Question: The following is part of the computer

The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 Index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2% over the coming month.

a. If he holds a $6 million portfolio of Waterworks stock and wishes to hedge market exposure for the next month using one-month maturity S&P 500 futures contracts, how many contracts should he enter? Should he buy or sell contracts? The S&P 500 currently is at 3,000 and the contract multiplier is $50.

b. What is the standard deviation of the monthly return of the hedged portfolio? c. Assuming that monthly returns are approximately normally distributed, what is the probability that this market-neutral strategy will lose money over the next month? Assume the risk-free rate is 0.5% per month.

> What is the duration of the bond in the previous problem if coupons are paid annually? Explain why the duration changes in the direction it does.

> Find the duration of a bond with settlement date May 27, 2018, and maturity date November 15, 2027. The coupon rate of the bond is 7%, and the bond pays coupons semiannually. The bond is selling at a yield to maturity of 8%. You can use Spreadsheet 11.2,

> You are managing a portfolio of $1 million. Your target duration is 10 years, and you can choose from two bonds: a zero-coupon bond with maturity five years and a perpetuity, each currently yielding 5%. a. How much of (i) the zero-coupon bond and (ii) t

> Spice asks Meyers (see previous problem) to quantify price changes from changes in interest rates. To illustrate, Meyers computes the value change for the fixed-rate note in the table. Specifically, he assumes an increase in the level of interest rate of

> Frank Meyers, CFA, is a fixed-income portfolio manager for a large pension fund. A member of the Investment Committee, Fred Spice, is very interested in learning about the management of fixed-income portfolios. Spice has approached Meyers with several qu

> Pension funds pay lifetime annuities to recipients. If a firm remains in business indefinitely, the pension obligation will resemble a perpetuity. Suppose, therefore, that you are managing a pension fund with obligations to make perpetual payments of $2

> You will be paying $10,000 a year in tuition expenses at the end of the next two years. Bonds currently yield 8%. a. What are the present value and duration of your obligation? b. What maturity zero-coupon bond would immunize your obligation? c. Suppo

> Long-term Treasury bonds currently are selling at yields to maturity of nearly 6%. You expect interest rates to fall. The rest of the market thinks that they will remain unchanged over the coming year. In each question, choose the bond that will provide

> Rank the interest rate sensitivity of the following pairs of bonds. a. Bond A is a 6% coupon, 20-year-maturity bond selling at par value. Bond B is a 6% coupon, 20-year-maturity bond selling below par value. b. Bond A is a 20-year, noncallable coupon b

> Jones Group has been generating stable after-tax return on equity (ROE) despite declining operating income. Explain how it might be able to maintain its stable after-tax ROE.

> You own a fixed-income asset with a duration of five years. If the level of interest rates, which is currently 8%, goes down by 10 basis points, how much do you expect the price of the asset to go up (in percentage terms)?

> If the plan in the previous problem wants to fully fund and immunize its position, how much of its portfolio should it allocate to one-year zero-coupon bonds and perpetuities, respectively, if these are the only two assets funding the plan?

> A pension plan is obligated to make disbursements of $1 million, $2 million, and $1 million at the end of each of the next three years, respectively. Find the duration of the plan’s obligations if the interest rate is 10% annually.

> A nine-year bond paying coupons annually has a yield of 10% and a duration of 7.194 years. If the bond’s yield changes by 50 basis points, what is the percentage change in the bond’s price?

> a. Find the duration of a 6% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 6%. b. What is the duration if the yield to maturity is 10%?

> Short-term interest rates are more volatile than long-term rates. Despite this, the rates of return of long-term bonds are more volatile than returns on short-term securities. How can these two empirical observations be reconciled?

> Is the decrease in a bond’s price corresponding to an increase in its yield to maturity more or less than the price increase resulting from a decrease in yield of equal magnitude?

> You are being interviewed for a job as a portfolio manager at an investment counseling partnership. As part of the interview, you are asked to demonstrate your ability to develop investment portfolio policy statements for the clients listed below: a. A

> Under the flat tax (Spreadsheet 21.4), will a 1% increase in ROR offset a 1% increase in the tax rate?

> What savings rate from real income (Spreadsheet 21.3) will produce the same retirement annuity as a 15% savings rate from nominal income?

