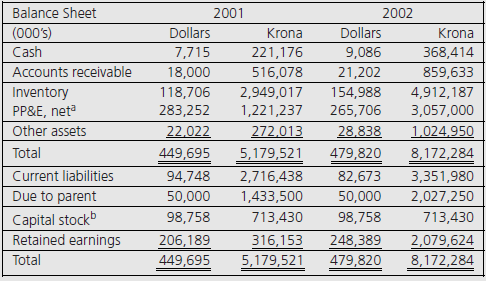

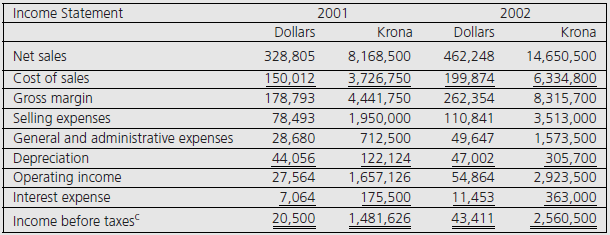

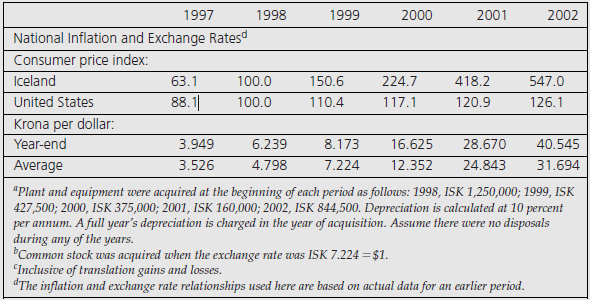

Question: Inc. In 1993 Icelandic Enterprises was incorporated

Inc. In 1993 Icelandic Enterprises was incorporated in Reykjavik to manufacture and distribute women’s cosmetics in Iceland. All of its outstanding stock was acquired at the beginning of 2001 by International Cosmetics, Ltd. (IC), a U.S.-based MNE headquartered in Shelton, Connecticut.

Competition with major cosmetics manufacturers both within and outside Iceland was very keen. As a result, Icelandic Enterprises (now a whollyowned subsidiary of International Cosmetics) was under constant pressure to expand its product offerings. This required frequent investment in new equipment. Competition also affected the company’s pricing flexibility. As the demand for cosmetics was price elastic, Icelandic lost market share every time it raised its prices. Accordingly, when Icelandic increased selling prices, it did so in small increments while increasing its advertising and promotional efforts to minimize the adverse effects of the price increase on sales volume.

International Cosmetics’ financial policies with respect to Icelandic were dictated by two major considerations: the continued inflation and devaluation of the Icelandic krona (ISK). To counter these, headquarters management was eager to recoup its dollar investment in Icelandic Enterprises through dollar dividends. If dividends were not possible, subsidiary managers were instructed to preserve IC’s original equity investment in Icelandic krona. Due to the unstable krona, all financial management analyses were made in dollars. International Cosmetics designated the dollar as Icelandic Enterprise’s functional currency. Accordingly, it adopted the temporal method when translating Icelandic’s krona accounts to their dollar equivalents. All monetary assets and liabilities were translated to dollars using the current exchange rate. All nonmonetary items, except those assets that were carried at current values, were translated using historical rates. Income and expense accounts were translated at the average exchange rates prevailing during the year, except depreciation and amortization charges related to assets translated at historical exchange rates. Translation gains and losses were taken directly to consolidated earnings.

Adjusting Icelandic’s accounts for inflation was not attempted. Management believed that such restatements were too costly and subjective. IC’s management also claimed that translating Icelandic’s accounts to dollars automatically approximated the impact of inflation. The following is a comparative balance sheet and income statement for Icelandic Enterprises, along with relevant foreign exchange and general price-level indexes.

