Question: Refer to the financial statements for Samsung

Refer to the financial statements for Samsung in Appendix A. How much were its cash payments for treasury stock purchases for the year ended December 31, 2013?

Samsung’s financial statements from Appendix A:

Transcribed Image Text:

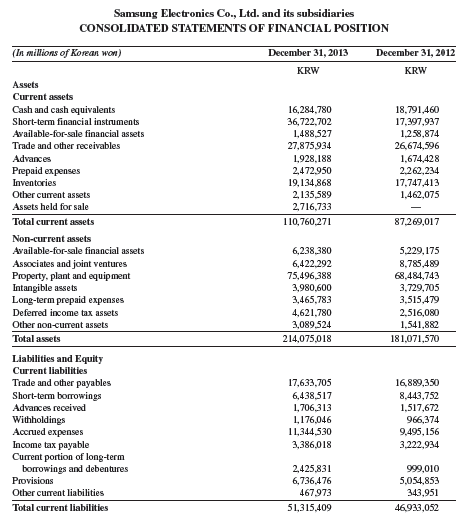

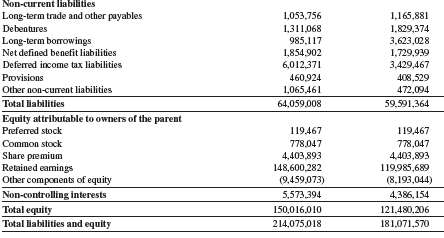

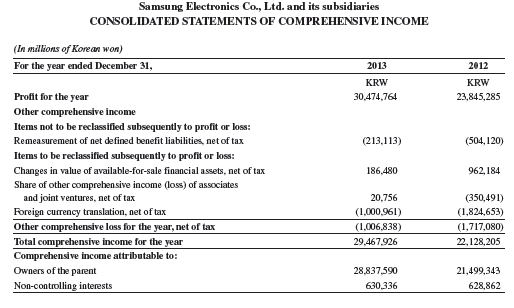

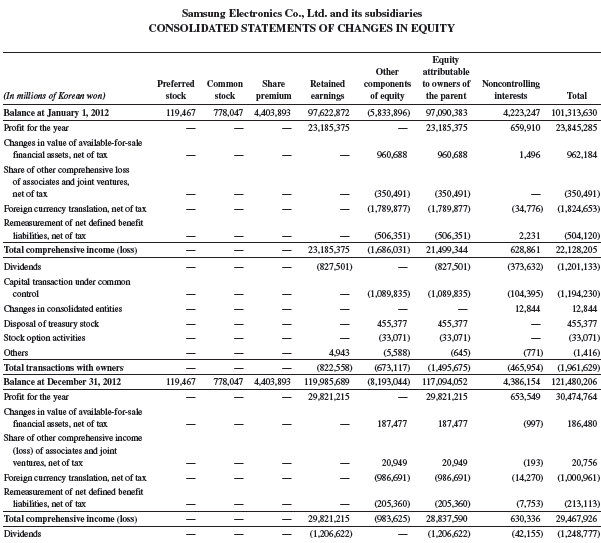

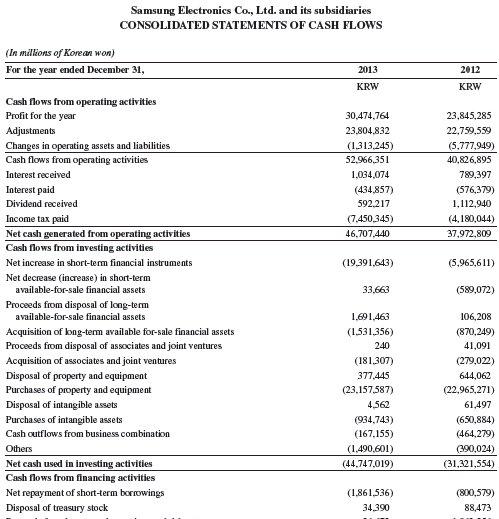

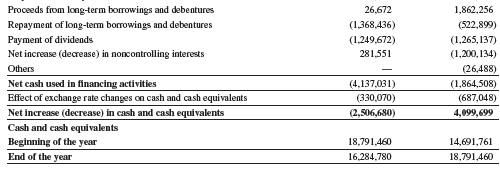

Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF FINANCIAL POSITION (In millions of Korean won) December 31, 2013 December 31, 2012 KRW KRW Assets Current assets Cash and cash equivalents Short-term financial instruments 16,284,780 36,722,702 1,488,527 27,875,934 18,791,460 17,397,937 1,258,874 26,674,596 Available-for-sale financial assets Trade and other receivables Advances 1,928,188 2,472,950 19,134,868 2,135,589 1,674,428 2,262,234 Prepaid expenses Inventories 17,747,413 1,462,075 Other current assets Assets held for sale 2,716,733 Total current assets 110,760,271 87,269,017 Non-current assets Available-for-sale financial assets 6,238,380 5,229,175 Associates and joint ventures Property, plant and equipment Intangible assets Long-term prepaid expenses 6,422,292 75,496,388 3,980,600 3,465,783 4,621,780 8,785,489 68,484,743 3,729,705 3,515,479 2,516,080 Deferred income tax assets Other non-curent assets 3,089,524 1,541,882 Total assets 214,075,018 181,071,570 Liabilities and Equity Current liabilities Trade and other payables 17,633,705 16,889,350 Short-term borrowings 8,443,752 6,438,517 1,706,313 1,176,046 11,344,530 Advances received Withholdings Accrued expenses Income tax payable Current portion of long-term borrowings and debentures 1,517,672 966,374 9,495, 156 3,222,934 3,386,018 2,425,831 6,736,476 999,010 5,054,853 343,951 Provisions Other current liabilities 467,973 Total current liabilities 51,315,409 46,933,052 Non-current Iliabilities Long-term trade and other payables 1,053,756 1,165,881 debentures 1,311,068 1,829,374 3,623,028 1,729,939 3,429,467 Long-term borowings 985,117 Net defined benefit liabilities 1,854,902 6,012,371 Deferred income tax liabilities Provisions 460,924 408,529 472,094 Other non-curent liabilities 1,065,461 Total liabilities 64,059,008 59,591,364 Equity attributable to owners of the parent Preferred stock 119,467 119,467 Common stock 778,047 Share premium Retained eamings Other components of equity 4,403,893 148,600,282 (9,459,073) 778,047 4,403,893 119,985,689 (8,193,044) Non-controlling interests 5,573,394 4,386, 154 Total equity 150,016,010 121,480,206 Total liabilities and equity 214,075,018 181,071,570 Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF INCOME (In millions of Korean won) For the year ended December 31, 2013 2012 KRW KRW Revenue 228,692,667 201,103,613 Cost of sales 137,696,309 126,651,931 Gross profit Selling and administrative expenses Operating profit 90,996,358 74,451,682 54,211,345 45,402,344 36,785,013 29,049,338 Other non-operating