Question: Assume that Home and Office City, Inc.,

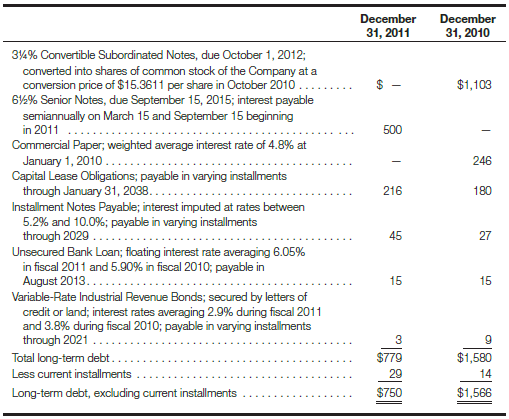

Assume that Home and Office City, Inc., provided the following comparative data concerning long-term debt in the notes to its 2011 annual report (amounts in millions):

Required:

a. As indicated, Home and Office City’s 31â„4% Convertible Subordinated Notes were converted into shares of common stock in October 2010. How many shares of stock were issued in conversion of these notes?

b. Regarding the 61â„2% Senior Notes, Home and Office City, Inc., also disclosed that “The Company, at its option, may redeem all or any portion of the Senior Notes by notice to the holder. The Senior Notes are redeemable at a redemption price, plus accrued interest, equal to the greater of (1) 100% of the principal amount of the Senior Notes to be redeemed or (2) the sum of the present values of the remaining scheduled payments of principal and interest on the Senior Notes to maturity.†Redeemable fixed-rate notes, such as those described here, are similar to callable term bonds. Thinking of the 61â„2% Senior Notes on this basis, would it have been possible for Home and Office City, Inc., to redeem (“callâ€) these notes for an amount

1. Below face value (at a discount)?

2. Above face value (at a premium)?

3. Equal to face value (at par)?

What circumstances would have been most likely to prompt Home and Office City to redeem these notes?

c. Recall from the discussion of Cash and Cash Equivalents in Chapter 5 that commercial paper is like an IOU issued by a very creditworthy corporation. Home and Office City’s note disclosures concerning commercial paper reveal that “The company has a back-up credit facility with a consortium of banks for up to $800 million. The credit facility contains various restrictive covenants, none of which is expected to materially impact the company’s liquidity or capital resources.†What do you think is meant by this statement?

d. What other information would you have wanted to know about Home and Office City’s “Capital Lease Obligations†when making an assessment of the company’s overall liquidity and leverage?

e. Regarding the “Installment Notes Payable,†what is meant by “interest imputed at rates between 5.2% and 10%�

f. Why do you suppose that Home and Office City’s “Unsecured Bank Loan†was immaterial in relation to the company’s total long-term debt?

g. Note that the “current installments†due on Home and Office City’s long-term debt were immaterial in amount for both years presented. Based on the data presented

in this case, explain why this is likely to change over the next five years.

Transcribed Image Text:

December December 31, 2011 31, 2010 34% Convertible Subordinated Notes, due October 1, 2012; converted into shares of common stock of the Company at a conversion price of $15.3611 per share in October 2010.. $1,103 6%% Senior Notes, due September 15, 2015; interest payable semiannually on March 15 and September 15 beginning in 2011 500 Commercial Paper; weighted average interest rate of 4.8% at January 1, 2010. Capital Lease Obligations; payable in varying installments through January 31, 2038... Installment Notes Payable; interest imputed at rates between 5.2% and 10.0%; payable in varying installments through 2029 ... Unsecured Bank Loan; floating interest rate averaging 6.05% in fiscal 2011 and 5.90% in fiscal 2010; payable in August 2013... Variable-Rate Industrial Revenue Bonds; secured by letters of credit or land; interest rates averaging 2.9% during fiscal 2011 and 3.8% during fiscal 2010; payable in varying installments through 2021.. 246 216 180 45 27 15 15 3 6. Total long-term debt. $779 $1,580 Less current installments 29 14 Long-term debt, excluding current installments $750 $1,566

> Homestead Oil Corp. was incorporated on January 1, 2010, and issued the following stock for cash: 800,000 shares of no-par common stock were authorized; 150,000 shares were issued on January 1, 2010, at $19 per share. 200,000 shares of $100 par value, 9

