Question: Jack Aerospace Technologies (JAT) researches,

Jack Aerospace Technologies (JAT) researches, designs, manufactures, delivers, and services numerous product part components to the world’s largest aircraft companies. JAT produces approximately 120 aircraft products using numerous processes and many employees. In recent years, JAT’s profitability has suffered, which can be attributed to increased competition, customer dissatisfaction, and regulatory pressures. Noela, president of JAT, called a meeting to consider ways to improve profitability. She labeled the meeting a strategic planning session and invited the following officers: Katerina, environmental manager; Francisca, head of research and development; Misato, vice president of production and quality; Sakari, vice president of finance; and William, marketing vice president.

Noela: “You all have received the quarterly financial reports for the past two years. The trends are negative. We are losing market share, profits are decreasing, and our costs seem to be increasing. We need to take actions to increase sales, reduce costs, or both, and we need to do so as quickly as possible. Given our research strengths, it seems to me that our best bet is to grow revenues by introducing new products with proprietary rights. As far as costs are concerned, we need to improve our performance on that dimension as well. Lower per-unit costs for new and existing products are needed. Any suggestions?â€

Francisca: “For our products, our ability to control costs resides in development—my area—rather than manufacturing. We probably need to pay more attention to product and process design issues if we are to successfully lower costs. Revenues also are affected in this stage. Once we patent a new part or component, the clock begins to tick, and we need to reduce time to market. Significantly, reducing time to market will allow us to generate revenues for a longer period of time than we currently are experiencing. For example, reducing the cycle time spent to convert new ideas into working engineering and other processes would help to improve time to market and also to increase revenues. Finally, we can grow revenues by increasing the volume of new products.â€

Misato: “While there is a lot of merit to the observation that the majority of our cost reduction opportunities reside in product development, significant cost reduction opportunities also involve manufacturing as well. For example, we might be able to reduce our manufacturing cycle time of converting raw materials into finished product. Furthermore, as you know, the Federal Aviation Administration (FAA) and other delegated authorities play a critical role in our business, as they must approve all our aircraft products. After more than a decade in our research lab, we recently received regulatory approval for a number of new state-of-the-art flight-critical engine parts, such as the bearing housings in the turbofan engine of maritime patrol aircrafts that navies use for patrol and search-and-rescue missions. This new manufacturing technology uses additive manufacturing, which often is referred to as 3D printing. Traditionally, many of these parts have been complicated to manufacture, which has made their replacement very costly for customer operators because of the low quantity of orders placed and the need for expensive molds for holding molten metal. However, with 3D printing, we can print such parts more quickly, in smaller quantities, and without the need for expensive tools as components are manufactured using layers of powdered metal fused together with a laser. Finally, for some parts, our new 3D manufacturing technology has drastically reduced our lead time from nearly two years to only two weeks.â€

Francisca: “Given that the FAA must approve all changes in our manufacturing process, we have been reluctant, historically, to engage in process improvement or reengineering. However, given our recent performance and regulatory success involving our new 3D printing manufacturing technologies, I wonder if we shouldn’t reconsider this long-standing policy. We might be able to build on this success by expanding considerably on this line of product offerings. Some of the quality problems we have experienced could be corrected by changing some of our existing processes, and the costs saved might exceed any cost incurred from seeking FAA approval. I think our quality costs likely are significant and represent an opportunity for improvement.â€

Sakari: “Recent groundings of specific aircraft types for which we supply parts also has hurt our earnings. As a result, from a risk perspective, I wonder if broadening our customer base so that our parts and components are used on a greater number of different aircrafts might help reduce our concentration risk and help to limit the drop in sales revenues that usually accompanies specific aircraft groundings.â€

Katerina: “I agree that cost reduction—both in the product development stage and the manufacturing stage—should be a key strategic theme. The environmental area might offer some very good opportunities. A recent Pollution Prevention Act passed by the legislature requires that we monitor and report on the carbon emissions (across different Scope levels) of our products. We also have begun to calculate the costs of generating hazardous substances for each process. This Act was the push we needed to begin developing an environmental cost management system. The results so far indicate that environmental costs are much more than we realized. They are estimated to be in the range of 20 to 25 percent of total operating costs. Environmental costs can be reduced by such things as utilizing lighter yet stronger materials, eliminating the use of hazardous chemicals and other materials in production, advancing product designs that foster more efficient landings, reducing water usage throughout the value chain, and redesigning processes and products so that we can reduce both toxic residue release and carbon emissions. We might be able to have a really positive environmental impact while simultaneously reducing costs if more attention is paid to environmental issues during product development. However, I’m not sure if the financial numbers would support this assertion.â€

