Question: The Coca-Cola Company is a global

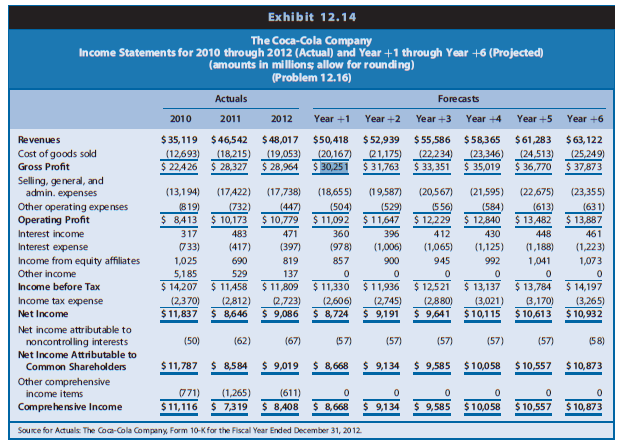

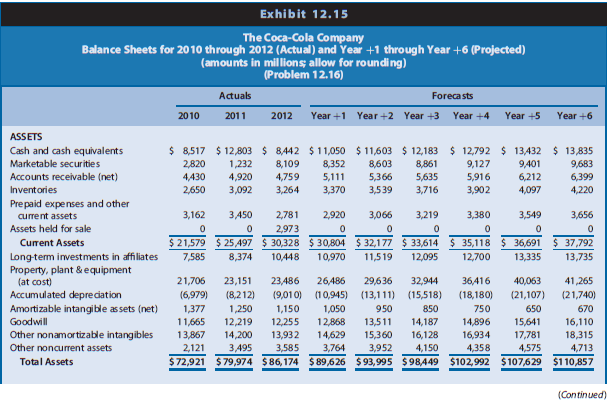

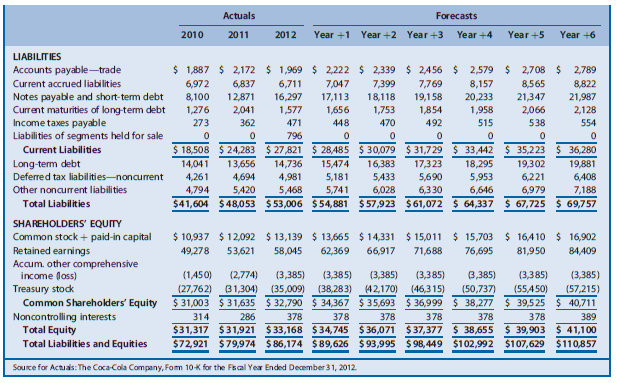

The Coca-Cola Company is a global soft drink beverage company (ticker: KO) that is a primary and direct competitor with PepsiCo. The data in Chapter 12’s Exhibits 12.14, 12.15, and 12.16 (pages 943–946) include the actual amounts for 2010, 2011, and 2012 and projected amounts for Year +1 to Year +6 for the income statements, balance sheets, and statements of cash flows, respectively, for Coca-Cola. The market equity beta for Coca-Cola at the end of 2012 is 0.75. Assume that the risk-free interest rate is 3.0% and the market risk premium is 6.0%. Coca-Cola had 4,469 million shares outstanding at the end of 2012, when Coca-Cola’s share price was $35.48.

REQUIRED

Part I—Computing Coca-Cola’s Share Value Using the Residual Income Valuation Approach

a. Use the CAPM to compute the required rate of return on common equity capital for

Coca-Cola.

b. Derive the projected residual income for Coca-Cola for Years +1 through +6 based on the projected financial statements. The financial statement forecasts for Year +6 assume that

Coca-Cola will experience a steady-state, long-run growth rate of 3% in Year +6 and beyond.

c. Using the required rate of return on common equity from Requirement a as a discount rate, compute the sum of the present value of residual income for Coca-Cola for Years +1 through +5.

d. Using the required rate of return on common equity from Requirement a as a discount rate and the long-run growth rate from Requirement b, compute the continuing value of Coca-Cola as of the start of Year +6 based on Coca-Cola’s continuing residual income in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1.

e. Compute the value of a share of Coca-Cola common stock.

