Question: Consider the following information regarding the

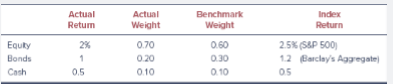

Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return of each sector of the manager’s portfolio in column 1, the fraction of the portfolio allocated to each sector in column 2, the benchmark or neutral sector allocations in column 3, and the returns of sector indices in column 4.

a. What was the manager’s return in the month? What was her over performance or underperformance?

b. What was the contribution of security selection to relative performance?

c. What was the contribution of asset allocation to relative performance? d. Confirm that the sum of selection and allocation contributions equals her total “excess†return relative to the bogey.

> With respect to hedge fund investing, the net return to an investor in a fund of funds would be lower than that earned from an individual hedge fund because of: a. Both the extra layer of fees and the higher liquidity offered. b. No reason; funds of fu

> Which of the following would be the most appropriate benchmark to use for hedge fund evaluation? a. A multifactor model. b. The S&P 500. c. The risk-free rate.

> Shaar (from the previous problem) has revised slightly her estimated earnings growth rate for Rio National and, using normalized (underlying trend) EPS, which is adjusted for temporary impacts on earnings, now wants to compare the current value of Rio Na

> Which of the following is most accurate in describing the problems of survivorship bias and backfill bias in the performance evaluation of hedge funds? a. Survivorship bias and backfill bias both result in upwardly biased hedge fund index returns. b. Su

> A hedge fund charges an incentive fee of 20% of any investment returns above the T-bill rate, which currently is 2% but is subject to a high water mark. In the first year, the fund suffers a loss of 8%. What rate of return must it earn in the second year

> A fund manages a $4.5 billion equity portfolio with a beta of 0.6. If the S&P contract multiplier is $50 and the index is currently at 3,000, how many contracts should the fund sell to make its overall position market neutral?

> Here are data on three hedge funds. Each fund charges its investors an incentive fee of 20% of total returns. Suppose initially that a fund of funds (FF) manager buys equal amounts of each of these funds and also charges its investors a 20% incentive fee

> Return to Problem 16. Now suppose that the manager misestimates the beta of Waterworks stock, believing it to be 0.50 instead of 0.75. The standard deviation of the monthly market rate of return is 5%. a. What is the standard deviation of the (now imper

> a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as Waterworks. Assume the residual returns (the e terms in Equations 20.1 and 20.2) on each of these stocks are independent of each

> The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 Index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month. a. If he holds a

> Suppose a hedge fund follows the following strategy: Each month it holds $100 million of an S&P 500 Index fund and writes one-month out-ofthe-money put options on $100 million of the index with exercise price 5% lower than the current value of the index.

> Log in to Connect, link to Chapter 20, and find there a spreadsheet containing monthly values of the S&P 500 Index. Suppose that in each month you had written an out-of-the-money put option on one unit of the index with an exercise price 5% lower than th

> Reconsider the hedge fund in the previous problem. Suppose it is January 1, the standard deviation of the fund’s annual returns is 50%, and the risk-free rate is 4%. The fund has an incentive fee of 20%, but its current high water mark is $66, and net as

> While valuing the equity of Rio National Corp. (from the previous problem), Katrina Shaar is considering the use of either free cash flow to the firm (FCFF) or free cash flow to equity (FCFE) in her valuation process. a. State two adjustments that Shaar

> A hedge fund with net asset value of $62 per share currently has a high water mark of $66. Is the value of its incentive fee more or less than it would be if the high water mark were $67?

> A hedge fund with $1 billion of assets charges a management fee of 2% and an incentive fee of 20% of returns over a money market rate, which currently is 5%. Calculate total fees, both in dollars and as a percent of assets under management, for portfolio

> Why is it harder to assess the performance of a hedge fund portfolio manager than that of a typical mutual fund manager?

> Would a market-neutral hedge fund be a good candidate for an investor’s entire retirement portfolio? If not, would there be a role for the hedge fund in the overall portfolio of such an investor?

> Much of this chapter was written from the perspective of a U.S. investor. But suppose you are advising an investor living in a small country (choose one to be concrete). How might the lessons of this chapter need to be modified for such an investor?

> If you were to invest $10,000 in the British bills of Problem 7, how would you lock in the dollar-denominated return?

> f the current exchange rate is $1.35/£, the one-year forward exchange rate is $1.45/£, and the interest rate on British government bills is 3% per year, what risk-free dollar-denominated return can be locked in by investing in the British bills?

> Calculate the contribution to total performance from currency, country, and stock selection for the manager in the example below. All exchange rates are expressed as units of foreign currency that can be purchased with 1 U.S. dollar.

