has no long-term debt. Th

> During 2017, the Town of Falmouth had a number of transactions that affected net position of its town skating rink, which is operated as an enterprise fund. You are provided with the following information for 2017 1. The beginning net position balances a

> The City of Saltwater Beach established an enterprise fund in 2015 to construct and operate Tribute Aquatic Center, a public swimming pool. The pool was completed and began operations in 2016. All costs, including repayment of debt, are to be paid by use

> GASB Concepts Statement No. 1, “Objectives of Financial Reporting,” states that “Accountability is the cornerstone of all financial reporting in government.” FASB Statements of Financial Accounting Concepts Statement No. 8, “Conceptual Framework for Fina

> The City of Ashville operates an internal service fund to provide garage space and repairs for all city-owned and-operated vehicles. The Central Garage Fund was established by a contribution of $300,000 from the General Fund on July 1, 2017, at which tim

> Washington City created an Information Technology department in 2013 to centralize information technology (IT) functions for the city. The goal of the department was to reduce costs, avoid duplication of efforts, and provide up-to-date technology to all

> Brown County operates a solid waste landfill for the citizens of the county. The following events occurred during the county’s fiscal year ended September 30, 2017. 1. The county paid interest costs of $6,869,000; of this amount, $214,000 was required to

> In July 1, 2016, the first day of its 2017 fiscal year, the City of Nevin issued at par $2,000,000 of 6 percent term bonds to construct a new city office building. The bonds mature in five years on July 1, 2021. Interest is payable semiannually on Januar

> As of December 31, 2016, Sandy Beach had $9,500,000 in 4.5 percent serial bonds outstanding. Cash of $509,000 is the debt service fund’s only asset as of December 31, 2016, and there are no liabilities. The serial bonds pay interest semiannually on Janua

> Following is Grant County’s debt service fund pre-closing trial balance for the fiscal year ended June 30, 2017. Required: Using information provided by the trial balance, answer the following. a. Assuming the budget was not amended,

> In preparation for a proposed bond sale, the city manager of the City of Appleton requested that you prepare a statement of legal debt margin and a schedule of direct and overlapping debt for the city as of December 31, 2016. You ascertain that the follo

> In early 2017, McCormick County agreed to acquire a new recreation equipment storage facility under a capital lease agreement. At the inception of the lease, a payment of $750,000 will be made; four additional annual lease payments, each in the amount of

> The City of Amarillo is authorized to issue $8,000,000, 3 percent regular serial bonds in 2017 for the construction of a new exit off the interstate highway within city limits. The bonds mature in equal annual amounts beginning on January 1, 2018, for

> Following are a number of unrelated transactions for the Village of Centerville, some of which affect governmental activities at the government-wide level. None of the transactions has been recorded yet. 1. The General Fund collected and transferred $750

> The City and County of Denver allocates its governmental fund balances among the classifications specified by GASB standards (see Illustration A2-4). Go to Denver’s Web site and locate its CAFR report for the 2013 fiscal year (Hint: Look for the Finance

> Residents from the Town of Mountain View authorized a $5,000,000 renovation to their historic town hall on November 15, 2016. Financing for the project consists of $2,500,000 from a 5 percent serial bond issue, $1,500,000 from a state grant, and $1,000,0

> During FY 2017, the voters of Surprise County approved construction of a $21 million police facility and an $11 million fire station to accommodate the county’s population growth. The construction will be financed by tax-supported bonds in the amount of

> Policymakers in your state have been talking about shifting from a defined benefit pension plan to a defined contribution pension plan or a hybrid alternative for new state employees. You work for a state legislator who asks you to research the pros and

> G ASB standards require that governments report other postemployment benefits offered to employees, which in some cases will be huge. To investigate the extent of the problem, examine the required supplementary information (RSI) of the most recent CAFRs