(1) Compute the total sum of the present value of all residual income (from Requirements c and d).

(2) Add the book value of equity as of the beginning of the valuation (that is, as of the end of 2012, or the start of Yearþ1).

(3) Adjust the total sum of the present value of residual income plus book value of common equity using the midyear discounting adjustment factor.

(4) Compute the per-share value estimate.

Part II—Sensitivity Analysis and Recommendation

f. Using the residual income valuation approach, recomputed the value of Coca-Cola shares under two alternative scenarios.

Scenario 1: Assume that Coca-Cola’s long-run growth will be 2%, not 3% as above, and that Coca-Cola’s required rate of return on equity is 1% higher than that calculated in Requirement a.

Scenario 2: Assume that Coca-Cola’s long-run growth will be 4%, not 3% as above, and that Coca-Cola’s required rate of return on equity is 1% lower than that calculated in Requirement a.

To quantify the sensitivity of your share value estimate for Coca-Cola to these variations in growth and discount rates, compare (in percentage terms) your value estimates under these two scenarios with your value estimate from Requirement e.

g. Using these data at the end of 2012, what reasonable range of share values would you have expected for Coca-Cola common stock? At that time, what was the market price for Coca-Cola shares relative to this range? What would you have recommended?

h. If you completed Problem 12.16 in Chapter 12, compare the value estimate you obtained in Requirement e of that problem (using the free cash flows to common equity shareholders valuation approach) with the value estimate you obtain here using the residual income valuation approach. The value estimates should be the same. If you have not completed Problem 12.16, you would benefit from doing so now.

Transcribed Image Text:

Exhibit 12.14 The Coca-Cola Company Income Statements for 2010 through 2012 (Actual) and Year +1 through Year +6 (Projected) (amounts in millions; allow for rounding) (Problem 12.16) Actuals Forecasts 2010 2011 2012 Year +1 Year +2 Year +3 Year +4 Year +5 Year +6 $ 35,119 $46,542 (12,693) (18,215) $ 22,426 $ 28,327 $ 48,017 (19,053) $ 28,964 $ 63, 122 (25,249) $ 37,873 $50,418 $52,939 $ 55,586 (22,234) $ 33,351 $58,365 (23,346) $ 35,019 Revenues $61,283 Cost of goods sold (20,167) $ 30,251 (21,175) $ 31,763 (24,513) $ 36,770 Gross Profit Selling, general, and admin. expenses (13,194) (17,422) (17,738) (18,655) (19,587) (20,567) (21,595) (22,675) (23,355) Other operating expenses Operating Profit (819) (732) (447) (504) $ 11,092 (529) $ 11,647 (556) (584) (613) $ 13,482 448 (631) $ 10,173 483 $ 8413 $ 10,779 $ 12,229 $ 12,840 $ 13,887 Interest income 317 471 360 396 412 430 461 Interest expense (733) (417) (397) (978) (1,006) (1,065) (1,125) (1,188) (1,223) Income from equity affiliates 1,025 690 819 857 900 945 992 1,041 1,073 Other income 5,185 529 137 $ 11,330 $ 13,137 $ 13,784 $ 12,521 (2,880) $ 9,641 Income before Tax $ 14,207 $ 11,458 $ 11,809 $ 11,936 $ 14,197 Income tax expense (2,370) (2,812) (2,723) (2,606) (2,745) $ 9,191 (3,021) 3,170) (3,265) Net Income $11,837 $ 8,646 $ 9,086 $ 8,724 $10,115 $ 10,613 $ 10,932 Net income attributable to noncontrolling interests (50) (62) (67) (57) (57) (57) (57) (57) (58) Net Income Attributable to $11,787 $ 8,584 $ 9,019 $ 8,668 $ 9,134 $ 9,585 $ 10,058 $ 10,557 $ 10,873 Common Shareholders Other comprehensive income items 771) (1,265) (611) Comprehensive Income $11,116 $ 7,319 $ 8408 $ 8,668 $ 9,134 $ 9,585 $ 10,058 $ 10,557 $ 10,873 Source for Actuals The Coca-Cola Company, Form 10-Kfor the Fiscal Year Ended December 31, 2012 Exhibit 12.15 The Coca-Cola Company Balance Sheets for 2010 through 2012 (Actual) and Year +1 through Year +6 (Projected) (amounts in millions allow for rounding) (Problem 12.16) Actuals Forecasts 2010 2011 2012 Year +1 Year+2 Year +3 Year +4 Year +5 Year +6 ASSETS $ 13,835 $ 8,517 $ 12,803 $ 8,442 $ 11,050 $ 11,603 $ 12,183 $ 12,792 $ 13,432 9,401 6,212 4,097 Cash and cash equivalents Marketable securities 8,861 5,635 3,716 2,820 1,232 8,109 8,352 8,603 9,127 9,683 6,399 4,220 Accounts receivable (net) 4,430 4,920 4,759 5,111 5,366 5,916 Inventories 2,650 3,092 3,264 3,370 3,539 3,902 Prepaid expenses and other current assets 3,162 3,450 2,781 2,920 3,066 3,219 3,380 3,549 3,656 Assets held for sale 2,973 $ 21,579 $ 25,A97 $ 30,328 $ 30,804 $ 32,177 $ 33,614 $ 35,118 $ 36,691 $ 37,792 11,519 Curent Assets Long-term investments in affiliates Property, plant & equipment (at cost) Accumulated depre ciation Amortizable intangible assets (net) Goodwill 7,585 8,374 10,448 10,970 12,095 12,700 13,335 13,735 21,706 23,151 23,486 26,486 29,636 32,944 36,416 40,063 41,265 (6,979) (8,212) 1,250 (9,010) (10,945) (13,111) (15,518) (18,180) (21,107) (21,740) 1,377 11,665 1,150 12,255 13,932 1,050 950 850 750 650 670 12,219 14,200 12,868 13,511 14,187 14,896 15,641 16,110 Other nonamortiz able intangibles 13,867 14,629 15,360 16,128 16,934 4,358 17,781 18,315 Other noncurrent assets 3,952 $72,921 $79,974 $86,174 $ 89,626 $ 93,995 $98,449 $102,992 $107,629 $110,857 2,121 3,495 3,585 3,764 4,150 4,575 4,713 Total Assets (Continued) Actuals Forecasts 2010 2011 2012 Year +1 Year +2 Year +3 Year +4 Year +5 Year +6 LIABILITIES Accounts payable-trade $ 1,887 $ 2,172 $ 1,969 $ 2,222 $ 2,339 $ 2,456 $ 2,579 $ 2,708 $ 2,789 Current accrued liabilities 6,972 6,837 8,822 6,711 16,297 7,047 7,399 7,769 8,157 8,565 17,113 Notes payable and short-term debt Current maturities of long-term debt Income taxes payable Liabilities of segments held for sale 8,100 12,871 18,118 19,1 58 