Question: Marissa Skye and Alexa Reichele, tire analysts

Marissa Skye and Alexa Reichele, tire analysts for a global investment fund located in Manhattan, are examining the 20X0 earnings performance of two potential investment candidates. Reflecting the company’s investment philosophy of picking the best stocks wherever they are located in the world, both junior analysts have adopted an approach of undertaking matched comparisons of leading firms in the tire industry. For starters, Dietrich and Marissa focused on Goodyear Tire & Rubber Company (United States) and Continental A.G. (Germany) as their first screen.

ALEXA: Well, what do you think, Marissa?

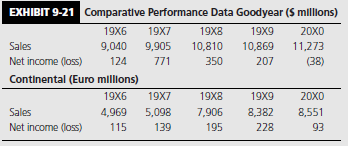

MARISSA: Looking at the income trends (see Exhibit 9-21), I sort of like Continental.

ALEXA: Yes, I agree. Goodyear’s results are much more volatile.

MARISSA: I always look to see how a company has done in an off year. Owing to the continued consolidation of the tire industry, excess capacity created by reduced demand for autos and trucks, as well as reduced consumer spending for replacement tires in light of economic and political uncertainties, 20X0 was a disastrous year for every major company in the industry. Given that environment, Continental’s performance was stellar!

ALEXA: Maybe we’d better check with Kazuo, our accountant, to see if we’re reading the tea leaves correctly.

MARISSA: I’ll give him a call. (After a 5-minute conversation) ALEXA: Well, what did he say?

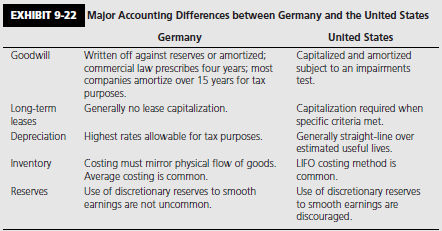

MARISSA: He said, we’re probably correct in our overall assessment (I think he’s just being polite), but that we’d better check the company’s accounting policies. He says German accounting principles tend to impart a conservative bias to corporate earnings. He’ll send us an e-mail attachment summarizing some major GAAP differences between the United States and

Germany very soon. (The e-mail attachment is reproduced as Exhibit 9-22.)

MARISSA: (Having examined the attachment) Looks like there are some major differences in reporting rules between Germany and the United States.

ALEXA: Do you think we should attempt to restate Continental’s accounts to a U.S. GAAP basis?

MARISSA: Why don’t we try?

ALEXA: Where should we start?

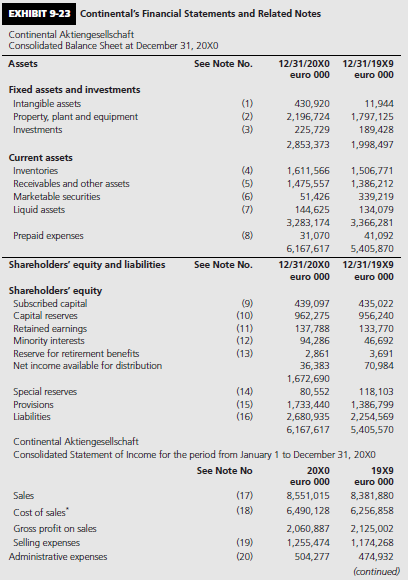

MARISSA: Let’s examine Continental’s financial statements (see Exhibit 9-23) to see if we can detect any unusual accounting practices that may have a distorting effect on the company’s reported performance. I notice that Continental follows the European practice of including both parent company (Consolidated A.G.) and consolidated numbers. Let’s just focus on the consolidated figures for now.

ALEXA: Right. And if we find some disparities, maybe we should just attempt one or two adjustments, particularly those for which we have sufficient information. If these adjustments have a significant earnings impact, then let’s press the right buttons and see if we can’t get the company to give us some additional information so that we can do a more comprehensive analysis.