Required:

1. Comment on International Cosmetics’ policies on the basis of “as reported†earnings.

2. Is management correct in stating that by translating their financial reports into dollars they “automatically approximate the impact of inflation�

3. What revised actions/policies would you recommend based on inflation adjusted figures?

Transcribed Image Text:

Balance Sheet 2001 2002 (000's) Dollars Krona Dollars Krona Cash 7,715 221,176 9,086 368,414 Accounts receivable 18,000 516,078 21,202 859,633 Inventory PP&E, neta Other assets 118,706 283,252 2,949,017 1,221,237 154,988 265,706 4,912,187 3,057,000 22,022 272,013 28,838 1.024.950 Total 449,695 5,179,521 479,820 8,172,284 Current liabilities 94,748 2,716,438 82,673 3,351,980 Due to parent 50,000 1,433,500 50,000 2,027,250 Capital stockb Retained earnings 98,758 713,430 98,758 713,430 206,189 449,695 316,153 5,179,521 248,389 479,820 2,079,624 8,172,284 Total Income Statement 2001 2002 Dollars Krona Dollars Krona Net sales 328,805 8,168,500 462,248 14,650,500 Cost of sales Gross margin Selling expenses General and administrative expenses 150,012 3,726,750 199,874 6,334,800 178,793 4,441,750 262,354 8,315,700 78,493 1,950,000 110,841 3,513,000 28,680 712,500 49,647 1,573,500 Depreciation Operating income Interest expense Income before taxes 44,056 27,564 122,124 1,657,126 47,002 54,864 305,700 2,923,500 363,000 2,560,500 7,064 175,500 1,481,626 11,453 43,411 20,500 1997 1998 1999 2000 2001 2002 National Inflation and Exchange Ratesd Consumer price index: Iceland 63.1 100.0 150.6 224.7 418.2 547.0 United States 88.1 100.0 110.4 117,1 120.9 126.1 Krona per dollar: Year-end 3.949 6.239 8.173 16.625 28.670 40.545 Average 3.526 4.798 7.224 12.352 24.843 31.694 "Plant and equipment were acquired at the beginning of each period as follows: 1998, ISK 1,250,000; 1999, ISK 427,500; 2000, ISK 375,000; 2001, ISK 160,000; 2002, ISK 844,500. Depreciation is calculated at 10 percent per annum. A full year's depreciation is charged in the year of acquisition. Assume there were no disposals during any of the years. Common stock was acquired when the Exchange Rate was ISK 7.224 = $1. "Inclusive of translation gains and losses. "The inflation and exchange rate relationships used here are based on actual data for an earlier period.

> Exhibit 1-4 lists the number of majority owned foreign affiliates in each country that Nestle includes in its consolidated results. What international accounting issues are triggered by this Exhibit? Countries in Which Nestle Owns One or More Majori

> One of the accounting development patterns that was introduced in Chapter 2 was the macroeconomic development model. Under this framework accounting practices are designed to enhance national macroeconomic goals. A national policy advocating stable emplo

> Identify three to four criteria that you would personally use to judge the merits of any corporate database. Use these criteria to rate the information content of any Web site appearing in exhibit 9-4 as excellent, fair, or poor. // EXHIBIT 9-4 Free

> The IASB Web site (www.iasb.org) summarizes each of the current International Financial Reporting Standards. Required: Answer each of the following questions. a. In measuring inventories at the lower of cost or net realizable value, does net realizable

> The U.S. Securities and Exchange Commission (SEC) roadmap issued in 2008 may eventually move U.S. issuers to report under International Financial Reporting Standards (IFRS). Consider the following critical questions of such a move: a. IFRS lack detailed

> Chapter 3 discusses financial reporting and accounting measurements under International Financial Reporting Standards (IFRS). Chapter 4 discusses the same issues for U.S. GAAP and Exhibit 4-2 summarizes some of the significant differences between IFRS an

> The biographies of current IASB board members are on the IASB Web site (www.iasb.org). Required: Identify the current board members (including the chair and vice-chair). Note each member’s home country and prior affiliation(s). Which board members have

> Exhibit 8-3 identifies current IASB standards and their respective titles. Required: Using information on the IASB Web site (www.iasb.org) or other available information, prepare an updated list of IASB standards. EXHIBIT 8-3 Current IASB Standard