income 2,429,551 1,552,989 Other non-operating expense 1,614,048 1,576,025 Share of profit of associates and joint ventures 504,063 986,611 Finance income 8,014,672 7,836,554 Finance costs 7,754,972 7,934,450 Profit before income tax 38,364,279 29,915,017 Income tax expense 7,889,515 6,069,732 Profit for the year 30,474,764 23,845,285 Profit attributable to owners of the parent 29,821,215 23,185,375 Profit attributable to non-controlling interests 653,549 659,910 Eamings per share for profit attributable to owners of the parent (in Korean Won) -Basic 197,841 154,020 -Diluted 197,800 153,950 Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (In millions of Korean won) For the year ended December 31, 2013 2012 KRW KRW Profit for the year 30,474,764 23,845,285 Other comprehensive income Items not to be reclassifled subsequently to profit or loss: Remeasurement of net defined benefit liabilities, net of tax (213,113) (504, 120) Items to be reclassified subsequently to profit or loss: Changes in value of available-for-sale financial assets, net of tax 186,480 962, 184 Share of other comprehensive income (loss) of associates and joint ventures, net of tax 20,756 (350,491) Foreign currency translation, net of tax (1,000,961) (1,824,653) Other comprehensive loss for the year, net of tax Total comprehensive income for the year Comprehensive income attributable to: (1,006,838) (1,717,080) 29,467,926 22,128,205 Owners of the parent 28,837,590 21,499,343 Non-controlling interests 630,336 628,862 Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY Equity attributable components to owners of Noncontrolling the parent Other Retained earnings Preferred Сommon Share (In millions of Korean won) stock stock premium of equity interests Total Balance at January 1, 2012 Profit for the year 119,467 778,047 4,403,893 97,622,872 (5,833,896) 97,090,383 4,223,247 101,313,630 23,185,375 23,185,375 659,910 23,845,285 Changes in value of available-for-sake financial assets, net of tax 960,688 960,688 1,496 962,184 Share of other comprehensive los of associates and joint ventures, net of tax (350,491) (350,491) (350,491) Foreign currency translation, net of tax (1,789,877) (1,789,877) (34,776) (1,824,653) Remezsurement of net defined benefit liabilities, net of tax (506,351) (506,351) 2,231 (504,120) Total comprehensive income (loss) 23,185,375 (1,686,031) 21,499,344 628,861 22,128,205 Dividends (827,501) (827,501) (373,632) (1,201,133) Capital transaction under common control (1,089,835) (1,089,835) (104,395) (1,194,230) Changes in consolidated entities 12,844 12,844 Disposal of treasury stock 455,377 455,377 455,377 Stock option activities (33,071) (33,071) (33,071) Others 4,943 (5,588) (645) (771) (1,416) Total transactions with owners (822,558) (673,117) (1,495,675) (8,193,044) 117,094,052 (465,954) (1,961,629) Balance at December 31, 2012 119,467 778,047 4,403,893 119,985,689 4,386,154 121,480,206 Profit for the year 29,821,215 29,821,215 653,549 30,474,764 Changes in value of available-for-sake financial ssets, net of tax 187,477 187,477 (997) 