> Allyn, Inc., has the following owners’ equity section in its November 30, 2010, balance sheet: Paid-in capital: 12% preferred stock, $60 par value, 1,500 shares authorized, issued, and outstanding . . .. .. . . .. . . . . . .. . . .. . . . $ ? Common st

> Assume that you own 3,000 shares of Blueco, Inc.’s, common stock and that you currently receive cash dividends of $.42 per share per year. Required: a. If Blueco, Inc., declared a 5% stock dividend, how many shares of common stock would you receive as a

> Indicate the effect of each of the following transactions on total assets, total liabilities, and total owners’ equity. Use ï€«ï€ for increase, − for decrease, and (NE) for no effect. The

> Under what circumstances would you (as an investor) prefer to receive cash dividends rather than stock dividends? Under what circumstances would you prefer stock dividends to cash dividends?

> Blanker, Inc., has paid a regular quarterly cash dividend of $0.50 per share for several years. The common stock is publicly traded. On February 21 of the current year, Blanker’s board of directors declared the regular first-quarter dividend of $0.50 per

> Qamar, Inc., did not pay dividends in 2009 or 2010, even though 50,000 shares of its 6.5%, $50 par value cumulative preferred stock were outstanding during those years. The company has 800,000 shares of $2.50 par value common stock outstanding. Required

> Calculate the cash dividends required to be paid for each of the following preferred stock issues: Required: a. The semiannual dividend on 6% cumulative preferred, $50 par value, 30,000 shares authorized, issued, and outstanding. b. The annual dividend

> Calculate the annual cash dividends required to be paid for each of the following preferred stock issues: Required: a. $3.75 cumulative preferred, no par value; 200,000 shares authorized, 161,522 shares issued. (The treasury stock caption of the stockho

> The balance sheet caption for common stock is the following: Common stock without par value, 2,000,000 shares authorized, 400,000 shares issued, and 360,000 shares outstanding . . . . . . . . . . . . . . . . . . . . . . . $2,600,000 Required: a. Calcul

> From the following data, calculate the Retained Earnings balance as of December 31, 2010: Retained earnings, December 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $490,400 Net decrease in total assets during 2011

> At the beginning of the current fiscal year, the balance sheet of Cummings Co. showed liabilities of $219,000. During the year, liabilities decreased by $36,000; assets increased by $77,000; and paid-in capital also increased by $10,000 to $190,000. Divi

> At the beginning of the current fiscal year, the balance sheet of Hughey, Inc., showed owners’ equity of $520,000. During the year, liabilities increased by $21,000 to $234,000; paid-in capital increased by $40,000 to $175,000; and asse

> Assume that you own 500 shares of $10 par value common stock of a company and the company has a 2-for-1 stock split when the market price per share is $40. Required: a. How many shares of common stock will you own after the stock split? b. What will pro

> Circle-Square, Ltd., is in the process of liquidating and going out of business. The firm’s balance sheet shows $22,800 in cash, accounts receivable of $114,200, inventory totaling $61,400, plant and equipment of $265,000, and total liabilities of $305,6

> Find a list of common stock exdividend date data. (You can go, via Google, to stocks—wsj.com. Select the reference which is labeled Market Data Center; then select the stocks and trading statistics tab; then select the Dividends section. Scroll down unti

> Knight, Inc., expects to incur a loss for the current year. The chairperson of the board of directors wants to have a cash dividend so that the company’s record of having paid a dividend during every year of its existence will continue. What factors will

> Your conversation with Mr. Gerrard, which took place in February 2011 (see Case 6.28), continued as follows: Case 4.26: Gerrard Construction Co. is an excavation contractor. The following summarized data (in thousands) are taken from the December 31, 2

> The transactions affecting the owners’ equity accounts of DeZurik Corp. for the year ended June 30, 2011, are summarized here: 1. 320,000 shares of common stock were issued at $14.25 per share. 2. 80,000 shares of treasury (common) stock were sold for $

> For now you can ignore the 2011 column in the balance sheet; all disclosures presented here relate to the June 30, 2010, balance sheet.) DeZurik Corp. had the following owners’ equity section in its June 30, 2010, balance sheet (in thou