20,233 21,347 21,987 1,276 2,041 1,577 1,656 1,753 1,854 1,958 2,066 2,128 273 362 471 448 470 492 515 538 554 796 Current Liabilities $ 18,508 $ 24,283 $ 27,821 $ 28,485 $ 30,079 $ 31,729 $ 33,442 $ 35,223 $ 36,280 Long-term debt Deferred tax liabilities-noncurrent 13,656 4,694 14,041 14,736 15,474 16,383 17,323 18,295 19,302 19,881 4,261 4,981 5,181 5,433 5,690 5,953 6,221 6,408 Other noncurrent liabilities 4,794 5,420 5,468 5,741 6,028 6,330 6,646 6,979 7,188 Total Liabilities $41,604 $48,053 $ 53,006 $54,881 $ 57,923 $61,072 $ 64,337 $ 67,725 $ 69,757 SHAREHOLDERS' EQUITY Common stock + paid-in capital Retained earnings Accum. other comprehensive income (loss) $ 10,937 $ 12,092 $ 13,139 $ 13,665 $ 14,331 $ 15,011 $ 15,703 $ 16,410 $ 16,902 66,917 49,278 53,621 58,045 62,369 71,688 76,695 81,950 84,409 (1,450) (2,774) (3,385) (3,385) (3,385) (3,385) 3,385) (3,385) (3,385) Treasury stock (27,762) (38,283) $ 31,003 $ 31,635 $ 32,790 $ 34,367 $ 35,693 $ 36,999 $ 38,277 31,304) (35,009) (42,170) (46,315) (50,737) (55,450) (57,215) $ 39,525 $ 40,711 Common Sharehoklders' Equity Noncontrolling interests Total Equity 314 286 378 378 378 378 378 378 389 $31,317 $31,921 $33,168 $34,745 $ 36,071 $ 37,377 $ 38,655 $ 39,903 $ 41,100 $72,921 $79,974 $ 86,174 $ 89,626 $ 93,995 $ 98,449 $102,992 $107,629 $110,857 Total Liabilities and Equities Source for Actuais: The Coca-Cola Company, Fom 10-K for the Fkal Year Ended December 31, 2012 Exhibit 12.16 The Coca-Cola Company Projected Implied Statements of Cash Flows for Year +1 through Year +6 (amounts in millions; allow for rounding) (Problem 12.16) Forecasts Year +1 Year +2 Year +3 Year +4 Year +5 Year +6 IMPLIED STATEMENT OF CASH FLOWS $ 9,151 $ 9,600 2,407 (268) (177) (153) 117 $10,071 $ 8,705 1,935 (352) (106) (139) 253 336 (23) 200 $10,567 2,928 (296) (195) (169) 129 408 Net Income $10,884 Add back deprediation expense (net) (Increase) Decrease in receivables (net) (Increase) Decrease in inventories (Increase) Decrease in prepaid expenses Increase (Decrease) in accounts payable-trade Increase (Decrease) in current accrued liabilities Increase (Decrease) in income taxes payable Net change in deferred tax assets and liabilities Increase (Decrease) in other noncurrent liabilities Cash flows from assets/liabilities of segment sold Net Cash Flows from Operations 2,166 (256) (169) (146) 117 2,661 (282) (186) (161) 633 (186) (123) (106) 123 81 352 370 388 257 22 22 23 23 16 253 257 301 263 268 187 209 273 287 316 332 2,177 $13,259 $11,778 $13,995 $12,476 $13,217 $11,852 (Increase) Decrease in prop., plant, & equip, at cost (Increase) Decrease in marketable securities (Increase) Decrease in investment securities (Increase) Decrease in amortizable intangible assets (net) (Increase) Decrease in goodwill and nonamort. intang. (Increase) Decrease in other non-current assets Net Cash Flows from Investing (3,000) (243) (522) 100 (1,309) (179) 3(5,154) (3,150) (251) (549) 100 (1,375) (188) 3 (5,412) (3,308) (258) (576) 100 (1,444) (3,473) (266) (605) 3,647) (274) (635) 100 (1,592) (1,202) (282) (400) (20) (1,003) (137) 3 (3,043) 100 (198) $ (5,683) (1,516) (208) $ (5,967) (218) 3(6,265) 1,103 909 666 Increase (Decrease) in short-term debt 895 738 526 1,140 940 679 1,180 973 693 1,221 1,007 707 702 Increase (Decrease) in long-term debt Increase (Decrease) in common stock + paid-in capital Increase (Decrease) in accum. OCI and other equity adjs. Increase (Decrease) in treasury stock Dividends Dividends to noncontrolling interests Net Cash Flows from Finanding 579 492 (3,274) (4,324) (57) $ (5,496) $ 2,608 (3,887) (4,547) (57) $ (5,813) $ 553 (4,145) (4,77 1) (57) (4,422) (5,007) (57) $ (6,641) (4,713) (5,255) (57) (1,765) (8,367) (47) $ (6,214) 580 S (8405) $ 403 $ (7,091) Net Change in Cash 609 640