186,480 Share of other comprebensive income (loss) of associates and joint ventures, net of tax 20,949 20,949 (193) 20,756 Foreign currency translation, net of tax (986,691) (986,691) (14,270) (1,000,961) Remessurement of net defined benefit liabilities, net of tax (205,360) (205,360) (7,753) (213,113) Total comprehensive income (loss) 29,821,215 (983,625) 28,837,590 630,336 29,467,926 Dividends (1,206,622) (1,206,622) (42,155) (1,248,777) Capital transaction under common control (312,959) (312,959) 600,042 287,083 Changes in consolidated entities (918) (918) Disposal of treasury stock 41,817 41,817 41,817 Stock option activities (11,999) k11.999) (11,999) Others 737 737 (65) 672 Total transactions with owners (1,206,622) (282,404) (1,489,026) 556,904 (932,122) Balance at December 31, 2013 119,467 778,047 4,403,893 148,600,282 (9,459,073) 144,442,616 5,573,394 150,016,010 |||||E Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF CASH FLOWS (In millions of Korean won) For the year ended December 31, 2013 2012 KRW KRW Cash flows from operating activities Profit for the year 30,474,764 23,845,285 Adjustments 23,804,832 22,759,559 Changes in operating assets and liabilities (1,313,245) (5,777,949) Cash flows from operating activities 52,966,351 40,826,895 Interest received 1,034,074 789,397 Interest paid (434,857) (576,379) Dividend received 592,217 1,112,940 Income tax paid (7,450,345) (4,180,044) Net cash generated from operating activities 46,707,440 37,972,809 Cash flows from investing activities Net increase in short-tem financial instruments (19,391,643) (5,965,611) Net decrease (increase) in short-term available-for-sale financial assets 33,663 (589,072) Proceeds from disposal of long-tem available-for-sale financial assets 1,691,463 106,208 Acquisition of long-term available for-sale financial assets (1,531,356) (870,249) Proceeds from disposal of associates and joint ventures 240 41,091 Acquisition of associates and joint ventures (181,307) (279,022) Disposal of property and equipment 377,445 644,062 Purchases of property and equipment (23,157,587) (22,965,271) Disposal of intangible assets 4,562 61,497 Purchases of intangible assets Cash outflows from business combination (934,743) (650,884) (167,155) (464,279) Others (1,490,601) (390,024) Net cash used in investing activities Cash flows from financing activities (44,747,019) (31,321,554) Net repayment of short-term borrowings (1,861,536) (800,579) Disposal of treasury stock 34,390 88,473 Proceeds from long-term borrowings and debentures 26,672 1,862,256 Repayment of long-term borrowings and debentures Payment of dividends. (1,368,436) (522,899) (1,249,672) (1,265, 137) Net increase (decrease) in noncontrolling interests 281,551 (1,200, 134) Others (26,488) Net cash used in financing activities (4,137,031) (1,864,508) Effect of exchange rate changes on cash and cash equivalents (330,070) (687,048) Net increase (decrease) in cash and cash equivalents (2,506,680) 4,099,699 Cash and cash equi valents Beginning of the year End of the year 18,791,460 14,691,761 16,284,780 18,791,460