> To continue with Sundanci, Abbey Naylor, CFA, has been directed to determine the value of Sundanci’s stock using the free cash flow to equity (FCFE) model. Naylor believes that Sundanci’s FCFE will grow at 27% for two years and 13% thereafter. Capital ex

> With a 3% inflation rate (Spreadsheet 21.2), by how much would your retirement annuity grow if you increase the savings rate by 1%? Is the benefit greater in the face of inflation?

> With no taxes or inflation (Spreadsheet 21.1), what would be your retirement annuity if you increase the savings rate by 1%?

> Why does a progressive tax code produce a retirement annuity for a middle-class household that is similar to that which would follow from a flat tax?

> What is the insurance aspect of the Social Security annuity?

> What type of investors would be interested in a target date retirement fund? Why?

> The same ship owner advertises a tariff whereby the freight charged per pound for all cargo will be the same. What kind of cargo can the ship owner expect to attract?

> Give another example of a moral hazard problem.

> In addition to expected longevity, what traits might affect an individual’s demand for a life annuity?

> Give another example of adverse selection

> Project your Social Security benefits with the parameters of Section 21.6.

> Helen Morgan, CFA, has been asked to use the dividend discount model to determine the value of Sundanci, Inc. Morgan anticipates that Sundanci’s earnings and dividends will grow at 32% for two years and 13% thereafter.Calculate the curr

> What is the trade-off between ROR and the rate of inflation with a Roth plan under a progressive tax (Spreadsheet 21.8)?

> Verify that the traditional tax shelter with a progressive tax (Spreadsheet 21.7) acts as a hedge. Compare the effect of a decline of 2% in the ROR to an increase of 2% in ROR.

> With a progressive tax (Spreadsheet 21.6), compare the effects of an increase of 1% in the lowest tax bracket to an increase of 1% in the highest tax bracket

> With a traditional tax shelter (Spreadsheet 21.5), compare the effect on real consumption during retirement of a 1% increase in the rate of inflation to a 1% increase in the tax rate

> A ship owner is attempting to insure an old vessel for twice its current market value. Is this an adverse selection or moral hazard issue?

> Why is it harder to assess the performance of a hedge fund portfolio manager than that of a typical mutual fund manager?

> How might the incentive fee of a hedge fund affect the manager’s proclivity to take on high-risk assets in the portfolio?

> Which of the following hedge fund types is most likely to have a return that is closest to risk free? a. A market-neutral hedge fund. b. An event-driven hedge fund. c. A long-short hedge fund.

> With respect to hedge fund investing, the net return to an investor in a fund of funds would be lower than that earned from an individual hedge fund because of: a. Both the extra layer of fees and the higher liquidity offered. b. No reason; funds of fu

> Which of the following would be the most appropriate benchmark to use for hedge fund evaluation? a. A multifactor model. b. The S&P 500. c. The risk-free rate.

> Shaar (from the previous problem) has revised slightly her estimated earnings growth rate for Rio National and, using normalized (underlying trend) EPS, which is adjusted for temporary impacts on earnings, now wants to compare the current value of Rio Na

> Which of the following is most accurate in describing the problems of survivorship bias and backfill bias in the performance evaluation of hedge funds? a. Survivorship bias and backfill bias both result in upwardly biased hedge fund index returns. b. Su

> A hedge fund charges an incentive fee of 20% of any investment returns above the T-bill rate, which currently is 2% but is subject to a high water mark. In the first year, the fund suffers a loss of 8%. What rate of return must it earn in the second year

> A fund manages a $4.5 billion equity portfolio with a beta of 0.6. If the S&P contract multiplier is $50 and the index is currently at 3,000, how many contracts should the fund sell to make its overall position market neutral?