> Imagine that a small manufacturing company decides to invest in a materials resource planning (MRP) system. This is a computerized information system that improves efficiency by automating such work as planning needs for resources, ordering materials, an

> What are an organization’s basic duties under the Occupational Safety and Health Act?

> Given that the “reasonable woman” standard is based on women’s ideas of what is appropriate, how might an organization with mostly male employees identify and avoid behavior that could be found to be sexual harassment?

> To identify instances of sexual harassment, the courts may use a “reasonable woman” standard of what constitutes offensive behavior. This standard is based on the idea that women and men have different ideas of what behavior is appropriate. What are the

> How does each of the following labor force trends affect HRM? a. Aging of the labor force b. Diversity of the labor force c. Skill deficiencies of the labor force

> How is the employment relationship typical of modern organizations different from the relationship of a generation ago?

> What HRM functions could an organization provide through self-service? What are some of advantages and disadvantages of using self-service for these functions?

> Why do multinational organizations hire host-country nationals to fill most of their foreign positions, rather than sending expatriates for most jobs?

> Suppose an organization decides to improve collaboration and knowledge sharing by developing an intranet to link its global workforce. It needs to train employees in several different countries to use this system. List the possible cultural issues you ca

> In recent years, many U.S. companies have invested in Russia and sent U.S. managers there in an attempt to transplant U.S.-style management. According to Hofstede (see Figure 15.3), U.S. culture has low power distance, uncertainty avoidance, and long-ter

> What are some HRM challenges that arise when a U.S. company expands from domestic markets by exporting? When it changes from simply exporting to operating as an international company? When an international company becomes a global company?

> Why do organizations outsource HRM functions? How does outsourcing affect the role of human resource professionals? Would you be more attracted to the role of HR professional in an organization that outsources many HR activities or in the outside firm th

> Identify the parent country, host country or countries, and third country or countries in the following example: A global soft-drink company called Cold Cola is headquartered in Atlanta, Georgia. It operates production facilities in Athens, Greece and in

> In the past, a large share of expatriate managers from the United States have returned home before successfully completing their foreign assignments. Suggest some possible reasons for the high failure rate. What can HR departments do to increase the succ

> What abilities make a candidate more likely to succeed in an assignment as an expatriate? Which of these abilities do you have? How might a person acquire these abilities?

> For an organization with operations in three different countries, what are some advantages and disadvantages of setting compensation according to the labor markets in the countries where the employees live and work? What are some advantages and disadvant

> Suppose you work in the HR department of a company that is expanding into a country where the law and culture make it difficult to lay off employees. How should your knowledge of that difficulty affect human resource planning for the overseas operations?

> Besides cultural differences, what other factors affect human resource management in an organization with international operations?

> How do HRM practices such as performance management and work design encourage employee empowerment?

> If the parties negotiating a labor contract are unable to reach an agreement, what actions can resolve the situation?

> Suppose you are the HR manager for a chain of clothing stores. You learn that union representatives have been encouraging the stores’ employees to sign authorization cards. What events can follow in this process of organizing? Suggest some ways that you

> What legal responsibilities do employers have regarding unions? What are the legal requirements affecting unions?

> When an organization decides to operate facilities in other countries, how can HRM practices support this change?

> How has union membership in the United States changed over the past few decades? How does union membership in the United States compare with union membership in other countries? How might these patterns in union membership affect the HR decisions of an i

> Why do managers at most companies prefer that unions not represent their employees? Can unions provide benefits to an employer? Explain.

> Why do employees join labor unions? Did you ever belong to a labor union? If you did, do you think the union membership benefited you? If not, do you think a union would have benefited you? Why or why not?

> What are the legal restrictions on labor-management cooperation?

> What can a company gain from union-management cooperation? What can workers gain?

> What are the usual steps in a grievance procedure? What are the advantages of resolving a grievance in the first step? What skills would a supervisor need so grievances can be resolved in the first step?

> Why are strikes uncommon? Under what conditions might management choose to accept a strike?

> Imagine that you are the human resource manager of a small architectural firm. You learn that the monthly premiums for the company’s existing health insurance policy will rise by 15 percent next year. What can you suggest to help your company manage this

> What are some advantages of offering a generous package of insurance benefits? What are some drawbacks of generous insurance benefits?