> Now suppose the investor in Problem 3 also sells forward £5,000 at a forward exchange rate of $2.10/£. a. Recalculate the dollar-denominated returns for each scenario. b. What happens to the standard deviation of the dollardenominated return? Compare i

> If each of the nine outcomes in Problem 3 is equally likely, find the standard deviation of both the pound- and dollar denominated rates of return.

> Rio National Corp. is a U.S.-based company and the largest competitor in its industry. Tables 13.5–13.8 present financial statements and related information for the company. Table 13.9 presents relevant industry and market data. The por

> Suppose a U.S. investor wishes to invest in a British firm currently selling for £40 per share. The investor has $10,000 to invest, and the current exchange rate is $2/£. a. How many shares can the investor purchase? b. Fill i

> In Figure 19.2, we provide stock market returns in both local and dollar-denominated terms. Which of these is more relevant? What does this have to do with whether the foreign exchange risk of an investment has been hedged?

> Do you agree with the following claim? “U.S. companies with global operations can give you international diversification.” Think about both business risk and foreign exchange risk.

> Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 6%, and the market’s average return was 14%. Performance is measured using an index model regression on excess re

> Based on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B are 12% and 16%, respectively. The beta of A is 0.7, while that of B is 1.4. The T-bill rate is currently 5%, whereas the expected rate of ret

> A manager buys three shares of stock today and then sells one of those shares each year for the next three years. His actions and the price history of the stock are summarized below. The stock pays no dividends. a. Calculate the time-weighted geometric a

> XYZ’s stock price and dividend history are as follows: An investor buys three shares of XYZ at the beginning of 2019, buys another two shares at the beginning of 2020, sells one share at the beginning of 2021, and sells all four remaini

> Consider the rate of return of stocks ABC and XYZ a. Calculate the arithmetic average return on these stocks over the sample period. b. Which stock has greater dispersion around the mean return? c. Calculate the geometric average returns of each stock.

> Suppose the value of your portfolio will either double or fall by half with equal probability in any particular year. a. What is the expected value of the portfolio after one year? b. What is the expected value of the arithmetic average return on the p

> When will the dollar-weighted return on a risky investment exceed the geometric return? When will it be lower?

> Janet Ludlow’s firm requires all its analysts to use a twostage DDM and the CAPM to value stocks. Using these measures, Ludlow has valued QuickBrush Company at $63 per share. She now must value SmileWhite Corporation. a. Calculate the

> Go to Kenneth French’s data library site at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. Select two industry portfolios of your choice and download 36 months of data. Download other data from the site as needed to perform th

> Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Is it possible for a positive alpha to be associated with inferior performance? Explain.

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Bill Smith is evaluating the performance of four large-cap equity portfolios: Funds A, B, C, and D. As part of his analysis, Smith computed the Sharpe ratio and Treynor’s measure for all four funds. Based on his finding, the ranks assig

> During a particular year, the T-bill rate was 6%, the market return was 14%, and a portfolio manager with beta of 0.5 realized a return of 10%. What was the manager’s alpha?

> Does the use of universes of managers with similar investment styles to evaluate relative investment performance overcome the statistical problems associated with instability of beta or total variability?

> Peninsular Research is initiating coverage of a mature manufacturing industry. John Jones, CFA, head of the research department, gathered the following fundamental industry and market data to help in his analysis: a. Compute the price-to-earnings (P0/E1)

> Conventional wisdom says that one should measure a manager’s investment performance over an entire market cycle. What arguments support this convention? What arguments contradict it?

> A global equity manager is assigned to select stocks from a universe of large stocks throughout the world. The manager will be evaluated by comparing her returns to the return on the MSCI World Market Portfolio, but she is free to hold stocks from variou

> Evaluate the market timing and security selection abilities of four managers whose performances are plotted in the accompanying diagrams.

> A household savings-account spreadsheet shows the following entries for the first day of each month: Use the Excel function XIRR to calculate the monthly dollar-weighted average return for this period.

> It is now January. The current annual interest rate is 3% . The June futures price for gold is $1,246.30, while the December futures price is $1,251. Is there an arbitrage opportunity here? If so, how would you exploit it?

> Suppose the value of the S&P 500 Stock Index is currently $3,000. a. If the one-year T-bill rate is 3% and the expected dividend yield on the S&P 500 is 2%, what should the one-year maturity futures price be? b. What if the T-bill rate is less than the

> What is the difference in cash flow between short-selling an asset and entering a short futures position?

> Why might individuals purchase futures contracts rather than the underlying asset?