> Kaui County has operated a popular oceanside municipal golf course for more than 30 years. Local patrons as well as tourists enjoy reasonable rates in a picturesque setting. Ten years ago, the course was quite profitable, so the county created an enterpr

> Use the 2012 CAFR for the City and County of Denver to respond to the following questions. Required: a. Does the City and County of Denver report any internal service funds? If so, identify the internal service funds found in its financial statements an

> Casper County has prepared the following operating statement for its proprietary funds. The county has three enterprise funds and two internal service funds. Required: The statement as presented is not in accordance with GASB standards. Identify the e

> Financial statements for the Building Maintenance Fund, an internal service fund of Coastal City, are reproduced here. No further information about the nature or purposes of this fund is given in the annual report. Required: a. Assuming that the Build

> This case focuses on the analysis of a city’s general obligation debt burden. After examining the accompanying table that shows a city’s general obligation (tax-supported) debt for the last ten fiscal years, answer the

> You are a town council member in the seaside town of Pleasantville. Poor economic conditions and unusually severe weather conditions have affected tourism in the town, leading to significantly reduced sales, income, and hotel resort tax collections. Town

> On November 9, 2011, the chairman of the FASB announced that a standard-setting project intended to improve the financial reporting of not-for-profit organizations had been added to the FASB’s agenda. Examine the Financial Accounting Standards Board’s We

> A tornado damaged a part of the City of Westbrook’s Police Station. Some of the costs related to the damage included the following: 1. The building wiring had to be replaced. Since the wiring was over 20 years old, replacing the wiring allowed the city t

> In preparation for the annual meeting of Barker County, the finance committee was meeting to discuss the financial reports that would be presented to the Board of Commissioners. The committee included a newly elected commissioner, Michelle Backin, who gr

> In this case, local governments receive reimbursements from the state government’s Department of Social Services for expenditures incurred in conducting an array of locally administered programs that benefit troubled teens. The state program provides rei

> Park City experienced unusual volatility of taxable property values over a particular five-year period. For the first three years of this period, the “pre-recession period,” average property values in the city increased by more than 35 percent. Then, alm

> State whether each of the following items should be classified as taxes, licenses and permits, intergovernmental revenues, charges for services, fines and forfeits, or miscellaneous revenue in a governmental fund. a. Sales and use taxes levied by the gov

> How do expenses and expenditures differ?

> Indicate whether each of the following expenditure items should be classified as a function, program, organization unit, activity, character, or object. a. Mayor’s Office. b. Public Safety. c. Residential trash disposal. d. Accident investigation. e. Sal

> Explain the meaning and significance of inter period equity .

> Indicate whether the following revenues should be classified as program revenues or general revenues on the government-wide statement of activities. a. Unrestricted operating grants that can be used at the discretion of the city council. b. Capital grant

> In reading Appendix A of this chapter, you may have been struck by the fact that many governmental accounting information (GAI) software systems appear to be incapable of handling the full reporting requirements of a governmental entity. A 2006 Market Re

> Using GP for general purpose government or SP for special purpose government, identify the following governments by type. a. Stonington Village. b. Lynnford Regional Library District. c. Hillsborough County Consolidated School District. d. Missoula, Mon

> Choose the best answer. 1. Which of the following financial statements is prepared by fiduciary funds? a. Statement of activities. b. Statement of net position. c. Statement of cash flows. d. All of the above. 2. At the government-wide level, where are f

> Choose the best answer. 1. Which of the following is not a fiduciary fund? a. Permanent fund. b. Private-purpose trust fund. c. Investment trust fund. d. Agency fund. 2. Which of the following is an example of a trust fund? a. A fund used to account for

> Utilizing the annual report obtained for Exercise 1–16, follow these instructions: a. Agency Funds. Does the government operate a tax agency fund or participate in a tax agency fund operated by another government? Does the government act as an agent for

> Choose the best answer. 1. Within the government-wide financial statements, the column for Business-type Activities will generally include: a. Internal service funds only. b. Enterprise funds only. c. All internal service fund and enterprise fund transac

