Question: In Problem 14, suppose that Douglas McDonnell

In Problem 14, suppose that Douglas McDonnell shareholders approve a 3-for-1 stock split on January 1, 2017. What is the new divisor for the index? Calculate the rate of return on the index for the year ending December 31, 2017, if Douglas McDonnell’s share price on January 1, 2018, is $39.33 per share.

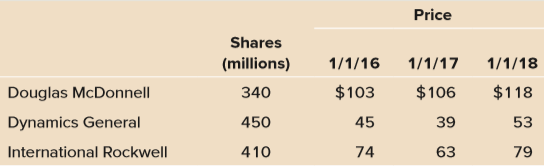

Data from Problem 14:

Suppose the following three defense stocks are to be combined into a stock index in January 2016 (perhaps a portfolio manager believes these stocks are an appropriate benchmark for his or her performance):

a. Calculate the initial value of the index if a price-weighting scheme is used.

b. What is the rate of return on this index for the year ending December 31, 2016? For the year ending December 31, 2017?

Transcribed Image Text:

Price Shares (millions) 1/1/16 1/1/17 1/1/18 Douglas McDonnell 340 $103 $106 $118 Dynamics General 450 45 39 53 International Rockwell 410 74 63 79

> A stock is currently priced at $53.87 and the futures on the stock that expire in six months have a price of $55.94. The risk-free rate is 5 percent and the stock is not expected to pay a dividend. Is there an arbitrage opportunity here? How would you ex

> Is it true that the NAV of a money market mutual fund never changes? How is this possible?

> A non-dividend-paying stock is currently priced at $48.15 per share. A futures contract maturing in five months has a price of $48.56 and the risk-free rate is 4 percent. Describe how you could make an arbitrage profit from this situation. How much could

> You have been assigned to implement a three-month hedge for a stock mutual fund portfolio that primarily invests in medium-sized companies. The mutual fund has a beta of 1.15 measured relative to the S&P Midcap 400, and the net asset value of the fund is

> You are short 15 gasoline futures contracts, established at an initial settle price of $2.085 per gallon, where each contract represents 42,000 gallons. Your initial margin to establish the position is $7,425 per contract and the maintenance margin is $6

> You are long 10 gold futures contracts, established at an initial settle price of $1,500 per ounce, where each contract represents 100 troy ounces. Your initial margin to establish the position is $12,000 per contract and the maintenance margin is $11,20

> Margin Call (LO2, CFA2) Suppose the initial margin on heating oil futures is $8,400, the maintenance margin is $7,200 per contract, and you establish a long position of 10 contracts today, where each contract represents 42,000 gallons. Tomorrow, the cont

> Calculate Jensen’s alpha for the fund, as well as its information ratio. Data for Problem 19: You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know

> You are constructing a portfolio of two assets, asset A and asset B. The expected returns of the assets are 12 percent and 15 percent, respectively. The standard deviations of the assets are 29 percent and 48 percent, respectively. The correlation betwee

> For the stock in Problem 13, what is the smallest expected gain over the next year with a probability of 1 percent? Does this number make sense? What does this tell you about stock return distributions? Data from Problem 13: A stock has an annual retur

> Landon Stevens is evaluating the expected performance of two common stocks, Furhman Labs, Inc., and Garten Testing, Inc. The risk-free rate is 4 percent, the expected return on the market is 11.5 percent, and the betas of the two stocks are 1.2 and 0.9,

> Consider the following information on Stocks I and II: The market risk premium is 8 percent and the risk-free rate is 5 percent. Which stock has the most systematic risk? Which one has the most unsystematic risk? Which stock is “riski

> Given that no-load funds are widely available, why would a rational investor pay a front-end load? More generally, why don’t fund investors always seek out funds with the lowest loads, management fees, and other fees?

> Fill in the following table, supplying all the missing information. Use this information to calculate the security’s beta.