> On January 1, 2010, Learned, Inc., issued $60 million face amount of 20-year, 14% stated rate bonds when market interest rates were 16%. The bonds pay interest semiannually each June 30 and December 31 and mature on December 31, 2029. Required: a. Using

> On January 1, 2010, Drennen, Inc., issued $3 million face amount of 10-year, 14% stated rate bonds when market interest rates were 12%. The bonds pay semiannual interest each June 30 and December 31 and mature on December 31, 2019. Required: a. Using th

> Riley Co. has outstanding $40 million face amount of 15% bonds that were issued on January 1, 1998, for $39,000,000. The 20-year bonds mature on December 31, 2017, and are callable at 102 (that is, they can be paid off at any time by paying the bondholde

> O’Kelley Co. has outstanding $2 million face amount of 12% bonds that were issued on January 1, 2002, for $2 million. The 20-year bonds were issued in $1,000 denominations and mature on December 31, 2021. Each $1,000 bond is convertible at the bondholder

> The following summary data for the payroll period ended December 27, 2009, are available for Cayman Coating Co.: Gross pay . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . $53,000 FICA tax withholdings . . . . . . .

> The following information was obtained from the records of Breanna, Inc.: Accounts receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . .. $ 10,000 Accumulated depreciation. . . . . . . . . . . . . . . . . .. . . . ... . 52,000 Cost of goods

> The following summary data for the payroll period ended on November 14, 2009, are available for Brac Construction Ltd.: Gross pay . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ ? FICA tax withholdings . . .

> Evans Ltd. publishes a monthly newsletter for retail marketing managers and requires its subscribers to pay $50 in advance for a one-year subscription. During the month of September 2010, Evans Ltd. sold 200 one-year subscriptions and received payments i

> (Note: See Exercise 5.14 for the related prepaid expense accounting .) On November 1, 2010, Gordon Co. collected $25,200 in cash from its tenant as an advance rent payment on its store location. The six-month lease period ends on April 30, 2011, at which

> Enter the following column headings across the top of a sheet of paper: Enter the transaction/adjustment letter in the first column and show the effect, if any, of each transaction/adjustment on the appropriate balance sheet category or on net income b

> Enter the following column headings across the top of a sheet of paper: Enter the transaction/adjustment letter in the first column, and show the effect, if any, of each of the transactions/adjustments on the appropriate balance sheet category or on th

> Enter the following column headings across the top of a sheet of paper: Enter the transaction/adjustment letter in the first column and show the effect, if any, of each of the transactions/adjustments on the appropriate balance sheet category or on the

> The difference between the amounts of book and tax depreciation expense, as well as the desire to report income tax expense that is related to book income before taxes, causes a long-term deferred income tax liability to be reported on the balance sheet.

> Atom Endeavour Co. issued $250 million face amount of 9% bonds when market interest rates were 8.92% for bonds of similar risk and other characteristics. Required: a. How much interest will be paid annually on these bonds? b. Were the bonds issued at a

> Reynolds Co. issued $40 million face amount of 11% bonds when market interest rates were 11.14% for bonds of similar risk and other characteristics. Required: a. How much interest will be paid annually on these bonds? b. Were the bonds issued at a premi

> On March 1, 2005, Matt purchased $63,000 of Lawson Co.’s 8%, 20-year bonds at face value. Lawson Co. has paid the annual interest due on the bonds regularly. On March 1, 2010, market interest rates had risen to 12%, and Matt is considering selling the bo

> Gary’s TV had the following accounts and amounts in its financial statements on December 31, 2010. Assume that all balance sheet items reflect account balances at December 31, 2010, and that all income statement items reflect activities that occurred dur

> On August 1, 2002, Bonnie purchased $15,000 of Huber Co.’s 10%, 20-year bonds at face value. Huber Co. has paid the semiannual interest due on the bonds regularly. On August 1, 2010, market rates of interest had fallen to 8%, and Bonnie is considering se

> Coley Co. issued $30 million face amount of 9%, 10-year bonds on June 1, 2010. The bonds pay interest on an annual basis on May 31 each year. Required: a. Assume that the market interest rates were slightly higher than 9% when the bonds were sold. Would

> Kaye Co. issued $1 million face amount of 11%, 20-year bonds on April 1, 2010. The bonds pay interest on an annual basis on March 31 each year. Required: a. Assume that market interest rates were slightly lower than 11% when the bonds were sold. Would t