> Which of the following statements are true regarding dividends? ______ 1. Cash and stock dividends reduce retained earnings. ______ 2. Dividends payable is recorded at the time a cash dividend is declared. ______ 3. The date of record refers to the date

> Costs of $5,000 were incurred to acquire goods and make them ready for sale. The goods were shipped to the buyer (FOB shipping point) for a cost of $200. Additional necessary costs of $400 were incurred to acquire the goods. What is the buyer’s total cos

> Identify the inventory costing method best described by each of the following separate statements. Assume a period of increasing costs. ______ 1. Yields a balance sheet inventory amount often markedly less than its replacement cost. ______ 2. Results in

> Answer each of the following questions related to international accounting standards. a. Explain how the accounting for merchandise purchases and sales is different between accounting under IFRS versus U.S. GAAP. b. Income statements prepared under IFRS

> After all partnership assets have been converted to cash and all liabilities paid, the remaining cash should equal the sum of the balances of the partners’ capital accounts. Why?

> Listed below are various transactions that a company incurred during the current year. Indicate the impact on total stockholders’ equity for each scenario. Specifically state whether stockholders’ equity would “Increase,” “Decrease,” or have “No Effect”

> Of the following statements, which are true for the corporate form of organization? ______ 1. Ownership rights cannot be easily transferred. ______ 2. Owners have unlimited liability for corporate debts. ______ 3. Capital is more easily accumulated than

> Identify whether each description best applies to a periodic or a perpetual inventory system. ______ a. Updates the inventory account only at period-end. ______ b. Requires an adjusting entry to record inventory shrinkage. ______ c. Markedly increased in

> Answer each of the following related to international accounting standards. a. In general, how similar or different are the definitions and characteristics of current liabilities between IFRS and U.S. GAAP? b. Companies reporting under IFRS often referen

> Fancher organized a limited partnership and is the only general partner. Carley invested $20,000 in the partnership and was admitted as a limited partner with the understanding that she would receive 10% of the profits. After two unprofitable years, the

> The following legal claims exist for Huprey Co. Identify the accounting treatment for each claim as either (a) a liability that is recorded or (b) an item described in notes to its financial statements. 1. Huprey (defendant) estimates that a pending law

> Which of the following items are normally classified as current liabilities for a company that has a 15-month operating cycle? ______ 1. Portion of long-term note due in 15 months. ______ 2. Note payable maturing in 2 years. ______ 3. Note payable due

> For each item below indicate whether the statement describes a multiple-step income statement or a single-step income statement. a. Multiple-step income statement b. Single-step income statement 1. Shows detailed computations of net sales and other cost

> Enter the letter for each term in the blank space beside the definition that it most closely matches. A. Sales discount B. Credit period C. Discount period D. FOB destination E. FOB shipping point F. Gross profit I. Cash discount G. Merchandise inven

> On June 3, a company borrows $200,000 cash by giving its bank a 90-day, interest-bearing note. On the statement of cash flows, where should this be reported?

> If a partnership contract does not state the period of time the partnership is to exist, when does the partnership end?

> Refer to Samsung’s 2013 statement of cash flows in Appendix A. List its cash flows from operating activities, investing activities, and financing activities. Samsung’s Statement of Cash Flow from Appendix A: Sams

> Under what circumstances are long-term investments in debt securities reported at cost and adjusted for amortization of any difference between cost and maturity value?

> On a balance sheet, what valuation must be reported for debt securities classified as available-for-sale?

> If a company purchases its only long-term investments in available-for-sale debt securities this period and their fair value is below cost at the balance sheet date, what entry is required to recognize this unrealized loss?

> If a short-term investment in available-for-sale securities costs $10,000 and is sold for $12,000, how should the difference between these two amounts be recorded?

> On a balance sheet, what valuation must be reported for short-term investments in trading securities?