> Suppose you observe the following situation: Assume these securities are correctly priced. Based on the CAPM, what is the expected return on the market? What is the risk-free rate? Security Beta Expected Return Peat Co. 1.05 12.3 Re-Peat Co. 0.90

> Asset W has an expected return of 12.0 percent and a beta of 1.1. If the risk-free rate is 4 percent, complete the following table for portfolios of asset W and a risk-free asset. Illustrate the relationship between portfolio expected return and portfoli

> You are going to invest in asset J and asset S. Asset J has an expected return of 13 percent and a standard deviation of 54 percent. Asset S has an expected return of 10 percent and a standard deviation of 19 percent. The correlation between the two asse

> In Problem 12, what is the standard deviation if the correlation is +1? 0? −1? As the correlation declines from +1 to −1 here, what do you see happening to portfolio volatility? Why? Data from Problem 12: Use the fol

> Suppose the yield to maturity on the bond in Problem 29 increases by 0.25 percent. What is the new price of the bond using duration? What is the new price of the bond using the bond pricing formula? What if the yield to maturity increases by 1 percent? B

> A Treasury bond with 8 years to maturity is currently quoted at 106:16. The bond has a coupon rate of 7.5 percent. What is the yield value of a 32nd for this bond?

> Fooling Company has a 10 percent callable bond outstanding on the market with 25 years to maturity, call protection for the next 10 years, and a call premium of $100. What is the yield to call (YTC) for this bond if the current price is 108 percent of pa

> Suppose you buy a 6 percent coupon bond today for $1,080. The bond has 10 years to maturity. What rate of return do you expect to earn on your investment? Two years from now, the YTM on your bond has increased by 2 percent, and you decide to sell. What p

> Bond J is a 4 percent coupon bond. Bond K is an 8 percent coupon bond. Both bonds have 10 years to maturity and have a YTM of 7 percent. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? What if rates sudde

> Refer to Table 1.1 for large-company stock and T-bill returns for the period 1973–1977: a. Calculate the observed risk premium in each year for the common stocks. b. Calculate the average returns and the average risk premium over this

> Both bond A and bond B have 6 percent coupons and are priced at par value. Bond A has 5 years to maturity, while bond B has 15 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in price of bond A? Of bond B? I

> Bond P is a premium bond with an 8 percent coupon, a YTM of 6 percent, and 15 years to maturity. Bond D is a discount bond with an 8 percent coupon, a YTM of 10 percent, and also 15 years to maturity. If interest rates remain unchanged, what do you expec

> A zero coupon bond with a 6 percent YTM has 20 years to maturity. Two years later, the price of the bond remains the same. What’s going on here?

> You observe that the current interest rate on short-term U.S. Treasury bills is 1.64 percent. You also read in the newspaper that the GDP deflator, which is a common macroeconomic indicator used by market analysts to gauge the inflation rate, currently i

> Suppose you purchase a $1,000 TIPS on January 1, 2016. The bond carries a fixed coupon of 1 percent. Over the first two years, semiannual inflation is 2 percent, 3 percent, 1 percent, and 2 percent, respectively. For each six-month period, calculate the

> Suppose the (quoted) yield on each of the six STRIPS increases by 0.05 percent. Calculate the percentage change in price for the one-year, three-year, and six-year STRIPS. Which one has the largest price change? Now suppose that the quoted price on each

> According to the pure expectations theory of interest rates, how much do you expect to pay for a one-year STRIPS on November 15, 2016? What is the corresponding implied forward rate? How does your answer compare to the current yield on a one-year STRIPS?

> Calculate the quoted yield for each of the STRIPS given in the table above. Does the market expect interest rates to go up or down in the future? Data for Problem 14: U.S. Treasury STRIPS, close of business November 15, 2015:

> Another technical indicator is the put/call ratio. The put/call ratio is the number of put options traded divided by the number of call options traded. The put/ call ratio can be constructed on the market or an individual stock. Below you will find the n

> Use the information from Problem 13 to calculate the three-day and five-day exponential moving averages for eBay and graph your results. Place two-thirds of the average weight on the most recent stock price. Are there any technical indications of the fut

> What is the difference between a futures contract and an option contract? Do the buyer of a futures contract and the buyer of an option contract have the same rights? What about the seller?