MARISSA: Sounds good. Let’s get started.

///

Transcribed Image Text:

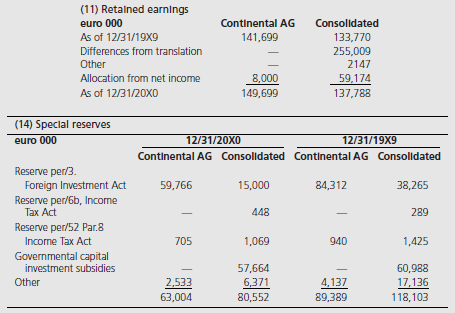

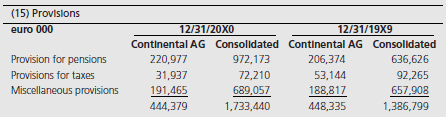

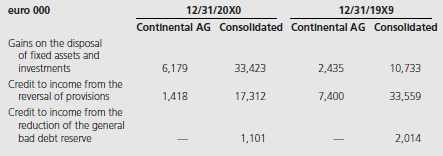

EXHIBIT 9-21 Comparative Performance Data Goodyear (S millions) 19X6 19X7 19X8 19X9 20X0 Sales 9,040 9,905 10,810 10,869 11,273 Net income (loss) 124 771 350 207 (38) Continental (Euro millions) 19X6 19X7 19X8 19X9 20X0 Sales Net income (loss) 4,969 5,098 7,906 8,382 8,551 115 139 195 228 93 EXHIBIT 9-22 MaJor Accounting Differences between Germany and the United States Germany United States Goodwill Written off against reserves or amortized; commercial law prescribes four years; most companies amortize over 15 years for tax Capitalized and amortized subject to an impairments test. purposes. Generally no lease capitalization. Long-term leases Capitalization required when specific criteria met. Generally straight-line over estimated useful lives. Depreciation Highest rates allowable for tax purposes. Inventory Costing must mirror physical flow of goods. Average costing is common. Use of discretionary reserves to smooth earnings are not uncommon. LIFO costing method is common. Use of discretionary reserves to smooth earnings are discouraged. Reserves EXHIBIT 9-23 Continental's Financial Statements and Related Notes Continental Aktiengesellschaft Consolidated Balance Sheet at December 31, 20X0 Assets See Note No. 12/31/20X0 12/31/19X9 euro 000 euro 000 Fixed assets and investments Intangible assets Property, plant and equipment (1) (2) (3) 430,920 11,944 2,196,724 1,797,125 Investments 225,729 189,428 2,853,373 1,998,497 Current assets (4) (5) (6) (7) Inventories 1,611,566 1,506,771 Receivables and other assets 1,475,557 1,386,212 Marketable securities 51,426 339,219 Liquid assets 144,625 134,079 3,283,174 3,366,281 Prepaid expenses (8) 31,070 41,092 6,167,617 5,405,870 Shareholders' equity and liabilities See Note No. 12/31/20x0 12/31/19X9 euro 000 euro 000 Shareholders' equity Subscribed capital Capital reserves Retained earnings Minority interests Reserve for retirement benefits Net income available for distribution (9) (10) (11) (12) (13) 439,097 962,275 435,022 956,240 137,788 94,286 133,770 46,692 2,861 36,383 3,691 70,984 1,672,690 Special reserves (14) (15) (16) 80,552 118,103 Provisions 1,733,440 2,680,935 1,386,799 2,254,569 Liabilities 6,167,617 5,405,570 Continental Aktiengesellschaft Consolidated Statement of Income for the period from January 1 to December 31, 20X0 See Note No 20X0 19X9 euro 000 euro 000 Sales (17) 8,551,015 8,381,880 Cost of sales (18) 6,490, 128 6,256,858 Gross profit on sales Selling expenses Administrative expenses 2,060,887 2,125,002 (19) 1,255,474 1,174,268 (20) 504,277 474,932 (continued) EXHIBIT 9-23 Continental's Financlal Statements and Related Notes (Continued) 19X9 euro 000 See Note No 20X0 euro 000 Other operating income (21) 194,266 164,076 Other operating expenses (22) 140,218 91,351 Net income from investments and financial activities Continental Aktiengesellschaft Consolidated Statement of Income for the period from January 1 to December 31, 20X0 (23) 2138,777 2116,536 See Note No 20х0 19X9 euro 000 euro 000 Net income from regular business activities 216,407 431,991 Тахes (24) 122,972 204,153 Net income for the year Balance brought forward from previous year 93,435 227,838 1,380 1,199 Minority interests in earning (25) 288 258 Withdrawal from the reserve for retirement benefits + 830 +544 Change in reserves 259,174 2158,539 Net income available for distribution 36,383 70,984 (11) Retalned earnings euro 000 Continental AG Consolldated As of 12/31/19X9 141,699 133,770 255,009 Differences from translation Other 2147 Allocation from net income 8,000 59,174 As of 12/31/20XO 149,699 137,788 (14) Special reserves euro 000 12/31/20X0 12/31/19X9 Continental AG Consolldated Continental AG Consolldated Reserve per/3. Foreign Investrment Act 59,766 15,000 84,312 38,265 Reserve per/6b, Income Таx Act 448 289 Reserve per/52 Par.8 Income Tax Act 705 1,069 940 1,425 Governmental capital investment subsidies 57,664 60,988 6,371 80,552 Other 2,533 4,137 17,136 118,103 63,004 89,389 (15) Provislons euro 000 12/31/20X0 12/31/19X9 Continental AG Consolldated Continental AG Consolldated Provision for pensions 220,977 972,173 206,374 636,626 Provisions for taxes 31,937 72,210 53,144 92,265 Miscellaneous provisions 191,465 689,057 188,817 657,908 444,379 1,733,440 448,335 1,386,799