> Kirkland Theater sells season tickets for six events at a price of $252. For the 2010 season, 1,200 season tickets were sold. Required: a. Use the horizontal model (or write the journal entry) to show the effect of the sale of the season tickets. b. Use

> Cool froth Brewing Company distributes its products in an aluminum keg. Customers are charged a deposit of $50 per keg; deposits are recorded in the Keg Deposits account. Required: a. Where on the balance sheet will the Keg Deposits account be found? Ex

> Prist Co. had not provided a warranty on its products, but competitive pressures forced management to add this feature at the beginning of 2010. Based on an analysis of customer complaints made over the past two years, the cost of a warranty program was

> Karysa Co. operates in a city in which real estate tax bills for one year are issued in May of the subsequent year. Thus tax bills for 2010 are issued in May 2011 and are payable in July 2011. Required: a. Explain how the amount of tax expense for calen

> At March 31, 2010, the end of the first year of operations at Jaryd, Inc., the firm’s accountant neglected to accrue payroll taxes of $4,800 that were applicable to payrolls for the year then ended. Required: a. Use the horizontal model (or write the jo

> On August 1, 2010, Colombo Co.’s treasurer signed a note promising to pay $240,000 on December 31, 2010. The proceeds of the note were $232,000. Required: a. Calculate the discount rate used by the lender. b. Calculate the effective interest rate (APR)

> On April 15, 2010, Powell, Inc., obtained a six-month working capital loan from its bank. The face amount of the note signed by the treasurer was $300,000. The interest rate charged by the bank was 9%. The bank made the loan on a discount basis. Require

> Pope’s Garage had the following accounts and amounts in its financial statements on December 31, 2010. Assume that all balance sheet items reflect account balances at December 31, 2010, and that all income statement items reflect activities that occurred

> Enter the following column headings across the top of a sheet of paper: Enter the transaction/adjustment letter in the first column and show the effect, if any, of each transaction/adjustment on the appropriate balance sheet category or on net income b

> A review of the accounting records at Corless Co. revealed the following information concerning the company’s liabilities that were outstanding at December 31, 2011, and 2010, respectively: Required: a. Corless Co. has not yet made an

> Ambrose Co. has the option of purchasing a new delivery truck for $28,200 in cash or leasing the truck for $6,100 per year, payable at the end of each year for six years. The truck also has a useful life of six years and will be depreciated on a straight

> On January 1, 2010, Carey, Inc., entered into a No cancellable lease agreement, agreeing to pay $3,500 at the end of each year for four years to acquire a new computer system having a market value of $10,200. The expected useful life of the computer syst

> The balance sheets of HiROE, Inc., showed the following at December 31, 2011, and 2010: Required: a. If there have not been any purchases, sales, or other transactions affecting this equipment account since the equipment was first acquired, what is the

> The balance sheets of Tully Corp. showed the following at December 31, 2011, and 2010: Required: a. If there have not been any purchases, sales, or other transactions affecting this machine account since the machine was first acquired, what is the amou

> Moyle Co. acquired a machine on January 1, 2010, at a cost of $320,000. The machine is expected to have a five-year useful life, with a salvage value of $20,000. The machine is capable of producing 300,000 units of product in its lifetime. Actual product

> Grove Co. acquired a production machine on January 1, 2010, at a cost of $240,000. The machine is expected to have a four year useful life, with a salvage value of $40,000. The machine is capable of producing 50,000 units of product in its lifetime. Actu

> Porter, Inc., acquired a machine that cost $720,000 on October 1, 2010. The machine is expected to have a four-year useful life and an estimated salvage value of $80,000 at the end of its life. Porter, Inc., uses the calendar year for financial reporting

> The information presented here represents selected data from the December 31, 2010, balance sheets and income statements for the year then ended for three firms: Required: Calculate the missing amounts for each firm. Firm A Firm B Firm C Total asse

> Listed here are a number of financial statement captions. Indicate in the spaces to the right of each caption the category of each item and the financial statement(s) on which the item can usually be found. Use the following abbreviations: Category

> When Yuji died in March 2017, his gross estate was valued at $8 million. He owed debts totaling $300,000. Funeral and administration expenses were $12,000 and $120,000, respectively. The marginal estate tax rate exceeded his estate’s marginal income tax