> The chapter contains a chronology of some significant events in the history of international accounting standard setting. Required: Consider the 1995 European Commission adoption of a new approach to accounting harmonization. Consult some literature re

> The text discusses the many organizations involved with international convergence activities, including the IASB, EU, and IFAC. Required: a. Compare and contrast these three organizations in terms of their standard-setting procedures. b. At what types a

> Exhibit 8-2 presents the Web site addresses of national accountancy organizations, many of which are involved in international accounting standard-setting and convergence activities. Required: Select one of the accounting organizations and search its

> What international reporting issues are triggered by AKZO NOBEL’s foreign operations disclosures appearing in Exhibit 1-3 for investors? For managerial accountants? Selected 2008 Foreign Operations Data for AKZO Nobel (Euro million

> Exhibit 8-1 presents the Web site addresses of many major international organizations involved in international accounting harmonization. Consider the following three: the International Federation of Accountants (IFAC), the United Nations Intergovernment

> Three solutions have been proposed for resolving the problems associated with filing financial statements across national borders: (1) reciprocity (also known as mutual recognition), (2) reconciliation, and (3) use of international standards. Required:

> Compare and contrast the following proposed approaches for dealing with international differences in accounting, disclosure, and auditing standards: (1) reciprocity, (2) reconciliation, and (3) international standards.

> Distinguish between the terms “harmonization” and “convergence” as they apply to accounting standards.

> What role do the United Nations and the Organization for Economic Cooperation and Development play in harmonizing accounting and auditing standards?

> Describe IOSCO’s work on harmonizing disclosure standards for cross-border offerings and initial listings by foreign issuers. Why is this work important to securities regulators around the world?

> Why is the concept of auditing convergence important? Will international harmonization of auditing standards be more or less difficult to achieve than international harmonization of accounting principles? Describe IFAC’s work on converging auditing stand

> What is the purpose of accounting harmonization in the European Union (EU)? Why did the EU abandon its approach to harmonization via directives to one favoring the IASB?

> Describe the structure of the International Accounting Standards Board and how it sets International Financial Reporting Standards.

> What evidence is there that International Financial Reporting Standards are becoming widely accepted around the world? Do you believe that worldwide convergence of accounting standards will end investor concerns about cross-national differences in accoun

> Does the geographic pattern of merchandise exports contained in Exhibit 1-2 correlate well with the pattern of AKZO Nobel’s geographic distribution of sales shown in Exhibit 1-3? What might explain any differences you observe? EXHI

> What are the key rationales against the development and widespread application of International Financial Reporting Standards?

> What are the key rationales that support the development and widespread application of International Financial Reporting Standards?

> Sir David Tweedie, chairman of the International Accounting Standards Board, is quoted as saying that the IASB and the FASB will eventually merge. “U.S. standards and ours will become so close that it will be senseless having two boards, and they will me

> Petro China Company Limited (Petro China) was established as a joint stock company under the company law of the People’s Republic of China in 1999 as part of the restructuring of China National Petroleum Corporation. Petro China is an integrated oil and

> The year-end balance sheet of Helsinki Corporation, a wholly owned British affiliate in Finland, is reproduced here. Relevant exchange rate and inflation information is also provided. Exchange rate and price information: January 1: General price index

> Doosan Enterprises, a U.S. subsidiary domiciled in South Korea, accounts for its inventories on a FIFO basis. The company translates its inventories to dollars at the current rate. Year-end inventories are recorded at 10,920,000 won. During the year, the

> Ninsuvaan Corporation, a U.S. subsidiary in Bangkok, Thailand, begins and ends its calendar year with an inventory balance of BHT500 million. The dollar/baht exchange rate on January 1 was $0.02 = BHT1. During the year, the U.S. general price level advan

> The balance sheet of Rackett & Ball plc., a U.K.-based sporting goods manufacturer, is presented here. Figures are stated in millions of pounds (£m). During the year, the producers’ price index increased from 100 to 120

> Now assume that Majikstan Enterprises is a foreign subsidiary of a U.S.-based multinational corporation and that its financial statements are consolidated with those of its U.S. parent. Relevant exchange rate and general price-level information for the y

> Majikstan Enterprises has equipment on its books that it acquired at the start of 2009 . The equipment is being depreciated in straight-line fashion over a 10-year period and has no salvage value. The current cost of this equipment at the end of 2010 was

> Examine the Web sites of five exchanges listed in Appendix 1-1 that you feel would be most attractive to foreign listers. Which exchange in your chosen set proved most popular during the last two years? Provide possible explanations for your observation.