> Refer to the income statement of Samsung in Appendix A. How can you tell that it uses the consolidated method of accounting? Income Statement of Samsung from Appendix A: Samsung Electronics Co, Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF

> Refer to Google’s statement of comprehensive income. What was the amount of its 2013 change in net unrealized gains for its AFS investments? Google’s Statement of Comprehensive Income: Google Inc. CONSOLIDATED ST

> Refer to Apple’s statement of comprehensive income in Appendix A. What is the amount of foreign currency translation adjustment for the year ended September 28, 2013? Is this adjustment an unrealized gain or an unrealized loss? Apple&a

> If a U.S. company makes a credit sale to a foreign customer required to make payment in U.S. dollars, can the U.S. company have an exchange gain or loss on this sale?

> What is an employer’s unemployment merit rating? How are these ratings assigned to employers?

> What are two major challenges in accounting for international operations?

> Under what circumstances does a company prepare consolidated financial statements?

> In accounting for investments in equity securities, when should the equity method be used?

> Under what two conditions should investments be classified as current assets?

> What factors affect the market rates for bonds?

> What are the duties of a trustee for bondholders?

> What is the main difference between a bond and a share of stock?

> When can a lease create both an asset and a liability for the lessee?

> Refer to the statements for Google in Appendix A. For the year ended December 31, 2013, what is its debt-to-equity ratio? What does this ratio tell us? Google’s Financial Statements from Appendix A: Google Inc. CONSOLIDATE

> Refer to the statement of cash flows for Samsung in Appendix A. For the year ended December 31, 2013, what was the amount for repayment of long-term borrowings and debentures? Samsung’s Statement of Cash Flow from Appendix A: Sams

> Refer to Samsung’s recent balance sheet in Appendix A. What current liabilities related to income taxes are on its balance sheet? Explain the meaning of each income tax account identified. Samsung’s Balance Sheet from Appendix A: / /

> By what amount did Samsung’s long-term borrowings increase or decrease in 2013? Samsung’s Financial Statements from Appendix A: Samsung Electronics Co., Ltd. and its subsidiaries CONSOLIDATED STATEMENTS OF FI

> Refer to Apple’s annual report in Appendix A. Is there any indication that Apple has issued long-term debt? Apple’s Balance Sheet from Appendix A: Apple Inc. CONSOLIDATED BALANCE SHEETS (In millions, except numbe

> What is the issue price of a $2,000 bond sold at 98 1⁄4? What is the issue price of a $6,000 bond sold at 101 1⁄2?

> If you know the par value of bonds, the contract rate, and the market rate, how do you compute the bonds’ price?

> What is the main difference between notes payable and bonds payable?

> Why would an investor find convertible preferred stock attractive?

> What is the difference between the par value and the call price of a share of preferred stock?

> What is the preemptive right of common stockholders?

> What is the difference between authorized shares and outstanding shares?

> Who is responsible for directing a corporation’s affairs?

> Suppose that a company has a facility located where disastrous weather conditions often occur. Should it report a probable loss from a future disaster as a liability on its balance sheet? Explain.

> Refer to the 2013 balance sheet for Google in Appendix A. What is the par value per share of its preferred stock? Suggest a rationale for the amount of par value it assigned. Google’s Balance Sheet from Appendix A: Google Inc. CON

> Refer to Apple’s fiscal 2013 balance sheet in Appendix A. How many shares of common stock are authorized? How many shares of voting common stock are issued? Apple’s Balance Sheet from Appendix A:

> How are organization expenses reported?

> What is a stock option?

> How are EPS results computed for a corporation with a simple capital structure?

> Why do laws place limits on treasury stock purchases?

> How does the purchase of treasury stock affect the purchaser’s assets and total equity?

> Courts have ruled that a stock dividend is not taxable income to stockholders. What justifies this decision?

> Why is the term liquidating dividend used to describe cash dividends debited against paid-in capital accounts?

> Why are warranty liabilities usually recognized on the balance sheet as liabilities even when they are uncertain?

> What are organization expenses? Provide examples.

> George, Burton, and Dillman have been partners for three years. The partnership is being dissolved. George is leaving the firm, but Burton and Dillman plan to carry on the business. In the final settlement, George places a $75,000 salary claim against th

> What does the term unlimited liability mean when it is applied to partnership members?

> Allocation of partnership income among the partners appears on what financial statement?