> Here are data on three hedge funds. Each fund charges its investors an incentive fee of 20% of total returns. Suppose initially that a fund of funds (FF) manager buys equal amounts of each of these funds and also charges its investors a 20% incentive fee

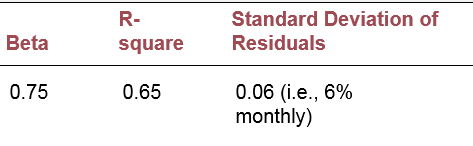

> Return to Problem 16. Now suppose that the manager misestimates the beta of Waterworks stock, believing it to be 0.50 instead of 0.75. The standard deviation of the monthly market rate of return is 5%. a. What is the standard deviation of the (now imper

> a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as Waterworks. Assume the residual returns (the e terms in Equations 20.1 and 20.2) on each of these stocks are independent of each

> Suppose a hedge fund follows the following strategy: Each month it holds $100 million of an S&P 500 Index fund and writes one-month out-ofthe-money put options on $100 million of the index with exercise price 5% lower than the current value of the index.

> Log in to Connect, link to Chapter 20, and find there a spreadsheet containing monthly values of the S&P 500 Index. Suppose that in each month you had written an out-of-the-money put option on one unit of the index with an exercise price 5% lower than th

> Reconsider the hedge fund in the previous problem. Suppose it is January 1, the standard deviation of the fund’s annual returns is 50%, and the risk-free rate is 4%. The fund has an incentive fee of 20%, but its current high water mark is $66, and net as

> While valuing the equity of Rio National Corp. (from the previous problem), Katrina Shaar is considering the use of either free cash flow to the firm (FCFF) or free cash flow to equity (FCFE) in her valuation process. a. State two adjustments that Shaar

> A hedge fund with net asset value of $62 per share currently has a high water mark of $66. Is the value of its incentive fee more or less than it would be if the high water mark were $67?

> A hedge fund with $1 billion of assets charges a management fee of 2% and an incentive fee of 20% of returns over a money market rate, which currently is 5%. Calculate total fees, both in dollars and as a percent of assets under management, for portfolio

> Why is it harder to assess the performance of a hedge fund portfolio manager than that of a typical mutual fund manager?

> Would a market-neutral hedge fund be a good candidate for an investor’s entire retirement portfolio? If not, would there be a role for the hedge fund in the overall portfolio of such an investor?

> Much of this chapter was written from the perspective of a U.S. investor. But suppose you are advising an investor living in a small country (choose one to be concrete). How might the lessons of this chapter need to be modified for such an investor?

> If you were to invest $10,000 in the British bills of Problem 7, how would you lock in the dollar-denominated return?

> f the current exchange rate is $1.35/£, the one-year forward exchange rate is $1.45/£, and the interest rate on British government bills is 3% per year, what risk-free dollar-denominated return can be locked in by investing in the British bills?

> Calculate the contribution to total performance from currency, country, and stock selection for the manager in the example below. All exchange rates are expressed as units of foreign currency that can be purchased with 1 U.S. dollar.

> Now suppose the investor in Problem 3 also sells forward £5,000 at a forward exchange rate of $2.10/£. a. Recalculate the dollar-denominated returns for each scenario. b. What happens to the standard deviation of the dollardenominated return? Compare i

> If each of the nine outcomes in Problem 3 is equally likely, find the standard deviation of both the pound- and dollar denominated rates of return.

> Rio National Corp. is a U.S.-based company and the largest competitor in its industry. Tables 13.5–13.8 present financial statements and related information for the company. Table 13.9 presents relevant industry and market data. The por

> Suppose a U.S. investor wishes to invest in a British firm currently selling for £40 per share. The investor has $10,000 to invest, and the current exchange rate is $2/£. a. How many shares can the investor purchase? b. Fill i

> In Figure 19.2, we provide stock market returns in both local and dollar-denominated terms. Which of these is more relevant? What does this have to do with whether the foreign exchange risk of an investment has been hedged?

> Do you agree with the following claim? “U.S. companies with global operations can give you international diversification.” Think about both business risk and foreign exchange risk.

> Consider the two (excess return) index-model regression results for stocks A and B. The risk-free rate over the period was 6%, and the market’s average return was 14%. Performance is measured using an index model regression on excess re

> Based on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B are 12% and 16%, respectively. The beta of A is 0.7, while that of B is 1.4. The T-bill rate is currently 5%, whereas the expected rate of ret

> A manager buys three shares of stock today and then sells one of those shares each year for the next three years. His actions and the price history of the stock are summarized below. The stock pays no dividends. a. Calculate the time-weighted geometric a

> XYZ’s stock price and dividend history are as follows: An investor buys three shares of XYZ at the beginning of 2019, buys another two shares at the beginning of 2020, sells one share at the beginning of 2021, and sells all four remaini

> Consider the rate of return of stocks ABC and XYZ a. Calculate the arithmetic average return on these stocks over the sample period. b. Which stock has greater dispersion around the mean return? c. Calculate the geometric average returns of each stock.