> Revisit Sobrero Corporation in Exercise 1. In addition to the information provided there, assume that Mexico’s construction cost index increased by 80 percent during the year, while the price of vacant land adjacent to Sobrero Corporation’s hotel increas

> Using the information provided in Exercise 2. Calculate Majikstan Enterprises’ net monetary gain or loss in local currency for 2011 based on the following general price-level information. 12/31/10 ……………………………………………………………………………..30,000 Average …………………………

> The comparative historical-cost balance sheets of Majikstan Enterprises for 2010 and 2011 are reproduced below. The accounts are expressed in 000’s of renges (MJR’s). Required: What was the change in Majikstanâ

> Sobrero Corporation, a Mexican affiliate of a major U.S.-based hotel chain, starts the calendar year with 1 billion pesos (P) cash equity investment. It immediately acquires a refurbished hotel in Acapulco for P 900 million. Owing to a favorable tourist

> Examine the income statements of Modello, Vestel, and Infosys, referenced earlier in this chapter. Which earnings number do you feel provides the better earnings metric for an investment analyst, and why?

> From a user’s perspective, what is the inherent problem in attempting to analyze historical cost-based financial statements of a company domiciled in an inflationary, devaluation-prone country?

> What does double-dipping mean in accounting for foreign inflation?

> How does accounting for foreign inflation differ from accounting for domestic inflation?

> What is a gearing adjustment, and on what ideas is it based?

> As a potential investor in the shares of multinational enterprises, which inflation method, restate-translate or translate-restate, would give you consolidated information most relevant to your decision needs? Which information set is best from the viewp

> Examine Exhibit 1-2 and compute the compounded annual growth rate of merchandise trade versus the global trade in services for the 20 year period beginning 1985 and ending 2005. What implication does your finding have for accounting as a service activity

> Briefly describe the historical-cost-constant purchasing power and current-cost models. How are they similar? How do they differ?

> As more and more companies span the globe in terms of their operating, financing, and investing activities, they will increasingly turn to international financial reporting standards when communicating with domestic and non-domestic financial statement r

> Following are the remarks of a prominent member of the U.S. Congress. Explain why you agree or disagree. The plain fact of the matter is that inflation accounting is a premature, imprecise, and underdeveloped method of recording basic business facts. To

> Consider the statement: “The object of accounting for changing prices is to ensure that a company is able to maintain its operating capability.” How accurate is it?

> Kashmir Enterprises, an Indian carpet manufacturer, begins the calendar year with the following Indian rupee (INR) balances: During the first week in January, the company acquires additional manufacturing inventories costing INR 2,400,000 on account an

> On December 15, MSC Corporation acquires its first foreign affiliate by acquiring 100 percent of the net assets of the Armaselah Oil Company based in Saudi Arabia for 930,000,000 Saudi Arabian riyals.(SAR). At the time, the exchange rate was $1.00 = SAR3

> A 100 percent–owned foreign subsidiary’s trial balance consists of the accounts listed as follows. Which exchange rate—current, historical, or average—would be used to translate these accounts to parent currency assuming that the foreign currency is the

> Company A is headquartered in Country A and reports in the currency unit of Country A, the Apeso. Company B is headquartered in Country B and reports in the currency unit of Country B, the Bol. Company A and B hold identical assets, Apeso100 and Bol100,

> Use the information provided in Exercise 6. Required: a. What would be the translation effect if Shanghai Corporation’s balance sheet were translated by the temporal method assuming the Chinese yuan appreciates by 25 percent? By the current rate method?