William: “I like what I am hearing because I think that it also affects our ability to increase market share and revenues. I know our incentive system focuses primarily on rewarding innovative new product designs with unique performance features. For example, environmental impact is one of our major concerns. Some aviation industry stakeholders increasingly pay particular attention to carbon footprints (and other environmental footprint impacts), and right now we are not competing well. Our environmental image is negative and needs to be improved. I am convinced that doing so will allow us to increase market share. Quality is another important matter. For example, many of our parts are considered “safety-critical†or “flight-critical†by the FAA, which means that they must function properly on every flight. Malfunction or failure of these parts poses major threats to safety and potentially could cause considerable aircraft damage. We have had to recall two batches of products during the past two years due to poor quality, which has hurt our image. Improving the processes to avoid these kinds of problems will save us a lot of grief. Product image and reputation are essential to increasing customer satisfaction and market share.â€

Noela: “Typically, we have tried to improve financial performance by investing more heavily in innovative research and development initiatives in an attempt to increase revenue. However, as mentioned earlier, perhaps it would be prudent to give more attention to cost management. So far, we have some very good suggestions to help achieve these two objectives, but I have some concerns. First, do we have the talent and capabilities to improve quality and environmental performance? Francisca, do your professionals really understand what they need to do to improve process and product designs so that we can see the desired quality and environmental improvements? Also, how can we reduce the cycle time for products and the time to market once patented?â€

Francisca: “Let me answer those questions in order. First, we probably are lacking the understanding on the design issues. We will need to do some training to help our research scientists understand the consequences. We may need to hire additional specialty engineers who are equipped to help us ramp up our 3D design and manufacturing business lines if we decide to move in that direction. Second, we may need to make cost efficiencies, and other cost controls, significant performance measures and reward our people for actions that reduce those measures. Our employees need to align their interests with those of the company. If we can achieve these steps, we should see more profit produced per employee.â€

Noela: “Good. Now, Misato, tell us about production and quality. Do our manufacturing engineers and production workers need help with environmental and quality issues?â€

Misato: “Well, I certainly consider our efforts around inspection to be quality related in nature. A less obvious but potentially important quality-related effort regards our waste production, which occurs both because of quality deficiencies in various facility areas and certain environmental challenges. Without question, training will be needed. Moreover, I really need to hire several quality engineers.â€

Katerina: “I also think that we need an environmental engineer with experience in aerospace manufacturing processes.â€

Noela: “Good. We certainly shouldn’t ignore the necessary infrastructure to bring about the needed changes. Sakari, you have been relatively quiet; what do you think about all this? Do you have any suggestions?â€

Sakari: “Infrastructure is important. If these changes are going to work, timely and accurate information will be needed. It is hard to design products and processes with cost being a significant issue without providing the right kind of cost information. We are in the process of revamping the cost management information system so that it is activity based and we can provide quality and environmental cost information. After listening to the comments made here, I might also suggest that we need to reevaluate our strategic-based control system that it can be used to align the interests of our employees with our strategy. People need to know what is important, that the most critical factors are being measured, and that they are going to be evaluated and rewarded based on those factors. Finally, I would encourage the use of target costing to help manage costs during product development. To help you all understand the importance of good information, I have assembled some activity data relating to two new products (FLI 4HY and FLI 2LW) currently under development. The data are organized into resource, activity, and cost object modules with an accompanying list of activity drivers to facilitate the use of an ABC software package recently acquired by JAT.â€