> Explain, in your own words, the difference between a multicurrency translation exposure report and a multicurrency transactions exposure report.

> List 10 ways to reduce a firm’s foreign exchange exposure for a foreign affiliate located in a devaluation-prone country. In each instance, identify the cost–benefit trade-offs that need to be measured.

> Compare and contrast the terms translation, transaction, and economic exposure. Does FAS No. 52 resolve the issue of accounting versus economic exposure?

> The scene is a conference room on the 10th floor of an office building on Wall Street, occupied by Anthes Enterprises, a small, rapidly growing manufacturer of electronic trading systems for equities, commodities, and currencies. The agenda for the 8:00

> You have just landed a summer internship (congratulations) with the management information services group of Pirelli, the Italian global tire manufacturer. Management is acutely aware of the importance of risk management and the market’

> If you had a nontrivial sum of money to invest and decided to invest it in a country index fund, in which country or countries identified in Exhibit 1-7 would you invest your money? What accounting issues would play a role in your decision? Ten Exch

> Parent Company establishes three wholly owned affiliates in countries X, Y, and Z. Its total investment in each of the respective affiliates at the beginning of the year, together with year-end returns in parent currency (PC), appear here: Parent Compa

> Exhibit 10-9 contains a performance report that breaks out various operating variances of a foreign affiliate, assuming the parent currency is the functional currency under FAS No. 52. Using the information in Exhibit 10-9, repeat the variance analysis,

> To encourage its foreign managers to incorporate expected exchange rate changes into their operating decisions, Vancouver Enterprises requires that all foreign currency budgets be set in Canadian dollars using exchange rates projected for the end of the

> In evaluating the performance of a foreign manager, a parent company should never penalize a manager for things the manager cannot control. Given the information provided in Exercise 6, prepare a performance report identifying the relevant elements for e

> Global Enterprises, Inc. uses a number of performance criteria to evaluate its overseas operations, including return on investment. Compagnie de Calais, its Belgian subsidiary, submits the performance report shown in Exhibit 10-13 for the current fisca