> Re-examine Exhibit 1-1 which describes the outsourcing process for HP’s production of the Proliant ML150. For each leg of the production chain, identify the various accounting and related issues that might arise. EXHIBIT 1-1 Outsou

> Shanghai Corporation, the Chinese affiliate of a U.S. manufacturer, has the balance sheet shown below. The current exchange rate is $.0.15 = CNY1. Required: a. Translate the Chinese dollar balance sheet of Shanghai Corporation into U.S. dollars at the

> Sydney Corporation, an Australian-based multinational, borrowed 10,000,000 euros from a German lender at the beginning of the calendar year when the exchange rate was EUR.60 = AUD1. Before repaying this oneyear loan, Sydney Corporation learns that the Au

> U.S. Multinational Corporation’s subsidiary in Bangkok has on its books fixed assets valued at 7,500,000 baht. One-third of the assets were acquired two years ago when the exchange rate was THB40 = $1. The other fixed assets were acquired last year when

> On January 1, the wholly-owned Mexican affiliate of a Canadian parent company acquired an inventory of computer hard drives for its assembly operation. The cost incurred was 15,000,000 pesos when the exchange rate was MXN11.3 = C$1. By yearend, the Mexic

> On April 1, A. C. Corporation, a calendar-year U.S. electronics manufacturer, buys 32.5 million yen worth of computer chips from the Hidachi Company paying 10 percent down, the balance to be paid in 3 months. Interest at 8 percent per annum is payable on

> Assume that your Japanese affiliate reports sales revenue of 250,000,000 yen. Referring to Exhibit 6-1, translate this revenue figure to U.S. dollars using the direct bid spot rate. Do the same using the indirect spot quote. EXHIBIT 6-1 Sample of Sp

> What do current, historical, and average exchange rates mean in the context of foreign currency translation? Which of these rates give rise to translation gains and losses? Which do not?

> What is the difference between the spot, forward, and swap markets? Illustrate each description with an example.

> How does the treatment of translation gains and losses differ between the current and temporal translation methods under FAS No. 52, and what is the rationale for the differing accounting treatments?

> In what way is foreign currency translation tied to foreign inflation?

> Accounting may be viewed as having three components: measurement, disclosure, and auditing. What are the advantages and disadvantages of this classification? Can you suggest alternative classifications that might be useful?

> What lessons, if any, can be learned from examining the history of foreign currency translation in the United States?

> Under what set of conditions would the temporal method of currency translation be appropriate. Under what set of conditions would the current rate method be appropriate?

> Compare and contrast features of the major foreign currency translation methods introduced in this chapter. Which method do you think is best? Why?

> Briefly explain the nature of foreign currency translation as (a) a restatement process and (b) a remeasurement process.

> What is the difference between a transaction gain or loss and a translation gain or loss?

> A foreign currency transaction can be denominated in one currency, yet measured in another. Explain the difference between these two terms using the case of a Canadian dollar borrowing on the part of a Mexican affiliate of a U.S. parent company that desi

> The Offshore Investment Fund (OIF) was incorporated in Fairfield, Connecticut, for the sole purpose of allowing U.S. shareholders to invest in Spanish securities. The fund is listed on the New York Stock Exchange. The fund custodian is the Shady Rest Ban

> Regents Corporation is a recently acquired U.S. manufacturing subsidiary located on the outskirts of London. Its products are marketed principally in the United Kingdom with sales invoiced in pounds and prices determined by local competitive conditions.

> Exhibit 5-9 ranks 34 countries on earnings opacity. Which five countries have the most surprising placement? Why do you say so? EXHIBIT 5-9 Earnings Opacity Ranking of Countries from Least to Most 25. South Africa 26. Malaysia 27. Italy 28. Pakista

> The Organisation for Economic Cooperation and Development (OECD) published its revised Principles of Corporate Governance in 2004. Required: Obtain the document from the OECD Web site (www.oecd.org). a. Outline the six sections of the OECD’s corporate

> Explain how international accounting differs from purely domestic accounting.