> Fifteen years ago, Mrs. Cobb purchased land costing $80,000. She had the land titled in the names of Mr. and Mrs. Cobb, joint tenants with right of survivor ship. Mrs. Cobb died and was survived by Mr. Cobb. At Mrs. Cobb’s death, the land’s value was $20

> Five years ago, Andy and Sandy, siblings, pooled their resources and purchased a warehouse. Andy provided $50,000 of consideration, and Sandy furnished $100,000. Andy died and was survived by Sandy. The property, which they had titled in the names of And

> Ten years ago, Art purchased land for $60,000 and immediately titled it in the names of Art and Bart, joint tenants with right of survivorship. Bart paid no consideration. In 2017, Art died and was survived by Bart, his brother. The land’s value had appr

> Twelve years ago, Latoya transferred property to an irrevocable trust with a bank trustee. Latoya named Al to receive the trust income annually for life and Pat or Pat’s estate to receive the remainder upon Al’s death. Latoya reserved the power to design

> John owns all the stock of Lucas Corporation, an S corporation. John’s basis for the 1,000 shares is $130,000. On June 11 of the current year (assume a non-leap year), John gifts 100 shares of stock to his younger brother Michael, who has been working in

> Sue died on May 3, 2017. On October 1, 2015, Sue gave her son Tom land valued at $7,014,000. Sue applied a unified credit of $2,117,800 against the gift tax due on this transfer. On Sue’s date of death the land was valued at $9.4 million. a. With respec

> Mary died on April 3, 2017. As of this date, Mary’s gross estate was valued at $6.5 million. On October 3, Mary’s gross estate was valued at $5.8 million. The estate neither distributed nor sold any assets before October 3, 2017. Mary’s estate had no ded

> P Corporation purchases 100% of S Corporation’s stock for $2 million on January 1 of the current year. The corporations elect to file a consolidated tax return. During the current year, S reports $350,000 of taxable income and $30,000 of tax-exempt inter

> Giovanni died in 2017 with a gross estate of $6.9 million and debts of $30,000. He made post-1976 taxable gifts of $100,000, valued at $80,000 when Giovanni died. His estate paid state death taxes of $110,200. Calculate his estate tax base.

> Austin & Becker is an electing large partnership. During the current year, the partnership has the following income, loss, and deduction items: Ordinary income………………………………………………….$5,200,000 Rental loss…………………………………………………………(2,000,000) Longterm capital

> Maria Martinez died in 2017, survived by her spouse, Sergio, and two adult children. Her gross estate, all of which passed under her will, was valued at $7.2 million. She had Sec. 2053 deductions of $100,000. Her will left $200,000 to her church, 20% of

> Will, a bachelor, died in 2017. At that time, his sole asset was cash of $6 million. Assume no debts or funeral and administration expenses and no charitable bequests. His gift history was as follows: a. What was Will’s estate tax base

> Maria purchased an interest in a real estate tax shelter many years ago and deducted losses from its operation for several years. The real property owned by the tax shelter when Maria made her investment has been fully depreciated on a straightline basi

> Beth died on May 3, 2017. Her executor elected date-of-death valuation. Beth’s gross estate included, among other properties, the items listed below. What is the estate tax value of each item? a. 4,000 shares of Highline Corporation stock, traded on a s

> Debra has operated a family counseling practice for a number of years as a sole proprietor. She owns the condominium office space that she occupies in addition to her professional library and office furniture. She has a limited amount of working capital

> Consider the following balance sheet for DEF Partnership: Suppose Daniel wishes to exit the partnership completely. After discussions with Edward and Frances, the partners agree to let Daniel choose one of three options: 1. Daniel takes a liquidating d

> Frank, Greta, and Helen each have a one­third interest in the FGH Partnership. On December 31, 2016, the partnership reported the following balance sheet: The partnership placed Asset 1 (seven­year property) in service in 2014 and

> Pedro owns a 60% interest in the PD General Partnership having a $40,000 basis and $200,000 FMV. His share of partnership liabilities is $100,000. Because he is nearing retirement age, he has decided to give away his partnership interest on June 15 of th

> Della retires from the BCD General Partnership when her basis in her partnership interest is $70,000 including her $10,000 share of liabilities. The partnership is in the business of providing house cleaning services for local residences. At the date of