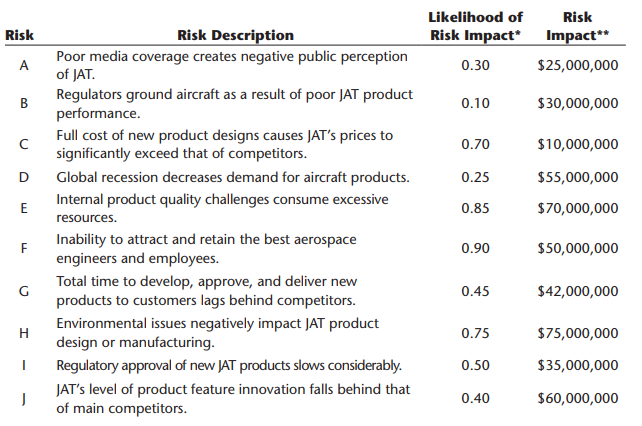

Risk Table

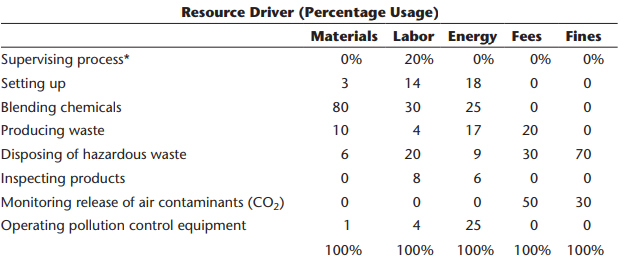

Resource Module (Projected General Ledger Costs of Manufacturing Process Associated with the Two Products)

Materials $20,000,000

Salaries and wages 10,000,000

Energy 5,000,000

License fee (environmental) 2,000,000

Environmental fines 4,000,000

Depreciation; pollution control equipment 2,000,000

Total $43,000,000

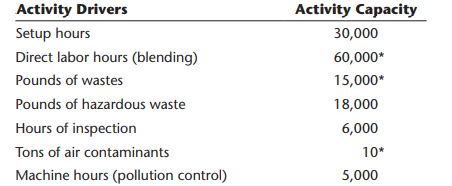

Activity Module

List of Activity Drivers

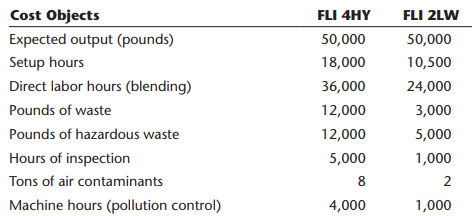

Cost Object Module (Products and Projected Activity Usage)

Required:

1. Use the comments from the executive meeting to evaluate the three elements of JAT’s strategic-based control system, including any recommended changes that would improve the system.

2. Use the data in JAT’s Risk Table to construct a risk plot of JAT’s inherent risks. Based on this inherent risk plot, identify and briefly discuss JAT’s three most important risks.

3. Based on your suggested improvements to JAT’s strategic-based control system (Requirement 1) and the results of your risk plot (Requirement 2), identify strategic objectives and possible quantitative performance measures for each of five perspectives: financial, customer, environmental, process, and learning and growth. Would you recommend the Balanced Scorecard for JAT? Why?

4. Consider the cost of activities (round all answers to three decimal places):

a. Determine the cost of the primary activities (e.g., setting up, blending chemicals, producing waste, disposing of hazardous waste, inspecting products, monitoring release of air contaminants, and operating pollution control equipment) for the proposed new activity-based cost management system. (Note: These costs will be part of the numerator when calculating the activity rates in Requirement 6.)

b. Assign the cost of the secondary activity (supervising) to the primary activities.

5. Classify the primary activities into three categories: environmental, quality, and other (neither quality nor environmental). Did some activities end up in more than one category? Also, are there any notable similarities or differences between the classifications of these primary activities and the results of the inherent risk plot (from Requirement 2)? Briefly explain your responses.

6. Consider the unit costs (round all answers to two decimal places):

a. Determine the cost per unit for the two proposed products (FLI 4HY and FLI 2LW) by calculating primary activity rates and applying costs accordingly.

b. Calculate the environmental cost per unit and the quality cost per unit.

c. What do these unit cost data tell you about the relative desirability of the two products?

d. How do the financial insights provided by these activity-based costs relate to the risk insights provided by the inherent risk plot (in Requirement 2)?