> Assume that the Barnes and Ardmore partnership agreement provides for a two-third/one-third sharing of income but says nothing about losses. The first year of partnership operation resulted in a loss, and Barnes argues that the loss should be shared equa

> Assume that Amey and Lacey are partners. Lacey dies, and her son claims the right to take his mother’s place in the partnership. Does he have this right? Why or why not?

> Can partners limit the right of a partner to commit their partnership to contracts? Would such an agreement be binding (a) on the partners and (b) on outsiders?

> How does a general partnership differ from a limited partnership?

> Apple began as a partnership. What does the term mutual agency mean when applied to a partnership?

> Assume a partner withdraws from a partnership and receives assets of greater value than the book value of his equity. Should the remaining partners share the resulting reduction in their equities in the ratio of their relative capital balances or accordi

> Identify the main difference between (a) plant assets and current assets, (b) plant assets and inventory, and (c) plant assets and long-term investments.

> Kay, Kat, and Kim are partners. In a liquidation, Kay’s share of partnership losses exceeds her capital account balance. Moreover, she is unable to meet the deficit from her personal assets, and her partners shared the excess losses. Does this relieve Ka

> What determines the amount deducted from an employee’s wages for federal income taxes?

> Which payroll taxes are the employee’s responsibility and which are the employer’s responsibility?

> What is the current Medicare tax rate? This rate is applied to what maximum level of salary and wages?

> What is the combined amount (in percent) of the employee and employer Social Security tax rate? (Assume wages do not exceed $200,000 per year.)

> If $988 is the total of a sale that includes its sales tax of 4%, what is the selling price of the item only?

> What are the three important questions concerning the uncertainty of liabilities?

> What is an estimated liability?

> Refer to Samsung’s balance sheet in Appendix A. List Samsung’s current liabilities as of December 31, 2013. Samsung’s Balance Sheet from Appendix A: / /

> Refer to Google’s balance sheet in Appendix A. What accrued expenses (liabilities) does Google report at December 31, 2013? Google’s Balance Sheet from Appendix A: Google Inc. CONSOLIDATED BALANCE SHEETS (In mill

> What is the difference between ordinary repairs and extraordinary repairs? How should each be recorded?

> Why does the direct write-off method of accounting for bad debts usually fail to match revenues and expenses?

> Refer to Apple’s balance sheet in Appendix A. What is the amount of Apple’s accounts payable as of September 28, 2013? Apple’s Balance Sheet from Appendix A: Apple Inc. CONSOLIDATED BALANCE SHEE

> What amount of income tax is withheld from the salary of an employee who is single with two withholding allowances and earning $725 per week? What if the employee earned $625 and has no withholding allowances? (Use Exhibit 11A.6.) Exhibit 11A.6: SI

> What is a wage bracket withholding table?

> What is the difference between a current and a long-term liability?

> What accounting concept justifies charging low-cost plant asset purchases immediately to an expense account?

> Why is the Modified Accelerated Cost Recovery System not generally accepted for financial accounting purposes?

> Why is the cost of a lump-sum purchase allocated to the individual assets acquired?

> What is different between land and land improvements?

> Refer to the December 31, 2013, balance sheet of Samsung in Appendix A. What long-term assets discussed in this chapter are reported by the company? Samsung’s Balance Sheet from Appendix A: / Samsung Electronics Co., Ltd. and i

> What is the general rule for cost inclusion for plant assets?

> Assume that a company buys another business and pays for its goodwill. If the company plans to incur costs each year to maintain the value of the goodwill, must it also amortize this goodwill?

> Refer to Samsung’s balance sheet in Appendix A. What does it title its plant assets? What is the book value of its plant assets at December 31, 2013? Samsung’s Balance Sheet from Appendix A: / /

> Refer to Google’s recent balance sheet in Appendix A. What property, plant and equipment assets does Google list on its balance sheet? What is the book value of its total net property, plant and equipment assets at December 31, 2013? G

> On its recent balance sheet in Appendix A, Apple lists its plant assets as “Property, plant and equipment, net.” What does “net” mean in this title? Apple Balance Sheet from Appendi

> How is total asset turnover computed? Why would a financial statement user be interested in total asset turnover?

> What are the characteristics of an intangible asset?

> Is the declining-balance method an acceptable way to compute depletion of natural resources? Explain.

> What is the process of allocating the cost of natural resources to expense as they are used?