> Choose the best answer. 1. Which of the following would not be considered a general long-term liability? a. T he estimated liability to clean up the hazardous waste storage sites of the city’s Public Works Department. b. Capitalized equ

> Section A provides a list of the results of Georgetown’s analysis of its fund balances at its fiscal year end. Section B provides a list of the possible classifications for reporting the items listed in Section A. Section A _____1. A t year end a special

> Choose the best answer. 1. When equipment was purchased with General Fund resources, which of the following accounts would have been debited in the General Fund? a. Expenditures. b. Equipment. c. Encumbrances. d. No entry should be made in the General F

> Choose the best answer. 1. Which of the following best describes the recommended format for the government-wide statement of activities? a. Revenues minus expenses equals change in net position. b. Revenues minus expenditures equals change in net positio

> A s noted in Appendix B to this chapter, most, if not all, state governments require public school districts to report financial and other data to the appropriate state agency, so the state can report standardized school data to the National Center for E

> Choose the best answer. 1. Which of the following statements is true regarding the definition of a fund? a. A fund is a fiscal entity that is designed to provide reporting that demonstrates conformance with finance-related legal and contractual provision

> Examine the CAFR. Utilizing the CAFR obtained for Exercise/Problem 1–15, examine the financial statements included in the financial section and answer the following questions. If the CAFR you have obtained does not conform to GAAP, it i

> How does total pension liability differ from net pension liability?

> Explain the difference between a private-purpose trust and a public-purpose trust. How does the reporting for the two types of trusts differ?

> Compare a defined benefit pension plan with a defined contribution pension plan. If you were an employee, which type of plan would you prefer? Why?

> Explain how the financial reporting of fiduciary funds differs from that of governmental funds.

> Describe the basic activities conducted by a tax agency fund. What are some of the issues that make tax agency fund accounting complex?

> Compare the accounting for pension expenditures in a governmental fund with the accounting for pension expenses at the government-wide level.

> Explain the distinction(s) between agency funds and trust funds. What financial statements are prepared for each?

> What are regulatory accounting principles and how do they relate to enterprise fund accounting?

> The city manager of University City is finalizing the budget proposal that must be submitted to the city council 60 days prior to the July 1 start of the next fiscal year, FY 20X2. An economic recession has significantly r educed the city’s revenues over

> When do GASB standards require inter fund receivables and payables to be reported as Internal Balances?

> What is the accounting treatment if an internal service fund recovers more or less than the costs incurred by the fund?

> What are the three components of net position provided by GASB? Describe how a government assigns amounts to the classifications.

> Although proprietary funds are often compared to for-profit businesses, there are several differences between accounting for proprietary funds and accounting for a for-profit organization. Identify and discuss at least one difference for each of the fund

> Explain the reporting requirements for internal service funds and enterprise funds. Internal service funds and enterprise funds are both proprietary funds, so why do their reporting requirements differ?

> What is meant by “segment information for enterprise funds”? When is the disclosure of segment information required?

> What are the characteristics of a proprietary fund? How do internal service funds and enterprise funds differ?

> What are the GASB requirements for reporting investments held for the purpose of servicing government debt?

> How do term bonds differ from serial bonds? What, if any, impact does this difference have on the entries made to the debt service fund over the life of the bonds?

> Governments are prevented from borrowing unlimited funds through the enforcement of debt limits. Explain the concept of a debt limit. How are debt limits computed? How is the concept of borrowing power or debt margin connected to debt limits?

> Refer to Case 3–11 for instructions about how to obtain the CAFR for a city of your choice. Using that CAFR, go to the required supplementary information (RSI) section, immediately following the notes to the financial statements, and locate the budgetar

> Although the most common type of general long-term liabilities are those arising from financing activities (e.g., bonds, notes, and capital leases), general long-term liabilities can also be created through operating activities. Provide examples of long-

> Explain the financial reporting for special assessment bonds when (a) a government assumes responsibility for debt service should special assessment collections be insufficient, and when (b) the government assumes no responsibility whatsoever.