7. Following Sakari’s suggestion, Noela decided to use target costing to help improve new product profitability. Based on analyses by Noela and William, the target prices for 4HY and 2LW are $500 per pound and $350 per pound, respectively. Noela has indicated that any new product should earn a gross profit equal to 20 percent of sales. Based on this information, answer the following items (round all answers to two decimal places):

a. What is the target cost for each product? Given this information, recommend the action that should be taken with respect to offering or not offering the two new products. Briefly explain your recommendation. Also, calculate the impact of your recommendation on JAT’s total profits.

b. Suppose William indicates that unit sales for each product can be increased by 50 percent if the selling price is lowered by 10 percent. Assuming the same target profit

(Noela wants the original target profit dollar amount per pound maintained), calculate the new target cost for each product. Furthermore, assume that Katerina believes that all environmental and quality costs are non-value-added. If all non-value-added costs were eliminated, could these new target costs be met? (Calculate the unit cost at the 50,000 unit level.) Also, calculate the effect on total profits under a scenario where all non-value-added costs are eliminated. (Include in this analysis any possible increase in sales volume.) Based on your scenario analysis, recommend whether JAT should or should not implement this new target cost and eliminate non-value-added costs. Briefly explain your recommendation.

c. After additional consultation with JAT’s general counsel, Katerina now believes that the cost to monitor the release of air contaminants is a value-added cost because it is required by the new Pollution Prevention Act. Recalculate the effect on total profits if the cost to monitor the release of air contaminants is treated as a value-added cost (i.e., not eliminated). Briefly explain how this treatment affects your recommendation (in Requirement 7b).

8. Sakari has decided that utilizing data analytics in responding to the issues raised in the planning meeting would allow for an easier and a quicker response to any subsequent “what-if?†questions and scenarios that might arise from management (e.g., what if particular activity usage or cost inputs changed?). Therefore, to assist Sakari with this endeavor:

a. Use Excel (or some other software tool) to create your inherent risk plot (from Requirement 2).

b. Use Excel (or some other software tool) to create a comprehensive spreadsheet that incorporates the necessary formulas and other cell references to respond to the quantitative requirements.

> Warren’s Sporting Goods Store sells a variety of sporting goods and clothing. In a back room, Warren’s has set up heat transfer equipment to personalize T-shirts for Little League teams. Typically, each team has the name of the individual player put on t

> Lieu Company is a specialty print shop. Usually, printing jobs are priced at standard cost plus 50 percent. Job 631 involved printing 400 wedding invitations with the following standard costs: Direct materials $240 Direct labor 60 Overhead 80 Total $38

> Cherise Ortega, marketing manager for Romer Company, was puzzled by the outcome of two recent bids. The company’s policy was to bid 150 percent of the full manufacturing cost. One job (labeled Job 97-28) had been turned down by a prospe

> Escuha Company produces two type of calculators: scientific and business. Both products pass through two producing departments. The business calculator is by far the most popular. The following data have been gathered for these two products: Required: 1.

> Refer to the data given in Problem 4-34 and suppose that the expected activity costs are reported as follows (all other data remain the same): Other overhead activities: The per unit overhead cost using the 14 activity-based drivers is $110.80 and $77.90

> For Reducir, Inc. Based on a recent internal study, the following information was also gathered and made available. The unit time information was gathered to allow the company to use TDABC. Cycle time was also calculated using historical production data.

> Refer to Brief Exercise 7-3. Now assume that Chekov Company uses the reciprocal method to allocate support department costs. Required: 1. Calculate the allocation ratios (rounded to four significant digits) for the four departments using the reciprocal m

> Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major subassembly for the cylinders in the Cutting and Welding Department. Other parts and the subassembly are then assembled in the Assembly Department. The activitie

> Refer to the data in Problem 4-32. The clinic has identified three types of patients: those with no heart disease, those with mild heart disease, and those with severe heart disease. The following additional data are provided: Required: 1. Using the acti

> The Bienestar Cardiology Clinic has two major activities: diagnostic and treatment. The two activities use four resources: nursing, medical technicians, cardiologists, and equipment. Detailed interviews have provided the work distribution matrix shown be

> Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234. Part #127 produced the highest volume of activity, and for many years it was the only

> Glencoe First National Bank operated for years under the assumption that profitability can be increased by increasing dollar volumes. Historically, First National’s efforts were directed toward increasing total dollars of sales and tota

> Glencoe Medical Clinic operates a cardiology care unit and a maternity care unit. Cara Abadi, the clinic’s administrator, is investigating the charges assigned to cardiology patients. Currently, all cardiology patients are charged the s

> Fisico Company produces exercise bikes. One of its plants produces two versions: a standard model and a deluxe model. The deluxe model has a wider and sturdier base and a variety of electronic gadgets to help the exerciser monitor heartbeat, calories bur