> Suppose the value of your portfolio will either double or fall by half with equal probability in any particular year. a. What is the expected value of the portfolio after one year? b. What is the expected value of the arithmetic average return on the p

> When will the dollar-weighted return on a risky investment exceed the geometric return? When will it be lower?

> Janet Ludlow’s firm requires all its analysts to use a twostage DDM and the CAPM to value stocks. Using these measures, Ludlow has valued QuickBrush Company at $63 per share. She now must value SmileWhite Corporation. a. Calculate the

> Go to Kenneth French’s data library site at http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. Select two industry portfolios of your choice and download 36 months of data. Download other data from the site as needed to perform th

> Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Is it possible for a positive alpha to be associated with inferior performance? Explain.

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Primo Management Co. is looking at how best to evaluate the performance of its managers. Primo has been hearing more and more about benchmark portfolios and is interested in trying this approach. As such, the company hired Sally Jones, CFA, as a consulta

> Bill Smith is evaluating the performance of four large-cap equity portfolios: Funds A, B, C, and D. As part of his analysis, Smith computed the Sharpe ratio and Treynor’s measure for all four funds. Based on his finding, the ranks assig

> During a particular year, the T-bill rate was 6%, the market return was 14%, and a portfolio manager with beta of 0.5 realized a return of 10%. What was the manager’s alpha?

> Does the use of universes of managers with similar investment styles to evaluate relative investment performance overcome the statistical problems associated with instability of beta or total variability?

> Peninsular Research is initiating coverage of a mature manufacturing industry. John Jones, CFA, head of the research department, gathered the following fundamental industry and market data to help in his analysis: a. Compute the price-to-earnings (P0/E1)

> Conventional wisdom says that one should measure a manager’s investment performance over an entire market cycle. What arguments support this convention? What arguments contradict it?

> A global equity manager is assigned to select stocks from a universe of large stocks throughout the world. The manager will be evaluated by comparing her returns to the return on the MSCI World Market Portfolio, but she is free to hold stocks from variou

> Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return of each sector of the manager’s portfolio in column 1, the fraction of the portfolio allocated to

> Evaluate the market timing and security selection abilities of four managers whose performances are plotted in the accompanying diagrams.

> A household savings-account spreadsheet shows the following entries for the first day of each month: Use the Excel function XIRR to calculate the monthly dollar-weighted average return for this period.

> It is now January. The current annual interest rate is 3% . The June futures price for gold is $1,246.30, while the December futures price is $1,251. Is there an arbitrage opportunity here? If so, how would you exploit it?

> Suppose the value of the S&P 500 Stock Index is currently $3,000. a. If the one-year T-bill rate is 3% and the expected dividend yield on the S&P 500 is 2%, what should the one-year maturity futures price be? b. What if the T-bill rate is less than the

> What is the difference in cash flow between short-selling an asset and entering a short futures position?

> Why might individuals purchase futures contracts rather than the underlying asset?

> a. Turn to Figure 17.1 and locate the E-Mini contract on the Standard & Poor’s 500 Index. If the margin requirement is 10% of the futures price times the multiplier of $50, how much must you deposit with your broker to buy one December contract? b. If t

> Phoebe Black’s investment club wants to buy the stock of either NewSoft, Inc. or Capital Corp. In this connection, Black prepared the following table. You have been asked to help her interpret the data, based on your forecast for a heal

> A newly issued bond paying a semiannual coupon has the following characteristics: a. Calculate modified duration using the information above. b. Explain why modified duration is a better measure than maturity when calculating the bond’

> You purchase a Treasury-bond futures contract with an initial margin requirement of 15% and a futures price of $115,098. The contract is traded on a $100,000 underlying par value bond. If the futures price falls to $108,000, what will be the percentage l

> A one-year gold futures contract is selling for $1,558. Spot gold prices are $1,500 and the one-year risk-free rate is 2%. a. According to spot-futures parity, what should be the futures price? b. What risk-free strategy can investors use to take advan