> Below you will find the closing stock prices for eBay over a three-week period. Calculate the simple three-day and five-day moving averages for the stock and graph your results. Are there any technical indications of the future direction of the stock pri

> A stock recently increased in price from $32 to $45. Using φ, what are the primary and secondary support areas for the stock?

> When a stock is going through a period of non constant growth for T periods, followed by constant growth forever, the residual income model can be modified as follows: where Al’s Infrared Sandwich Company had a book value of $12.95

> Given the information below for StartUp.Com, compute the expected share price at the end of 2017 using price ratio analysis. Year 2013 2014 2015 2016 Price N/A $ 68.12 $ 95.32 $104.18 EPS N/A -7.55 -4.30 -3.68 CFPS N/A -11.05 -8.20 -5.18 SPS N/A 4

> Given the information below for HooYah! Corporation, compute the expected share price at the end of 2017 using price ratio analysis. Assume that the historical average growth rates will remain the same for 2017. Year 2011 2012 2013 2014 2015 2016

> Given the information below for Seger Corporation, compute the expected share price at the end of 2017 using price ratio analysis. Assume that the historical average growth rates will remain the same for 2017. Year 2011 2012 2013 2014 2015 2016 Pric

> The dividend for Should I, Inc., is currently $1.25 per share. It is expected to grow at 20 percent next year and then decline linearly to a 5 percent perpetual rate beginning in four years. If you require a 15 percent return on the stock, what is the mo

> Suppose you want to replicate the performance of several stock indexes, some of which are price-weighted, others value-weighted, and still others equally weighted. Describe the investment strategy you need for each of the index types. Are any of the thre

> Another type of index is the geometric index. The calculation of a geometric index is similar to the calculation of a geometric return: 1 + R G = [(1 + R 1 )(1 + R 2 ) . . . (1 + R N )] 1/N The difference in the geometric index construction

> Historically there have been periods where a value-weighted index has a higher return than an equally weighted index and other periods where the opposite has occurred. Why do you suppose this would happen?

> Suppose a share of stock is selling for $100. A put and a call are offered, both with $100 strike prices and nine months to maturity. Intuitively, which do you think is more valuable?

> Escambia Beach Systems is offering 1,000 shares in a Dutch auction IPO. The following bids have been received: How much will Bidder A have to spend to purchase all of the shares that have been allocated to her? Bidder Quantity Price

> In addition to price-weighted and value-weighted indexes, an equally weighted index is one in which the index value is computed from the average rate of return of the stocks comprising the index. Equally weighted indexes are frequently used by financial

> Repeat Problem 14 if a value-weighted index is used. Assume the index is scaled by a factor of 10 million; that is, if the average firm’s market value is $5 billion, the index would be quoted as 500. Data from Problem 14: Suppose the

> Suppose the following three defense stocks are to be combined into a stock index in January 2016 (perhaps a portfolio manager believes these stocks are an appropriate benchmark for his or her performance): a. Calculate the initial value of the index

> You invested $1,250,000 with a market-neutral hedge fund manager. The fee structure is 2/20, and the fund has a high-water-mark provision. Suppose the first year the fund manager loses 10 percent and the second year she gains 20 percent. What are the man

> You purchased 2,000 shares in the New Pacific Growth Fund on January 2, 2016, at an offering price of $47.10 per share. The front-end load for this fund is 5 percent, and the back-end load for redemptions within one year is 2 percent. The underlying asse

> A sector fund specializing in commercial bank stocks had average daily assets of $3.4 billion during the year. This fund sold $1.25 billion worth of stock during the year, and its turnover ratio was 0.42. How much stock did this mutual fund purchase duri

> In Problem 18, suppose a put option with a $40 strike is also available with a premium of $2.80. Calculate your percentage return for the six-month holding period if the stock price declines to $36 per share. Data from Problem 18: Suppose you have $28,

> In Problem 18, suppose a dividend of $0.80 per share is paid. Comment on how the returns would be affected. Data from Problem 18: Suppose you have $28,000 to invest. You’re considering Miller-Moore Equine Enterprises (MMEE), which is currently selling

> How will personal tax rates impact the choice of a traditional versus a Roth IRA?