> Primera Company produces two products and uses a predetermined overhead rate to apply overhead. Primera currently applies overhead using a plantwide rate based on direct labor hours. Consideration is being given to the use of departmental overhead rates

> Kimball Company has developed the following cost formulas: Material usage: Ym = $80X; r = 0.95 Labor usage (direct): Yl = $20X; r = 0.96 Overhead activity: Yo = $350,000 + $100X; r = 0.75 Selling activity: Ys = $50,000 + $10X; r = 0.93 Where; X = Direct

> Big Mike’s, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controller’s department, believes that overhead activities and

> Refer to Brief Exercise 7-3. Now assume that Chekov Company uses the sequential method to allocate support department costs. The support departments are ranked in order of highest cost to lowest cost. Required: 1. Calculate the allocation ratios (rounded

> St. Teresa’s Medical Center (STMC) offers a number of specialized medical services, including neuroscience, cardiology, and oncology. STMC’s strong reputation for quality medical care allowed it to branch out into othe

> Rolertyme Company manufactures roller skates. With the exception of the rollers, all parts of the skates are produced internally. Neeta Booth, president of Rolertyme, has decided to make the rollers instead of buying them from external suppliers. The com

> Thames Assurance Company sells a variety of life and health insurance products. Recently, Thames developed a long-term care policy for sale to members of university and college alumni associations. Thames estimated that the sale and service of this type

> Harriman Industries manufactures engines for the aerospace industry. It has completed manufacturing the first unit of the new ZX-9 engine design. Management believes that the 1,000 labor hours required to complete this unit are reasonable and is prepared

> The Lockit Company manufactures door knobs for residential homes and apartments. Lockit is considering the use of simple (single-driver) and multiple regression analyses to forecast annual sales because previous forecasts have been inaccurate. The new sa

> Randy Harris, controller, has been given the charge to implement an advanced cost management system. As part of this process, he needs to identify activity drivers for the activities of the firm. During the past four months, Randy has spent considerable

> Friendly Bank is attempting to determine the cost behavior of its small business lending operations. One of the major activities is the application activity. Two possible activity drivers have been mentioned: application hours (number of hours to complet

> Weber Valley Regional Hospital has collected data on all of its activities for the past 16 months. Data for cardiac nursing care follow: Required: 1. Using the high-low method, calculate the variable rate per hour and the fixed cost for the nursing care

> DeMarco Company is developing a cost formula for its packing activity. Discussion with the workers in the Packing Department has revealed that packing costs are associated with the number of customer orders, the size of the orders, and the relative fragi

> The management of Wheeler Company has decided to develop cost formulas for its major overhead activities. Wheeler uses a highly automated manufacturing process, and power costs are a significant manufacturing cost. Cost analysts have decided that power c

> Chekov Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly. The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of Gene

> Vasani House Company produces numerous fabrics for use in automobile, airplane, and boat seats. For last year, Vasani House reported the following: Last year, Vasani House produced 6,800 units and sold 7,000 units at $250 per unit. Required: 1. Prepare a

> Mason, Durant, and Santos (MDS) is a tax services firm. The firm is located in Oklahoma City and employs 15 professionals and eight staff. The firm does tax work for small businesses and well-to-do individuals. The following data are provided for the las

> Allright Test Design Company creates, produces, and sells Internet-based CPA and CMA review courses for individual use. Davis Webber, head of human resources, is convinced that question development employees must have strong analytical and problem-solvin

> Spencer Company produced 200,000 cases of sports drinks during the past calendar year. Each case of 1-liter bottles sells for $36. Spencer had 2,500 cases of sports drinks in finished goods inventory at the beginning of the year. At the end of the year,

> The actions listed next are associated with either an activity-based operational control system or a traditional operational control system: a. Budgeted costs for the maintenance department are compared with the actual costs of the maintenance department

> The following items are associated with a traditional cost accounting information system, an activity-based cost accounting information system, or both (i.e., some elements are common to the two systems): a. Usage of direct materials b. Direct materials

> Wright Plastic Products is a small company that specialized in the production of plastic dinner plates until several years ago. Although profits for the company had been good, they have been declining in recent years because of increased competition. Man

> Brody Company makes industrial cleaning solvents. Various chemicals, detergent, and water are mixed together and then bottled in 10-gallon drums. Brody provided the following information for last year: Last year, Brody completed 100,000 units. Sales reve