> Assume the following: • Inflation and Zambian kwacha (ZMK) devaluation is 30 percent per month, or 1.2 percent per workday. • Foreign exchange rates at selected intervals for the current month are: 1/1 ……………………………………………….100.0 1/10 ……………………………………………..10

> Assume that management is considering whether to make the foreign direct investment described in Exercise 3. Investment will require $6,000,000 in equity capital. Cash flows to the parent are expected to increase by 5 percent over the previous year for e

> Review the operating data incorporated in Exhibit 10-3 for the Russian subsidiary of the U.S. parent company. Required: Using Exhibit 10-3 as a guide, prepare a cash flow report from a parent currency perspective identifying the components of the expe

> Slovenia Corporation manufactures a product that is marketed in North America, Europe, and Asia. Its total manufacturing cost to produce 100 units of product X is 2,250, detailed as follows: Raw materials ………………………………………………………………………€500 Direct labor ………

> Explain the difference between a standard costing system and the Kaizen costing system popularized in Japan.

> Referring to Exhibit 1-6, which geographic region of the world, the Americas, Asia-Pacific, or Europe-Africa-Middle East is experiencing the most activity in foreign listings? Do you expect this pattern to persist in the future? Please explain. EXHI

> How does value reporting differ from the financial reporting model you learned in your basic accounting course? Do you think this is a good reporting innovation?

> List six arguments that support a parent company’s use of its domestic control systems for its foreign operations, and six arguments against this practice.

> This chapter identifies four dimensions of the strategic planning process. How does Daihatsu’s management accounting system, described in this chapter, conform with that process?

> Foreign exchange rates are used to establish budgets and track actual performance. Of the various exchange rate combinations mentioned in this chapter, which do you favor? Why? Is your view the same when you add local inflation to the budgeting process?

> State the unique difficulties involved in designing and implementing performance evaluation systems in multinational companies.

> Refer to Exhibit 10-7 which presents the methodology for analyzing exchange rate variances. Describe in your own words what this methodology accomplishes. EXHIBIT 10-7 Three-Way Analysis of Exchange Rate Variance Computation Exchange Rate Operating

> As an employee on the financial staff of Multinational Enterprises, you are assigned to a three-person team that is assigned to examine the financial feasibility of establishing a wholly owned manufacturing subsidiary in the Czech Republic. You are to co

> Companies must decide whose rate of return (i.e., local vs. parent currency returns) to use when evaluating foreign direct investment opportunities. Discuss the internal reporting dimensions of this decision in a paragraph or two.

> General Electric Company’s worldwide performance evaluation system is based on a policy of decentralization. The policy reflects its conviction that managers will become more responsible and their business will be better managed if they are given the aut

> You are the CFO of Marisa Corporation, a major electronics manufacturer headquartered in Shelton, Connecticut. To date, your company’s operations have been confined to the United States and you are interested in diversifying your operat

> Stock exchange Web sites vary considerably in the information they provide and their ease of use. Required: Select any two of the stock exchanges presented in Appendix 1-1. Explore the Web sites of each of these stock exchanges. Prepare a table that c

> Investors, individual, corporate and institutional, are increasingly investing beyond national borders. The reason is not hard to find. Returns abroad, even after allowing for foreign currency exchange risk, have often exceeded those offered by domestic

> Examine Exhibit 9-9. On the basis of the information provided there, which opinion gives you the most comfort as an investor in nondomestic securities?