> a. Turn to Figure 17.1 and locate the E-Mini contract on the Standard & Poor’s 500 Index. If the margin requirement is 10% of the futures price times the multiplier of $50, how much must you deposit with your broker to buy one December contract? b. If t

> Phoebe Black’s investment club wants to buy the stock of either NewSoft, Inc. or Capital Corp. In this connection, Black prepared the following table. You have been asked to help her interpret the data, based on your forecast for a heal

> A newly issued bond paying a semiannual coupon has the following characteristics: a. Calculate modified duration using the information above. b. Explain why modified duration is a better measure than maturity when calculating the bond’

> You purchase a Treasury-bond futures contract with an initial margin requirement of 15% and a futures price of $115,098. The contract is traded on a $100,000 underlying par value bond. If the futures price falls to $108,000, what will be the percentage l

> A one-year gold futures contract is selling for $1,558. Spot gold prices are $1,500 and the one-year risk-free rate is 2%. a. According to spot-futures parity, what should be the futures price? b. What risk-free strategy can investors use to take advan

> The one-year futures price on a particular stock-index portfolio is 2,240, the stock index currently is 2,200, the one-year riskfree interest rate is 3%, and the year-end dividend that will be paid on a $2,200 investment in the index portfolio is $22. (L

> A corporation has issued a $10 million issue of floating-rate bonds on which it pays an interest rate 1% over the LIBOR rate. The bonds are selling at par value. The firm is worried that rates are about to rise, and it would like to lock in a fixed inter

> a. How would your hedging strategy in the previous problem change if, instead of holding an indexed portfolio, you hold a portfolio of only one stock with a beta of 0.6? b. How many contracts would you now choose to sell? Would your hedged position be r

> The S&P 500 Index is currently at 3,000. You manage a $15 million indexed equity portfolio. The S&P 500 futures contract has a multiplier of $50. a. If you are temporarily bearish on the stock market, how many contracts should you sell to fully elimina

> A corporation plans to issue $10 million of 10-year bonds in three months. At current yields, the bonds would have modified duration of eight years. The T-note futures contract is selling at F0 = 100 and has modified duration of six years. How can the fi

> A manager is holding a $1 million bond portfolio with a modified duration of eight years. She would like to hedge the risk of the portfolio by short-selling Treasury bonds. The modified duration of T-bonds is 10 years. How many dollars’ worth of T-bonds

> You are a corporate treasurer who will purchase $1 million of bonds for the sinking fund in three months. You believe rates soon will fall and would like to repurchase the company’s sinking fund bonds, which currently are selling below par, in advance of

> The multiplier for a futures contract on a stock market index is $50. The maturity of the contract is one year, the current level of the index is 3,000, and the risk-free interest rate is 0.2% per month. The dividend yield on the index is 0.1% per month.

> Christie Johnson, CFA, has been assigned to analyze Sundanci using the constant-dividend-growth price– earnings (P/E) ratio model. Johnson assumes that Sundanci’s earnings and dividends will grow at a constant rate of 13%. a. Calculate the P/E ratio base

> The current level of the S&P 500 is 3,000. The dividend yield on the S&P 500 is 2%. The risk-free interest rate is 1%. What should be the price of a one-year maturity futures contract?

> The margin requirement on the S&P 500 futures contract is 10%, and the stock index is currently 3,000. Each contract has a multiplier of $50. a. How much margin must be put up for each contract sold? b. If the futures price falls by 1% to 2,970, what w

> What type of interest rate swap would be appropriate for a speculator who believes interest rates soon will fall?

> Desert Trading Company has issued $100 million worth of longterm bonds at par at a fixed rate of 7%. The firm then enters into an interest rate swap where it pays LIBOR and receives a fixed 6% on notional principal of $100 million. What is the firm’s eff

> a. How should the parity condition (Equation 17.2) for stocks be modified for futures contracts on Treasury bonds? What should play the role of the dividend yield in that equation? b. In an environment with an upward-sloping yield curve, should Tbond fu

> Suppose the S&P 500 Index portfolio pays a dividend yield of 2% annually. The index currently is 3,000. The T-bill rate is 3%, and the S&P futures price for delivery in one year is $3,045. Construct an arbitrage strategy to exploit the mispricing and sho

> The multiplier for a futures contract on the stock-market index is $50. The maturity of the contract is one year, the current level of the index is 3,000, and the risk-free interest rate is 0.5% per month. The dividend yield on the index is 0.2% per mont

> One Chicago has just introduced a new single stock futures contract on the stock of Brandex, a company that currently pays no dividends. Each contract calls for delivery of 1,000 shares of stock in one year. The T-bill rate is 4% per year. a. If Brandex