> Foto-Fast Copy Shop provides a variety of photocopying and printing services. On June 5, the owner invested in some computer-aided photography equipment that enables customers to reproduce a picture or illustration, input it digitally into the computer,

> Firenza Company manufactures specialty tools to customer order. Budgeted overhead for the coming year is: Purchasing $40,000 Setups 37,500 Engineering 45,000 Other 40,000 Previously, Sanjay Bhatt, Firenza Company’s controller, had appli

> The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include: Fixed costs (salaries, tools): $64,900 per year Variable costs (supplies): $1.35 per maintenance hour The Assembly and Packaging departments expect to use ma

> During May, the following transactions were completed and reported by Sylvana Company: a . Materials purchased on account, $60,100. b. Materials issued to production to fill job-order requisitions: direct materials, $51,000; indirect materials, $8,950. c

> Lawanna Davis graduated from State U with a major in accounting five years ago. She obtained a position with a well-known professional services firm upon graduation and has become one of their outstanding performers. In the course of her work, she has de

> Garcia Industries produces tool and die machinery for manufacturers. The company expanded vertically in 20x1 by acquiring one of its suppliers of alloy steel plates, Keimer Steel Company. To manage the two separate businesses, the operations of Keimer ar

> Reddy Industries is a vertically integrated firm with several divisions that operate as decentralized profit centers. Reddy’s Systems Division manufactures scientific instruments and uses the products of two of Reddy’s

> For each of the following scenarios, determine whether the specified variable would increase, decrease, or remain the same. Explain your choice. 1. If sales and average operating assets for Kayman Company for Year 2 are identical to their values in Year

> At the end of 20x1, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To

> Carson Wellington, president of Mallory Plastics, was considering a report sent to him by Emily Sorensen, vice president of operations. The report was a summary of the progress made by an activity-based management system that was implemented three years

> CableTech Bell Corporation (CTB) operates in the telecommunications industry. CTB has two divisions: the Phone Division and the Cable Service Division. The Phone Division manufactures telephones in several plants located in the Midwest. The product lines

> Elena Chavez is founder and CEO of Willowbank, Inc., which owns and operates several assisted-living facilities. The facilities are apartment-style buildings with 25 to 30 one- or two-bedroom apartments. While each apartment has its own complete kitchen,

> Refer to Brief Exercise 7-10. (Round percentages to four significant digits and cost allocations to the nearest dollar.) Required: 1. Calculate the total revenue, total costs, and total gross profit the company will earn on the sale of L-Ten, Triol, and

> Beauville Furniture Corporation produces sofas, recliners, and lounge chairs. Beauville is located in a medium-sized community in the southeastern part of the United States. It is a major employer in the community. In fact, the economic well-being of the

> Each of the following scenarios requires the use of accounting information to carry out one or more of the following managerial activities: (1) planning, (2) control and evaluation, (3) continuous improvement, or (4) decision making. a. MANAGER: At t

> Bill Christensen, the production manager, was grumbling about the new quality cost system the plant controller wanted to put into place. “If we start trying to track every bit of spoiled material, we’ll never get any work done. Everybody knows when they

> If I can increase my reported profit by $2 million, the actual earnings per share will exceed analysts’ expectations, and stock prices will increase. The stock options that I am holding will become more valuable. The extra income will also make me eligib

> Consider the following actions associated with a cost management information system: a. Eliminating a non-value-added activity b. Determining how much it costs to perform a heart transplant c. Calculating the cost of inspecting components from an outside

> Hepworth Communications produces cell phones. One of the four major electronic components is produced internally. The other three components are purchased from external suppliers. The electronic components and other parts are assembled (by the Assembly D

> Classify each of the following actions as either being associated with the financial accounting information system (FS) or the cost management information system (CMS): a. Determining the total compensation of the CEO of a public company b. Issuing a qua

> Refer to the data given in Exercise 10-8. Required: 1. Compute the residual income for each of the opportunities. (Round to the nearest dollar.) 2. Compute the divisional residual income (rounded to the nearest dollar) for each of the following four alte

> At the end of Year 2, the manager of the Canned Foods Division is concerned about the division’s performance. As a result, he is considering the opportunity to invest in two independent projects. The first is juice boxes for elementary

> Allard, Inc., presented two years of data for its Frozen Foods Division and its Canned Foods Division. Required: 1. Compute the ROI and the margin and turnover ratios for each year for the Frozen Foods Division. (Round your answers to four significant di

> A company manufactures three products, L-Ten, Triol, and Pioze, from a joint process. Each production run costs $12,900. None of the products can be sold at split-off, but must be processed further. Information on one batch of the three products is as fo

> Arbus Company provided the following information: Turnover 1.4 Operating assets $120,000 Operating income 6,720 Required: 1. What is ROI? 2. What is margin?