> Assume you are a member of an international policy setting committee and are responsible for harmonizing audit report requirements internationally. Examine Exhibit 9-8. Based on the varying requirments you observe, what minimum set of requirements would

> Refer to Exhibit 9-3. This exhibit presents P/E ratios for public companies in various countries. What factors might explain the differences in P/E ratios that you observe? EXHIBIT 9-3 International Price/Earnings Ratios Country Index P/E Canada SPT

> The following sales revenue pattern for a British trading concern was cited earlier in the chapter: Required: a. Perform a convenience translation into U.S. dollars for each year given the following year-end exchange rates: 2009 £1 = $2.10

> Read Appendix 9-1. Referring to Exhibit 9-14 and related notes, assume instead that Toyoza’s inventories were costed using the FIFO method and that Lincoln Enterprises employed the LIFO method. Provide the adjusting journal entries to r

> Infosys Technologies, introduced in Chapter 1, regularly provides investors with a performance measure called economic value-added (EVA). Originally pioneered by GE, EVA measures the profitability of a company after deducting not just the cost of borrowi

> Refer again to Exhibits 9-5 and 9-6. Show how you would modify the consolidated funds statement appearing in Exhibit 9-5 to enable an investor to get a better feel for the actual investing and financing activities of the Norwegian subsidiary. EXHIBI

> Based on the balance sheet and income statement data contained in Exhibit 9-5, and using the suggested worksheet format shown in Exhibit 9-20 or one of your own choosing, show how the statement of cash flows appearing in Exhibit 9-5 was derived. EXH

> Condensed comparative income statements of Señorina Panchos, a Mexican restaurant chain, for the years 2009 through 2011 are presented in Exhibit 9-18 (000,000’s pesos). You are interested in gauging the past trend in div

> One interpretation of the popular efficient markets hypothesis is that the market fully impounds all public information as soon as it becomes available. Thus, it is supposedly not possible to beat the market if fundamental financial analysis techniques a

> Revisit Exhibit 1-5 and show how the ROE statistics of 33.8 percent and 29.5 percent were derived. Which of the two ROE statistics is the better performance measure to use when comparing the financial performance of Infosys with that of Verizon, a leadin

> What are the four main steps in doing a business strategy analysis using financial statements? Why, at each step, is analysis in a cross-border context more difficult than a single-country analysis?

> What is internal control, how do internal auditors relate to it, and how does this process relate to the analysis of financial statements?

> What role does the attest function play in international financial statement analysis?

> ABC Company, a U.S.-based MNC, uses the temporal translation method (see Chapter 6) in consolidating the results of its foreign operations. Translation gains or losses incurred upon consolidation are reflected immediately in reported earnings. Company XY

> If you were asked to provide the five most important recommendations you could think of to others analyzing nondomestic financial statements, what would they be?

> How does the translation of foreign currency financial statements differ from the foreign currency translation process described in Chapter 6?

> What are common pitfalls to avoid in conducting an international prospective analysis?

> Investors can cope with accounting principles in different ways. Can you suggest two methods of coping and which of the two you find most appealing?

> Describe the impact on accounting analysis of cross-country variations in accounting measurement and disclosure practices.

> Exhibit 1-4 lists the number of majority owned foreign affiliates in each country that Nestle includes in its consolidated results. What international accounting issues are triggered by this Exhibit? Countries in Which Nestle Owns One or More Majori

> One of the accounting development patterns that was introduced in Chapter 2 was the macroeconomic development model. Under this framework accounting practices are designed to enhance national macroeconomic goals. A national policy advocating stable emplo

> Identify three to four criteria that you would personally use to judge the merits of any corporate database. Use these criteria to rate the information content of any Web site appearing in exhibit 9-4 as excellent, fair, or poor. // EXHIBIT 9-4 Free

> The IASB Web site (www.iasb.org) summarizes each of the current International Financial Reporting Standards. Required: Answer each of the following questions. a. In measuring inventories at the lower of cost or net realizable value, does net realizable

> The U.S. Securities and Exchange Commission (SEC) roadmap issued in 2008 may eventually move U.S. issuers to report under International Financial Reporting Standards (IFRS). Consider the following critical questions of such a move: a. IFRS lack detailed

> Chapter 3 discusses financial reporting and accounting measurements under International Financial Reporting Standards (IFRS). Chapter 4 discusses the same issues for U.S. GAAP and Exhibit 4-2 summarizes some of the significant differences between IFRS an