> How do tax laws and accounting regulations affect benefits packages?

> Merging, downsizing, and reengineering all can radically change the structure of an organization. Choose one of these changes and describe HRM’s role in making the change succeed. If possible, apply your discussion to an actual merger, downsizing, or ree

> In principle, health insurance would be the most attractive to employees with large medical expenses, and retirement benefits would be most attractive to older employees. What else might a company include in its benefits package to appeal to young, healt

> Define the types of benefits required by law. How can organizations minimize the cost of these benefits while complying with the relevant laws?

> Why do employers provide employee benefits, rather than providing all compensation in the form of pay and letting employees buy the services they want?

> Why is it important to communicate information about employee benefits? Suppose you work in the HR department of a company that has decided to add new benefits—dental and vision insurance plus an additional two days of paid time off for “personal days.”

> What legal requirements might apply to a family leave policy? Suggest how this type of policy should be set up to meet those requirements.

> What issues should an organization consider in selecting a package of employee benefits? How should an employer manage the trade-offs among these considerations?

> Why do some organizations link the use of incentive pay to the organization’s overall performance? Is it appropriate to use stock performance as an incentive for employees at all levels? Why or why not?

> Suppose you are a human resource professional at a company that is setting up work teams for production and sales. What group incentives would you recommend to support this new work arrangement?

> What are the pros and cons of linking incentive pay to individual performance? How can organizations address the negatives?

> In a typical large corporation, the majority of the chief executive’s pay is tied to the company’s stock price. What are some benefits of this pay strategy? Some risks? How can organizations address the risks?

> At many organizations, goals include improving people’s performance by relying on knowledge workers, empowering employees, and assigning work to teams. How can HRM support these efforts?

> How can human resource management contribute to a company’s success?

> Suppose you are applying the residual income valuation model to value a firm with extremely conservative accounting. Suppose, for example, the firm is following U.S. GAAP or IFRS, but the firm does not recognize a substantial intangible asset on the bala

> Identify conditions that would lead an analyst to expect that management might attempt to manage earnings upward.

> In Problem 10.16, we projected financial statements for Walmart Stores, Inc. (Walmart) for Years +1 through +5. The data in Chapter 12’s Exhibits 12.17, 12.18, and 12.19 include the actual amounts for 2012 and the projected amounts for

> Exhibit 13.7 presents selected hypothetical data from projected financial statements for Steak ‘n Shake for Year +1 to Year +11. The amounts for Year +11 reflect a long-term growth assumption of 3%. The cost of equity capital is 9.34%.

> Priority Contractors provides maintenance and cleaning services to various corporate clients in New York City. The firm has provided the following forecasts of comprehensive income for Year +1 to Year +5: Year +1:........................................

> Starwood Hotels (Starwood) owns and operates many hotel properties under well-known brand names, including Sheraton, W, Westin, and St. Regis. Starwood focuses on the upper end of the lodging industry. Choice Hotels (Choice) is primarily a franchisor of

> A firm has experienced a decrease in its current ratio but an increase in its quick ratio during the last three years. What is the likely explanation for these results?

> Northrop Grumman Corporation is a leading global security company that provides innovative systems products and solutions in aerospace, electronics, information systems, shipbuilding, and technical services to government and commercial customers worldwid

> Assume American Airlines acquires a regional airline in the mid-western United States for $450 million. American Airlines allocates $150 million of the purchase price to landing rights at various airports. The landing rights expire in five years. What ty

> Morrissey Tool Company manufactures machine tools for other manufacturing firms. The firm is wholly owned by Kelsey Morrissey. The firm’s accountant developed the following long-term forecasts of comprehensive income: Year +1:............................