> Fermat, Inc., has acquired two new companies, one in consumer products and the other in financial services. Fermat’s top management believes that the executives of the two newly acquired companies can be most quickly assimilated into the parent company i

> The following selected data pertain to the Argent Division for last year: Sales $1,000,000 Variable costs $ 624,000 Traceable fixed costs $ 100,000 Average invested capital $1,500,000 Imputed interest rate 15% Required: 1. How much is the residual income

> Consider the data for each of the following four independent companies: Required: 1. Calculate the missing values in the above table. (Round rates to four significant digits.) 2. Assume that the cost of capital is 9 percent for each of the four firms. Co

> A multinational corporation has a number of divisions, two of which are the North American Division and the Pacific Rim Division. Data on the two divisions are as follows: Round all rates of return to four significant digits. Required: 1. Compute residua

> Asgard Farms, Inc., has a number of divisions that produce jams and jellies, condiments, and glassware. The Glassware Division manufactures a variety of bottles that can be sold externally (to soft-drink and juice bottlers) or internally to Asgard Farm’s

> Xenold, Inc., manufactures and sells cooktops and ovens through three divisions: Home, Restaurant, and Specialty. Each division is evaluated as a profit center. Data for each division for last year are as follows (numbers in thousands): The income tax ra

> Brewster Company manufactures elderberry wine. Last year, Brewster earned operating income of $192,000 after income taxes. Capital employed equaled $2.3 million. Brewster is 45 percent equity and 55 percent 10-year bonds paying 6 percent interest. Brewst

> Janson, Inc., uses a standard costing system. The predetermined overhead rates are calculated using practical capacity. Practical capacity for a year is defined as 100,000 units requiring 20,000 standard direct labor hours. Budgeted overhead for the year

> Madison Company uses the following rule to determine whether direct labor efficiency variances ought to be investigated. A direct labor efficiency variance will be investigated anytime the amount exceeds the lesser of $12,000 or 10 percent of the standar

> The expected costs for the Maintenance Department of Stazler, Inc., for the coming year include: Fixed costs (salaries, tools): $64,900 per year Variable costs (supplies): $1.35 per maintenance hour Estimated usage by: Assembly Department 4,500 Fabricati

> Samson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels: Paper pulp (4 lbs. @ $0.30) $ 1.20 Labor (1.8 hrs. @ $18) 32.40 Total prime cost $33.60 During the f

> Redfield Company uses two types of direct labor for the manufacturing of its products: fabricating and assembly. Redfield has developed the following standard mix for direct labor, where output is measured in units. During the second week in April, Redfi

> Chypre, Inc., purchased the amount used of each direct material input on May 2 for the following actual prices: solvent mix for $5.20 per gallon, and aromatic compound for $8,010 per gallon. Required: 1. Compute and journalize the direct materials price

> Chypre, Inc., produces a cologne mist using a solvent mix (water and pure alcohol) and aromatic compounds (the scent base) that it sells to other companies for bottling and sale to consumers. Chypre developed the following standard cost sheet: On May 2,

> Refer to the data in Exercise 9-15. Required: 1. Compute overhead variances using a two-variance analysis. 2. Compute overhead variances using a three-variance analysis. 3. Illustrate how the two- and three-variance analyses are related to the four-varia

> Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 120,000 units requiring 480,000 direct labor hours. (Practical capacity is 500,000 hours.)