> The biographies of current IASB board members are on the IASB Web site (www.iasb.org). Required: Identify the current board members (including the chair and vice-chair). Note each member’s home country and prior affiliation(s). Which board members have

> Exhibit 8-3 identifies current IASB standards and their respective titles. Required: Using information on the IASB Web site (www.iasb.org) or other available information, prepare an updated list of IASB standards. EXHIBIT 8-3 Current IASB Standard

> The chapter contains a chronology of some significant events in the history of international accounting standard setting. Required: Consider the 1995 European Commission adoption of a new approach to accounting harmonization. Consult some literature re

> The text discusses the many organizations involved with international convergence activities, including the IASB, EU, and IFAC. Required: a. Compare and contrast these three organizations in terms of their standard-setting procedures. b. At what types a

> Exhibit 8-2 presents the Web site addresses of national accountancy organizations, many of which are involved in international accounting standard-setting and convergence activities. Required: Select one of the accounting organizations and search its

> What international reporting issues are triggered by AKZO NOBEL’s foreign operations disclosures appearing in Exhibit 1-3 for investors? For managerial accountants? Selected 2008 Foreign Operations Data for AKZO Nobel (Euro million

> Exhibit 8-1 presents the Web site addresses of many major international organizations involved in international accounting harmonization. Consider the following three: the International Federation of Accountants (IFAC), the United Nations Intergovernment

> Three solutions have been proposed for resolving the problems associated with filing financial statements across national borders: (1) reciprocity (also known as mutual recognition), (2) reconciliation, and (3) use of international standards. Required:

> Compare and contrast the following proposed approaches for dealing with international differences in accounting, disclosure, and auditing standards: (1) reciprocity, (2) reconciliation, and (3) international standards.

> Distinguish between the terms “harmonization” and “convergence” as they apply to accounting standards.

> What role do the United Nations and the Organization for Economic Cooperation and Development play in harmonizing accounting and auditing standards?

> Describe IOSCO’s work on harmonizing disclosure standards for cross-border offerings and initial listings by foreign issuers. Why is this work important to securities regulators around the world?

> Why is the concept of auditing convergence important? Will international harmonization of auditing standards be more or less difficult to achieve than international harmonization of accounting principles? Describe IFAC’s work on converging auditing stand

> What is the purpose of accounting harmonization in the European Union (EU)? Why did the EU abandon its approach to harmonization via directives to one favoring the IASB?

> Describe the structure of the International Accounting Standards Board and how it sets International Financial Reporting Standards.

> What evidence is there that International Financial Reporting Standards are becoming widely accepted around the world? Do you believe that worldwide convergence of accounting standards will end investor concerns about cross-national differences in accoun

> Does the geographic pattern of merchandise exports contained in Exhibit 1-2 correlate well with the pattern of AKZO Nobel’s geographic distribution of sales shown in Exhibit 1-3? What might explain any differences you observe? EXHI

> What are the key rationales against the development and widespread application of International Financial Reporting Standards?

> What are the key rationales that support the development and widespread application of International Financial Reporting Standards?

> Sir David Tweedie, chairman of the International Accounting Standards Board, is quoted as saying that the IASB and the FASB will eventually merge. “U.S. standards and ours will become so close that it will be senseless having two boards, and they will me

> Petro China Company Limited (Petro China) was established as a joint stock company under the company law of the People’s Republic of China in 1999 as part of the restructuring of China National Petroleum Corporation. Petro China is an integrated oil and

> The year-end balance sheet of Helsinki Corporation, a wholly owned British affiliate in Finland, is reproduced here. Relevant exchange rate and inflation information is also provided. Exchange rate and price information: January 1: General price index

> Doosan Enterprises, a U.S. subsidiary domiciled in South Korea, accounts for its inventories on a FIFO basis. The company translates its inventories to dollars at the current rate. Year-end inventories are recorded at 10,920,000 won. During the year, the