> Select data for Avis and Hertz for 2012 follow. Based only on this information and ratios that you construct, speculate on similarities and differences in the operations and financing decisions of the two companies based on similarities and differences i

> If the firm is in a very competitive, mature industry, what effect will the competitive conditions have on residual income for the firm and others in the industry? Now suppose the firm holds a competitive advantage in its industry, but the advantage is n

> Vulcan Materials Company, a member of the S&P 500 Index, is the nation’s largest producer of construction aggregates, a major producer of asphalt mix and concrete, and a leading producer of cement in Florida. Exhibit 6.19 presents V

> The chapter describes free cash flows for common equity shareholders. Suppose a firm has no debt and uses marketable securities to manage operating liquidity. If the firm uses cash to purchase marketable securities, how does that transaction affect free

> Gap Inc. operates chains of retail clothing stores under the names of Gap, Banana Republic, and Old Navy. Exhibit 3.21 presents the statement of cash flows for Gap for Year 0 to Year 4. REQUIRED Discuss the relations between net income and cash flow fro

> Tesla Motors manufactures high performance electric vehicles that are extremely slick looking. Exhibit 3.20 presents the statement of cash flows for Tesla Motors for 2010–2012. REQUIRED Discuss the relations among net income, cash flow

> Texas Instruments primarily develops and manufactures semiconductors for use in technology-based products for various industries. The manufacturing process is capital-intensive and subject to cyclical swings in the economy. Because of overcapacity in the

> Refer to the websites and the Form 10-K reports of Home Depot (www.homedepot.com) and Lowe’s (www.lowes.com). Compare and contrast their business strategies.

> Assume that the firm’s cost of equity capital is 10% and that the firm’s existing assets and operations generate a 10% return on common equity. If the firm raises additional equity capital and invests in assets that will generate a return less than 10%,

> Microsoft Corporation (Microsoft) and Oracle Corporation (Oracle) engage in the design, manufacture, and sale of computer software. Microsoft sells and licenses a wide range of systems and application software to businesses, computer hardware manufacture

> The Coca-Cola Company (Coca-Cola), like PepsiCo, manufactures and markets a variety of beverages. Exhibit 3.18 presents a statement of cash flows for Coca-Cola for three years. REQUIRED Discuss the relations between net income and cash flow from operat

> BTB Electronics Inc. manufactures parts, components, and processing equipment for electronics and semiconductor applications in the communications, computer, automotive, and appliance industries. Its sales tend to vary with changes in the business cycle

> United Van Lines purchased a truck with a list price of $250,000 subject to a 6% discount if paid within 30 days. United Van Lines paid within the discount period. It paid $4,000 to obtain title to the truck with the state and an $800 license fee for the

> Flight Training Corporation is a privately held firm that provides fighter pilot training under contracts with the U.S. Air Force and the U.S. Navy. The firm owns approximately 100 Lear jets that it equips with radar jammers and other sophisticated elect

> Nojiri Pharmaceutical Industries develops, manufactures, and markets pharmaceutical products in Japan. The Japanese economy experienced recessionary conditions in recent years. In response to these conditions, the Japanese government increased the propor

> Eli Lilly and Company produces pharmaceutical products for humans and animals. Exhibit 7.18 includes a footnote excerpt from the annual report of Lilly for the period ending December 31, 2004. REQUIRED Review Exhibit 7.18 and answer the following questi

> Exhibit 3.27 presents common-size statements of cash flows for eight firms in various industries. All amounts in the common-size statements of cash flows are expressed as a percentage of cash flow from operations. In constructing the common-size percenta

> Aer Lingus is an international airline based in Ireland. Exhibit 3.26 provides the statement of cash flows for Year 1 and Year 2, which includes a footnote from the financial statements. Year 2 was characterized by weakening consumer demand for air trave

> Exhibit 6.22 presents selected financial statement data for Enron Corporation as originally reported for 1997, 1998, 1999, and 2000. In 2001, Enron restated its financial statements for earlier years because it reported several items beyond the limits of

> If a firm’s residual income for a particular year is positive, does that mean the firm was profitable? Explain. If a firm’s residual income for a particular year is negative, does that mean the firm necessarily reported a loss on the income statement? Ex

> The text states, ‘‘Over sufficiently long time periods, net income equals cash inflows minus cash outflows, other than cash flows with owners.’’ Demonstrate the accuracy of this statement in the following scenario: Two friends contributed $50,000 each to

> Firms value inventory under a variety of assumptions, including two common methods: last-in first out (LIFO) and first-in first-out (FIFO). Ignore taxes, assume that prices increase over time, and assume that a firm’s inventory balance is stable or grows

> ‘‘Asset valuation and recognition of net income closely relate.’’ Explain, including conditions when they do not.