> Arnie, Becky, and Clay are equal partners in the ABC General Partnership. The three individuals each have a $120,000 tax basis in their partnership interest. For business reasons, the partnership needs to be changed into the ABC Corporation, and all thre

> ABC Company, a limited liability company (LLC) organized in the state of Florida, reports using a calendar tax yearend. The LLC chooses to be taxed as a partnership. Alex, Bob, and Carrie (all calendar year taxpayers) own ABC equally, and each has a bas

> The JKL Partnership has three equal partners, Jingjing, Kevin, and Latisha. Latisha sells her interest to Larry for $690,000. The partnership does not have a Sec. 754 election in effect. Just before the sale of Latisha’s interest, the p

> Patty pays $100,000 cash for Stan’s one third interest in the STU Partnership. The partnership has a Sec. 754 election in effect. Just before the sale of Stan’s interest, STU’s balance sheet appears a

> For each of the following independent situations, determine which partnership(s) (if any) terminate and which partnership(s) (if any) continue. a. The KLMN Partnership is created when the KL Partnership merges with the MN Partnership. The ownership of t

> Tyra has a zero basis in her partnership interest and a share in partnership liabilities, which are quite large. Explain how these facts will affect the taxation of her departure from the partnership using the following methods of terminating her interes

> Wendy, Xenia, and Yancy own 40%, 8%, and 52%, respectively, of the WXY Partnership. For each of the following independent situations occurring in the current year, determine whether the WXY Partnership terminates and, if so, the date on which the termina

> Josh holds a general partnership interest in the JLK Partnership having a $40,000 basis and a $60,000 FMV. The JLK Partnership is a limited partnership that engages in real estate activities. Diana has an interest in the CDE Partnership having a $20,000

> Amy, a one­third partner, retires from the AJS Partnership on January 1 of the current year. Her basis in her partnership interest is $120,000 including her share of liabilities. Amy receives $160,000 in cash from the partnership for her inter

> John has a 60% capital and profits interest in the JAS Partnership with a basis of $333,600, which includes his share of liabilities, when he decides to retire. Andrew and Stephen want to continue the partnership’s business. On the date

> Bruce died on June 1 of the current year. On the date of his death, he held a one­third interest in the ABC Partnership, which had a $100,000 basis including his share of liabilities. Under the partnership agreement, Bruce’s

> When Jerry died on April 16 of the current year, he owned a 40% interest in the JM Partnership, and Michael owns the remaining 60% interest. All his assets are held in his estate for a two­year period while the estate is being settled. Jerry&a

> Kim retires from the KLM Partnership on January 1 of the current year. At that time, her basis in the partnership is $75,000, which includes her share of liabilities. The partnership reports the following balance sheet: Explain the tax consequences (i.e

> Brian owns 40% of the ABC Partnership before his retirement on April 15 of the current year. On that date, his basis in the partnership interest is $40,000 including his share of liabilities. The partnership’s balance sheet on that date

> Suzanne retires from the BRS Partnership when the basis of her one third interest is $105,000, which includes her share of liabilities. At the time of her retirement, the partnership had the following assets: The partnership has $60,000 of liabilities w

> Alice, Bob, and Charles are one­third partners in the ABC Partnership. The partners originally formed the partnership with cash contributions, so no partner has precontribution gains or losses. Prior to Alice’s sale of her pa

> Can a partner recognize both a gain and a loss on the sale of a partnership interest? If so, under what conditions?

> Clay owned 60% of the CAP Partnership and sold one-half of his interest (30%) to Steve for $75,000 cash. Before the sale, Clay’s basis in his entire partnership interest was $168,000 including his $30,000 share of partnership liabilitie

> Pat, Kelly, and Yvette are equal partners in the PKY Partnership before Kelly sells her partnership interest. On January 1 of the current year, Kelly’s basis in her partnership interest, including her share of liabilities, was $35,000.

> The LQD Partnership distributes the following property to Larry in a distribution that liquidates Larry’s interest in the partnership. Assume that no Sec. 754 election is in effect. Larry’s basis in his partnership int

> The AB Partnership pays its only liability (a $100,000 mortgage) on April 1 of the current year and terminates that same day. Alison and Bob were equal partners in the partnership but have partnership bases immediately preceding these transactions of $11