> The Excel Applications box in the chapter (available in Connect; link to Chapter 17 material) shows how to use the spot-futures parity relationship to find a “term structure of futures prices,” that is, futures prices for various maturity dates. a. Supp

> a. A single stock futures contract on a nondividend-paying stock with current price $150 has a maturity of one year. If the T-bill rate is 3%, what should the futures price be? b. What should the futures price be if the maturity of the contract is three

> At Litchfield Chemical Corp. (LCC), a director of the company said that the use of dividend discount models by investors is “proof ” that the higher the dividend, the higher the stock price. a. Using a constant-growth dividend discount model as a basis

> A stock will pay a dividend of D dollars in one year, which is when a futures contract matures. Consider the following strategy: Buy the stock, short a futures contract on the stock, and borrow S0 dollars, where S0 is the current price of the stock. a.

> On January 1, you sold one February maturity S&P 500 Index futures contract at a futures price of 3,000. If the futures price is 3,050 at contract maturity, what is your profit? The contract multiplier is $50

> a. Calculate the value of a call option on the stock in the previous problem with an exercise price of 110. b. Verify that the put-call parity relationship is satisfied by your answers to both Problems 8 and 9. (Do not use continuous compounding to calc

> We will derive a two-state put option value in this problem. Data: S0 = 100; X = 110; 1 + r = 1.10. The two possibilities for ST are 130 and 80. a. Show that the range of S is 50 while that of P is 30 across the two states. What is the hedge ratio of th

> Show that Black-Scholes call option hedge ratios increase as the stock price increases. Consider a one-year option with exercise price $50 on a stock with annual standard deviation 20%. The Tbill rate is 3% per year. Find N(d1) for stock prices (a) $45,

> Reconsider the determination of the hedge ratio in the two-state model (Section 16.2), where we showed that one-third share of stock would hedge one option. What would be the hedge ratio for each of the following exercise prices: (a) $120; (b) $110; (

> In each of the following questions, you are asked to compare two options with parameters as given. The risk-free interest rate for all cases should be assumed to be 6%. Assume the stocks on which these options are written pay no dividends. a. Which put

> a. Return to Problem 37. What will be the payoff to the put, Pu, if the stock goes up? b. What will be the payoff, Pd, if the stock price falls? c. Value the put option using the risk-neutral shortcut described in the On the Market Front box. Confirm t

> Return to Problem 35. Value the call option using the risk-neutral shortcut described in the On the Market Front box. Confirm that your answer matches the value you get using the two-state approach.

> Use the put-call parity relationship to demonstrate that an at-the-money European call option on a nondividend-paying stock must cost more than an at-the-money put option. Show that the prices of the put and call will be equal if X = S0(1 + r)T.

> The following questions have appeared on CFA examinations a. Which one of the following statements best expresses the central idea of countercyclical fiscal policy? Planned government deficits are appropriate during economic booms, and planned surpluses

> You build a binomial model with one period and assert that over the course of a year, the stock price will either rise by a factor of 1½ or fall by a factor of ⅔. What is your implicit assumption about the volatility of the stock’s rate of return over th

> Suppose you are attempting to value a one-year maturity option on a stock with volatility (i.e., annualized standard deviation) of σ = 0.40. What would be the appropriate values for u and d if your binomial model is set up using the following? a. One pe

> We showed in the chapter that the value of a call option increases with the volatility of the stock. Is this also true of put option values? Use the putcall parity relationship as well as a numerical example to demonstrate your answer. (

> You would like to be holding a protective put position on the stock of XYZ Co. to lock in a guaranteed minimum value of $100 at year-end. XYZ currently sells for $100. Over the next year, the stock price will either increase by 10% or decrease by 10%. Th

> You are a provider of portfolio insurance and are establishing a four-year program. The portfolio you manage is currently worth $100 million, and you promise to provide a minimum return of 0%. The equity portfolio has a standard deviation of 25% per year

> a. Return to Example 16.1. Use the binomial model to value a one-year European put option with exercise price $110 on the stock in that example. b. Show that your solution for the put price satisfies put-call parity.

> Consider an increase in the volatility of the stock in the previous problem. Suppose that if the stock increases in price, it will increase to $130, and that if it falls, it will fall to $70. Show that the value of the call option is higher than the valu

> You are attempting to value a call option with an exercise price of $100 and one year to expiration. The underlying stock pays no dividends, its current price is $100, and you believe it has a 50% chance of increasing to $120 and a 50% chance of decreasi

> You are very bullish (optimistic) on stock EFG, much more so than the rest of the market. In each question, choose the portfolio strategy that will give you the biggest dollar profit if your bullish forecast turns out to be correct. Explain your answer.