> Berner Company produces a dark chocolate candy bar. Recently, the company adopted the following standards for one bar of the candy: Direct materials (8.2 oz. @ $0.09) $0.738 Direct labor (0.07 hr. @ $18.00) 1.26 Standard prime cost $1.998 During the firs

> During the year, Vandy Company produced 280,000 components for industrial metal working machinery. Vandy’s direct materials and direct labor standards per unit are as follows: Direct materials (3.70 lbs. @ $6) $22.20 Direct labor (1.80 hr. @ $15) 28.80 R

> Quincy Farms is a producer of items made from farm products that are distributed to supermarkets. For many years, Quincy’s products have had strong regional sales on the basis of brand recognition. However, other companies have been marketing similar pro

> Suppose Gene determines that next year’s Sales Division activities include the following: Research—researching current and future conditions in the industry Shipping—arranging for shipping of mattress

> Jackson Products produces a barbeque sauce using three departments: Cooking, Mixing, and Bottling. In the Cooking Department, all materials are added at the beginning of the process. Output is measured in ounces. The production data for July are as follo

> Next year, Bob’s Bistro expects to produce 50,000 units and sell 50,500 units at a price of $20.00 each. Beginning inventory of finished goods is $13,000, and ending inventory of finished goods is expected to be $10,000. Total selling expense is projecte

> Olympus, Inc., manufactures three models of mattresses: the Sleepeze, the Plushette, and the Ultima. Forecast sales for next year are 15,000 for the Sleepeze, 12,000 for the Plushette, and 5,000 for the Ultima. Gene Dixon, vice president of sales, has pr

> At the end of the year, Engersol, Inc., actually produced 305,000 units of the commercial cleaner and 120,000 of the deluxe model. The actual overhead costs incurred were: Maintenance $ 56,900 Power 10,000 Indirect labor 108,700 Rent 28,000 Required: Pre

> In an attempt to improve budgeting, the controller for Engersol, Inc., has developed a flexible budget for overhead costs. Engersol, Inc., makes two types of products, commercial floor cleaners and household floor cleaners. The company expects to produce

> Ingles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufacture

> Del Spencer’s purchases clothing evenly throughout the month. All purchases are on account. On the first of every month, Jana Spencer, Del’s wife, pays for all of the previous month’s purchases. Terms are 2/10, n/30 (i.e., a 2 percent discount can be tak

> Del Spencer is the owner and founder of Del Spencer’s Men’s Clothing Store. Del Spencer’s has its own house charge accounts and has found from past experience that 10 percent of its sales are for cash. The remaining 90 percent are on credit. An aging sch

> Historically, Ragman Company has had no significant bad debt experience with its customers. Cash sales have accounted for 20 percent of total sales, and payments for credit sales have been received as follows: 40 percent of credit sales in the month of t

> LeeAnn Ortiz owns a retail store that sells new and used sporting equipment. LeeAnn has requested a cash budget for October. After examining the records of the company, you find the following: a. Cash balance on October 1 is $980. b. Actual sales for Aug

> Rosita thinks that it may be time to refuse to accept checks and to start accepting credit cards. She is negotiating with VISA/MasterCard and American Express, and she would start the new policy on April 1. Rosita estimates that with the drop in sales fr

> Rosita Flores owns Rosita’s Mexican Restaurant in Tempe, Arizona. Rosita’s is an affordable restaurant near campus and several hotels. Rosita accepts cash and checks. Checks are deposited immediately. The bank charges $0.50 per check; the amount per chec

> Gunnison Company had the following equivalent units schedule and cost information for its Sewing Department for the month of December: Required: 1. Calculate the unit cost for December, using the FIFO method. 2. Calculate the cost of goods transferred ou

> Tiger Drug Store carries a variety of health and beauty aids, including 500-count bottles of vitamins. The sales budget for vitamins for the first six months of the year is presented below. The owner of Tiger Drug believes that ending inventories should

> Video-Forward, Inc., designs and manufactures wearable video cameras. Models A-1, A-2, and A-3 are lightweight video cameras that can be used on arms and headbands. Models A-4 and A-5 have larger memory, better resolution, and more Wi-Fi-related features

> Macchu Company produces stuffed toy animals; one of these is “Andie the Llama.” Each Andie takes 0.30 yard of fabric and eight ounces of polyfiberfill. Fabric costs $3.50 per yard and polyfiberfill is $0.05 per ounce.

> Archer Company produces two products: the custom and the basic. The custom sells for $30, and the basic sells for $8. Projected sales of the two models for the coming four quarters are given below. The president of the company believes that the projected

> Palmgren Company produces consumer products. The sales budget for four months of the year is presented below. Company policy requires that ending inventories for each month be 25 percent of next month’s sales. At the beginning of July,