> What is the purpose of a debt service fund? Does a debt service fund require budgeting? Why or why not?

> How are general long-term liabilities distinguished from other long-term liabilities of the government? How does the financial reporting of general long-term liabilities differ from the financial reporting of other long-term liabilities?

> What two measures help protect a government from failure on a contractor’s part to comply with the terms and specifications of a construction agreement? Describe each measure and its primary purpose.

> Both a capital projects fund general ledger and the governmental activities general ledger at the government-wide level are affected by transactions related to construction of a new capital asset for a government. Describe the major differences in how ac

> If a capital project is incomplete at the end of a fiscal year, what happens to Encumbrances and all operating statement accounts at year-end?

> What is the accounting difference between using the modified approach for infrastructure assets and depreciating infrastructure assets? Under the modified approach, what happens if infrastructure assets are not maintained at or above the established cond

> What are examples of intangible assets held by governments? How are they recorded?

> Compare and contrast the valuation of general capital assets of a government to the valuation of assets of a for-profit entity. What special issues may arise in valuing a government’s assets that generally do not occur in a for-profit company?

> Locate a comprehensive annual financial report (CAFR) using a city’s Web site. Many cities, particularly those with a population greater than 25,000, publish their CAFRs on the city’s official Web site. At the city’s Web site, access a list of the city’s

> What is a service concession arrangement, and why might a government choose to enter into such an arrangement? Provide examples of general capital assets that might be subject to service concession arrangements.

> What are general capital assets? How are they reported in the fund and government-wide financial statements?

> How does a permanent fund differ from public-purpose trusts that are reported in special revenue funds? How does it differ from private-purpose trust funds?

> The computer department of a certain city, a General Fund department, charges other funds for data processing services. At the end of the fiscal year, the General Fund is owed $5,000 by the City Library Fund (a special revenue fund) and $8,000 by the Cit

> Explain why some governments may account for inventories of supplies using the purchases method in the General Fund and the consumption method at the government-wide level? How would the amount reported for expenditures in the General Fund compare with t

> How does accounting in a governmental fund for the purchase of supplies from an outside vendor differ from the purchase of supplies from an internal service fund?

> During a recession citizens and governments see a substantial decline in the value of homes. How might this decline in value impact a government’s gross property tax levy?

> In many cases, property taxes comprise a significant source of revenue and cash receipts for a government. If property tax cash collections typically occur during one or two collection periods, how do governments manage working capital needs?

> When preparing the statement or schedule of revenues, expenditures, and changes in fund balance on the budgetary basis, how are encumbrances outstanding at year end treated if they will be honored in the upcoming year?

> Explain why some transactions for governmental activities at the government wide level are reported differently than transactions for the General Fund. Give some examples of transactions that would be recorded in the general journals of (a) only the Gen

> Following is a description of the basic financial statements extracted from an example city’s management’s discussion and analysis (MD&A). Review the description and respond to the requirements at the end of the case. Government-wide Financial Statements

> Examine the Governmental Accounting Standards Board’s Web site (www.GASB.org) and prepare a brief report about its mission, standard setting process, board composition, and the role of the Governmental Accounting Standards Advisory Council. Can you deter

> Marketers rely heavily on demographics when purchasing media. IMC Perspective 10–1 talks about additional factors that may be important. Discuss some of these factors and why they might impact media usage.

> There is new research that indicates that the number of ads one is exposed to in a day may be much lower than the thousands previously reported. Which numbers do you consider correct and why?

> A number of studies have examined the role that personality and/or other personal characteristics may have on consumers’ media usage. Discuss some of these studies. Do you think that these characteristics may have an impact, or should marketers rely prim