> Exhibit 4.22 presents selected operating data for three retailers for a recent year. Macy’s operates several department store chains selling consumer products such as brand-name clothing, china, cosmetics, and bedding and has a large pr

> The chapter describes free cash flows for common equity shareholders. If the firm borrows cash by issuing debt, how does that transaction affect free cash flows for common equity shareholders in that period? If the firm uses cash to repay debt, how does

> ‘‘Some asset valuations using historical costs are highly relevant and very representationally faithful, whereas others may be representationally faithful but lack relevance. Some asset valuations based on fair values are highly relevant and very represe

> A recent article in Fortune magazine listed the following firms among the top ten most admired companies in the United States: Dell, Southwest Airlines, Microsoft, and Johnson & Johnson. Access the websites of these four companies or read the Business se

> A firm’s income tax return shows income taxes for 2009 of $35,000. The firm reports deferred tax assets before any valuation allowance of $24,600 at the beginning of 2009 and $27,200 at the end of 2009. It reports deferred tax liabilities of $18,900 at t

> Describe how the statement of cash flows is linked to each of the other financial statements (income statement and balance sheet). Also review how the other financial statements are linked with each other.

> Explain residual ROCE (return on common shareholders’ equity). What does residual ROCE represent? What does residual ROCE measure?

> Suppose the following hypothetical data represent total assets, book value, and market value of common shareholders’ equity (dollar amounts in millions) for Microsoft, Intel, and Dell, three firms involved in different aspects of the co

> What are the fundamental determinants of share value, and how do they affect market-based valuation multiples, such as market-to-book and price earnings ratios?

> A firm’s income tax return shows $50,000 of income taxes owed for 2009. For financial reporting, the firm reports deferred tax assets of $42,900 at the beginning of 2009 and $38,700 at the end of 2009. It reports deferred tax liabilities of $28,600 at th

> Explain the implications of a value to- book ratio that is exactly equal to 1. Compare the implications of a value-to-book ratio that is greater than 1 to those of a value-to-book ratio that is less than 1.

> Sunbeam Corporation manufactures and sells a variety of small household appliances, including toasters, food processors, and waffle grills. Exhibit 6.21 presents a statement of cash flows for Sunbeam for Year 5, Year 6, and Year 7. After experiencing dec

> Effective financial statement analysis requires an understanding of a firm’s economic characteristics. The relations between various financial statement items provide evidence of many of these economic characteristics. Exhibit 1.22 pres

> Dick’s Sporting Goods is a chain of full-line sporting goods retail stores offering a broad assortment of brand name sporting goods equipment, apparel, and footwear. Dick’s Sporting Goods had its initial public offerin

> In conceptual terms, explain the value-to-book valuation approach. Explain how the value-to-book approach described and demonstrated in this chapter relates to the residual income valuation approach described and demonstrated in Chapter 13.

> Analyzing the profitability of restaurants requires consideration of their strategies with respect to ownership of restaurants versus franchising. Firms that own and operate their restaurants report the assets and financing of those restaurants on their

> If the firm borrows capital from a bank and invests it in assets that earn a return greater than the interest rate charged by the bank, what effect will that have on residual income for the firm? How does that effect compare with the effects of capital s

> Why is it appropriate to use the required rate of return on equity capital (rather than the weighted-average cost of capital) as the discount rate when using the residual income valuation approach?

> The Coca-Cola Company is a global soft drink beverage company (ticker symbol ¼ KO) that is a primary and direct competitor with PepsiCo. The data in Exhibits 12.14–12.16 include the actual amounts for 2010, 2011, and 2012

> Identify conditions that would lead an analyst to expect that management might attempt to manage earnings downward.

> Explain the two roles of book value of common shareholders’ equity in the residual income valuation approach.