> Suppose you have $28,000 to invest. You’re considering Miller-Moore Equine Enterprises (MMEE), which is currently selling for $40 per share. You also notice that a call option with a $40 strike price and six months to maturity is available. The premium i

> You’ve located the following option quote for Eric-Cartman, Inc. (ECI): Two of the premiums shown can’t possibly be correct. Which two? Why? Call Put ECI Stock Price Strike Exp. Vol. Last Vol. Last 20

> In Problem 14, suppose JC Penney stock sells for $8 per share immediately before your options’ expiration. What is the rate of return on your investment? What is your rate of return if the stock sells for $10 per share (think about it)? Assume your holdi

> You believe the stock in Freeze Frame Co. is going to fall, so you short 600 shares at a price of $72. The initial margin is 50 percent. Construct the equity balance sheet for the original trade. Now construct equity balance sheets for a stock price of $

> You just sold short 750 shares of Wetscope, Inc., a fledgling software firm, at $96 per share. You cover your short when the price hits $86.50 per share one year later. If the company paid $0.75 per share in dividends over this period, what is your rate

> Which put contract sells for the lowest price? Which one sells for the highest price? Explain why these respective options trade at such extreme prices.

> If you wanted to purchase the right to sell 2,000 shares of JC Penney stock in November 2015 at a strike price of $9 per share, how much would this cost you?

> Looking back at Problem 12, suppose the call money rate is 5 percent and your broker charges you a spread of 1.25 percent over this rate. You hold the stock for six months and sell at a price of $65 per share. The company paid a dividend of $0.25 per sha

> The 1980s were a good decade for investors in S&P 500 stocks. To find out how good, construct a spreadsheet that calculates the arithmetic average return, variance, and standard deviation for the S&P 500 returns during the 1980s using spreadsheet functio

> You are given the returns for the following three stocks: Calculate the arithmetic return, geometric return, and standard deviation for each stock. Do you notice anything about the relationship between an asset’s arithmetic return,

> Given your answer to the last question and the discussion in the chapter, why would any rational person do anything other than load up on 100 percent small stocks?

> Suppose the call money rate is 4.5 percent, and you pay a spread of 2.5 percent over that. You buy 800 shares of stock at $34 per share. You put up $15,000. One year later, the stock is selling for $48 per share and you close out your position. What is y

> Suppose you purchase 500 shares of stock at $48 per share with an initial cash investment of $8,000. If your broker requires a 30 percent maintenance margin, at what share price will you be subject to a margin call? If you want to keep your position open

> Look back to Figure 1.1 and find the value of $1 invested in each asset class over this 90-year period. Calculate the geometric return for small-company stocks, large-company stocks, long-term government bonds, Treasury bills, and inflation.

> You have found an asset with a 12.60 percent arithmetic average return and a 10.24 percent geometric return. Your observation period is 40 years. What is your best estimate of the return of the asset over the next 5 years? 10 years? 20 years?

> Suppose the call money rate is 5.6 percent, and you pay a spread of 1.2 percent over that. You buy 1,000 shares at $40 per share with an initial margin of 50 percent. One year later, the stock is selling for $45 per share and you close out your position.

> In Problem 13, suppose the call money rate is 5 percent and you are charged a 1.5 percent premium over this rate. Calculate your return on investment for each of the following share prices one year later. Ignore dividends. a. $56 b. $48 c. $32 Suppose in

> Based on the historical record, what is the approximate probability that an investment in small stocks will double in value in a single year? How about triple in a single year?

> Based on the historical record, if you invest in long-term U.S. Treasury bonds, what is the approximate probability that your return will be below −6.3 percent in a given year? What range of returns would you expect to see 95 percent of the time? 99 perc

> Repeat Problems 2 and 3 assuming the initial margin requirement is 70 percent. Does this suggest a relationship between the initial margin and returns Problems 2: You purchase 275 shares of 2nd Chance Co. stock on margin at a price of $53. Your broker

> In Problem 2, suppose you sell the stock at a price of $62. What is your return? What would your return have been had you purchased the stock without margin? What if the stock price is $46 when you sell the stock? Problem 2: You purchase 275 shares of

> What is the distinction between a real asset and a financial asset? What are the two basic types of financial assets, and what does each represent?