> Exhibit 5-8 is the corporate governance disclosure of the Volvo Group. Some of the disclosures relate to independence requirements for the board of directors and audit committee. Required: a. What is the independence requirement for the board of direct

> The Global Reporting Initiative (GRI) has developed a set of guidelines for social responsibility reporting. Required: Go to the GRI Web site (www.globalreporting. org) and find its guidelines. The disclosure guidelines are categorized as indicators of

> Corporate social responsibility (CSR), as practiced by business, means many different things. Consider the following: “At one end of the broad span of CSR lie corporate policies that any wellrun company ought to have in place anyway, policies that are ca

> Exhibit 5-4 presents the independent assurance report on Roche’s sustainability reporting. The auditor’s engagement was carried out “in accordance with International Standards on Assurance Engagements (ISAE) 3000.” Required: a. Go to the World Wide Web

> Exhibit 5-3 presents the safety and environmental disclosure of Roche. Required: Comparing the three years: (1) Which measures show an improved record of safety and environmental protection? (2) Which measures show a worse record of safety and envir

> Exhibit 5-2 presents the employment disclosure of Roche. Required: a. How do the employment levels compare between the periods presented? Where are Roche’s employees located? b. Which regions of the world have the highest turnover ra

> Exhibit 5-1 presents the business-segment and geographic-segment information of Lafarge, a French company that uses International Financial Reporting Standards (IFRS) in it consolidated financial statements. /// Required: Go to the Web site of the In

> The Outlook section in Daimler’s 2008 annual report may be found at http://ar2008.daimler. com/daimler/annual/2008/gb/English/pdf/ 04_DAI_AR2008_Management-Report.pdf (pp. 82–87). Required: Provide (1) a list of items forecasted (e.g., sales, profits,

> Why are multinational corporations increasingly being held accountable to constituencies other than traditional investor groups?

> The chapter discusses the objectives of investororiented markets: investor protection and market quality. Transparent financial reporting is important for achieving these objectives. What is transparent financial reporting? Explain how transparent financ

> Outsourcing, especially from vendors located abroad, has become a politically sensitive issue, especially in the United States. Do you think this argument has merit? What are the consequences of this debate for international accounting?

> On October 3, 2000, E-centives, incorporated in the United States, made an initial public offering on the Swiss Stock Exchange’s New Market. The company raised approximately US$40 million. E-centive’s offering circular

> Analyze Alibaba’s business model relative to all the different forms of digital and online marketing covered in this chapter.

> Given that Alibaba does not own or distribute any of the merchandise exchanged on its sites, describe what factors had to develop for the company to succeed.

> As a digital retailer, how does Alibaba provide value to Chinese consumers? What sets of values are unique to the Chinese market?

> Should all companies consider reducing their sales forces in favor of telemarketing? Discuss the pros and cons of this action.

> Refer to Appendix 2, Marketing by the Numbers, to determine the marketing return on sales (marketing ROS) and return on marketing investment (marketing ROI) for Company A and Company B in the chart below. Which company is performing better? Explain.

> Many marketers are still learning how to use social media platforms effectively to engage customers in meaningful relationships. Locate three social media platforms used by the Kenneth Cole brand to engage customers. Is the brand’s marketing message cons

> Kenneth Cole believes that his controversial tweets improve business and provoke conversation and awareness. Is this an effective use of social media to engage customers with the brand? Why or why not?

> Discuss advantages and disadvantages of “Buy” buttons for social media sites like Pinterest and search engines like Google. What are the advantages and disadvantages for marketers making their goods available through “Buy” buttons on these sites?

> What competitive advantage does Pinterest (www.pinterest.com) have over other social media that might make its “Buy” button more successful?

> Although mobile advertising makes up a small percentage of online advertising, it is one of the fastest-growing advertising channels. But one obstacle is measuring return on investment in mobile. How are marketers measuring the return on investment in mo

> Visit www.krazycouponlady.com and browse a deal you would consider purchasing. After identifying the deal, conduct an online price comparison at various retailers to determine the range of prices you would typically pay for the product. Present your conc