> Ninsuvaan Corporation, a U.S. subsidiary in Bangkok, Thailand, begins and ends its calendar year with an inventory balance of BHT500 million. The dollar/baht exchange rate on January 1 was $0.02 = BHT1. During the year, the U.S. general price level advan

> The balance sheet of Rackett & Ball plc., a U.K.-based sporting goods manufacturer, is presented here. Figures are stated in millions of pounds (£m). During the year, the producers’ price index increased from 100 to 120

> Now assume that Majikstan Enterprises is a foreign subsidiary of a U.S.-based multinational corporation and that its financial statements are consolidated with those of its U.S. parent. Relevant exchange rate and general price-level information for the y

> Majikstan Enterprises has equipment on its books that it acquired at the start of 2009 . The equipment is being depreciated in straight-line fashion over a 10-year period and has no salvage value. The current cost of this equipment at the end of 2010 was

> Examine the Web sites of five exchanges listed in Appendix 1-1 that you feel would be most attractive to foreign listers. Which exchange in your chosen set proved most popular during the last two years? Provide possible explanations for your observation.

> Revisit Sobrero Corporation in Exercise 1. In addition to the information provided there, assume that Mexico’s construction cost index increased by 80 percent during the year, while the price of vacant land adjacent to Sobrero Corporation’s hotel increas

> Using the information provided in Exercise 2. Calculate Majikstan Enterprises’ net monetary gain or loss in local currency for 2011 based on the following general price-level information. 12/31/10 ……………………………………………………………………………..30,000 Average …………………………

> The comparative historical-cost balance sheets of Majikstan Enterprises for 2010 and 2011 are reproduced below. The accounts are expressed in 000’s of renges (MJR’s). Required: What was the change in Majikstanâ

> Sobrero Corporation, a Mexican affiliate of a major U.S.-based hotel chain, starts the calendar year with 1 billion pesos (P) cash equity investment. It immediately acquires a refurbished hotel in Acapulco for P 900 million. Owing to a favorable tourist

> Examine the income statements of Modello, Vestel, and Infosys, referenced earlier in this chapter. Which earnings number do you feel provides the better earnings metric for an investment analyst, and why?

> From a user’s perspective, what is the inherent problem in attempting to analyze historical cost-based financial statements of a company domiciled in an inflationary, devaluation-prone country?

> What does double-dipping mean in accounting for foreign inflation?

> How does accounting for foreign inflation differ from accounting for domestic inflation?

> What is a gearing adjustment, and on what ideas is it based?

> As a potential investor in the shares of multinational enterprises, which inflation method, restate-translate or translate-restate, would give you consolidated information most relevant to your decision needs? Which information set is best from the viewp

> Examine Exhibit 1-2 and compute the compounded annual growth rate of merchandise trade versus the global trade in services for the 20 year period beginning 1985 and ending 2005. What implication does your finding have for accounting as a service activity

> Briefly describe the historical-cost-constant purchasing power and current-cost models. How are they similar? How do they differ?

> As more and more companies span the globe in terms of their operating, financing, and investing activities, they will increasingly turn to international financial reporting standards when communicating with domestic and non-domestic financial statement r

> Following are the remarks of a prominent member of the U.S. Congress. Explain why you agree or disagree. The plain fact of the matter is that inflation accounting is a premature, imprecise, and underdeveloped method of recording basic business facts. To

> Consider the statement: “The object of accounting for changing prices is to ensure that a company is able to maintain its operating capability.” How accurate is it?

> Inc. In 1993 Icelandic Enterprises was incorporated in Reykjavik to manufacture and distribute women’s cosmetics in Iceland. All of its outstanding stock was acquired at the beginning of 2001 by International Cosmetics, Ltd. (IC), a U.S

> Kashmir Enterprises, an Indian carpet manufacturer, begins the calendar year with the following Indian rupee (INR) balances: During the first week in January, the company acquires additional manufacturing inventories costing INR 2,400,000 on account an