> What is the Analees’ return objective? a. 6.67 percent b. 6.17 percent c. 3.83 percent

> Compare the City Center project with specific projects discussed in the chapter, namely: Sony’s Chromatron, Syntex’s Enrprostil, Motorola’s Iridium, Eurotunnel’s Channel Tunnel, Boeing’s Dreamliner, and Airbus’s A380. Your discussion should indicate whet

> Consider whether MGM faced issues in the City Center project that could be characterized as sunk costs, and if so, whether they exhibited behavior consistent with “escalation of commitment.”

> Consider the issues of project budget, scope, and project timetable. Discuss the extent to which the City Center project reflects survey evidence discussed in the chapter about capital budgeting biases associated with the planning fallacy.

> What insights from the discussion of the Morgan Stanley 2003 report on eBay apply to the 2013 report on Aetna by ValuEngine?

> What insights from the discussion of the Morgan Stanley 2003 report on eBay apply to the 2013 report on Aetna by Leerink Swann?

> What insights from the discussion of the Morgan Stanley 2003 report on eBay apply to the 2013 report on Aetna by Cantor Fitzgerald?

> What insights from the discussion of the Morgan Stanley 2003 report on eBay apply to the 2013 report on Aetna by Jefferies?

> How would you use behavioral concepts to explain generally why different analysts arrive at different price targets?

> Identify the psychological phenomena in the minicase. Prioritize the phenomena from most important to least important. Begin your answer by defining the phenomena, and then describing their role in the minicase. As part of your answer, discuss the implic

> The U.S. Army Corps of Engineers maintains locks and dams on U.S. waterways, and engages consultants to analyze the kinds of issues described in the minicase. One of these consultants points out that even if it is below standard, concrete might last a hu

> Imagine a decision task in which you are to choose between two alternatives that involve blindly drawing a single chip from one of two urns, labeled A and B respectively. Both urns contain colored balls. The proportion of the different colors is describe

> As of July 2015, 30 countries worldwide are operating 438 nuclear reactors for electricity generation and 67 new nuclear plants are under construction in 15 countries. Nuclear power plants provided 10.9 percent of the world’s electricity production in 20

> Of the 10 psychological phenomena introduced in Chapter 1, identify which ones apply to the minicase, and give reasons to support your answer.

> Consider the financial planning case study in Chapter 13 about William and Mira Bold. At the end of the case, financial planner Claire begins to prepare for her second meeting with the Bolts. How can Claire use the information provided about the Bolts’ f

> Discuss if the manner in which people’s answers to questions 7.1 through 7.6 above provides an indication of their financial literacy.90 Questions 7.1: Suppose you had $100 in a savings account and the interest rate was 2 percent per year. After five y

> Given the information provided in the chapter, discuss the psychological phenomena associated with Martha Stewart’s investment decisions.

> Precept Capital Management is a hedge fund located in Dallas, Texas. The fund employs several investment strategies, one of which is based on comparing the trajectory of stock prices to the trajectory of EPS forecasts. To illustrate the strategy, consi

> On the MHHE web site for this book, in the Chapter 13 files, you will find an Excel file with return data on Valeant and other firms. Use regression analysis to assess the factor structure of the stocks in the data file, and discuss your findings.

> The minicase in Chapter 3 contains an excerpt from a ValuEngine analyst report about the firm Aetna. The report states that ValuEngine’s forecasting models capture important features of stock price dynamics, such as short-term price reversals, intermedia

> Impact investors make investments in firms, organizations, and funds in order to generate positive social and environmental impacts alongside a financial return. Toniic is an organization dedicated to impact investing, whose members comprise ultra-high n

> Warren Buffett described his investment philosophy as being greedy when others are fearful and being fearful when others are greedy. Bob Goldfarb is the chairman of Ruane, Cunniff & Goldfarb, the investment company that manages the Sequoia Fund. Goldfarb